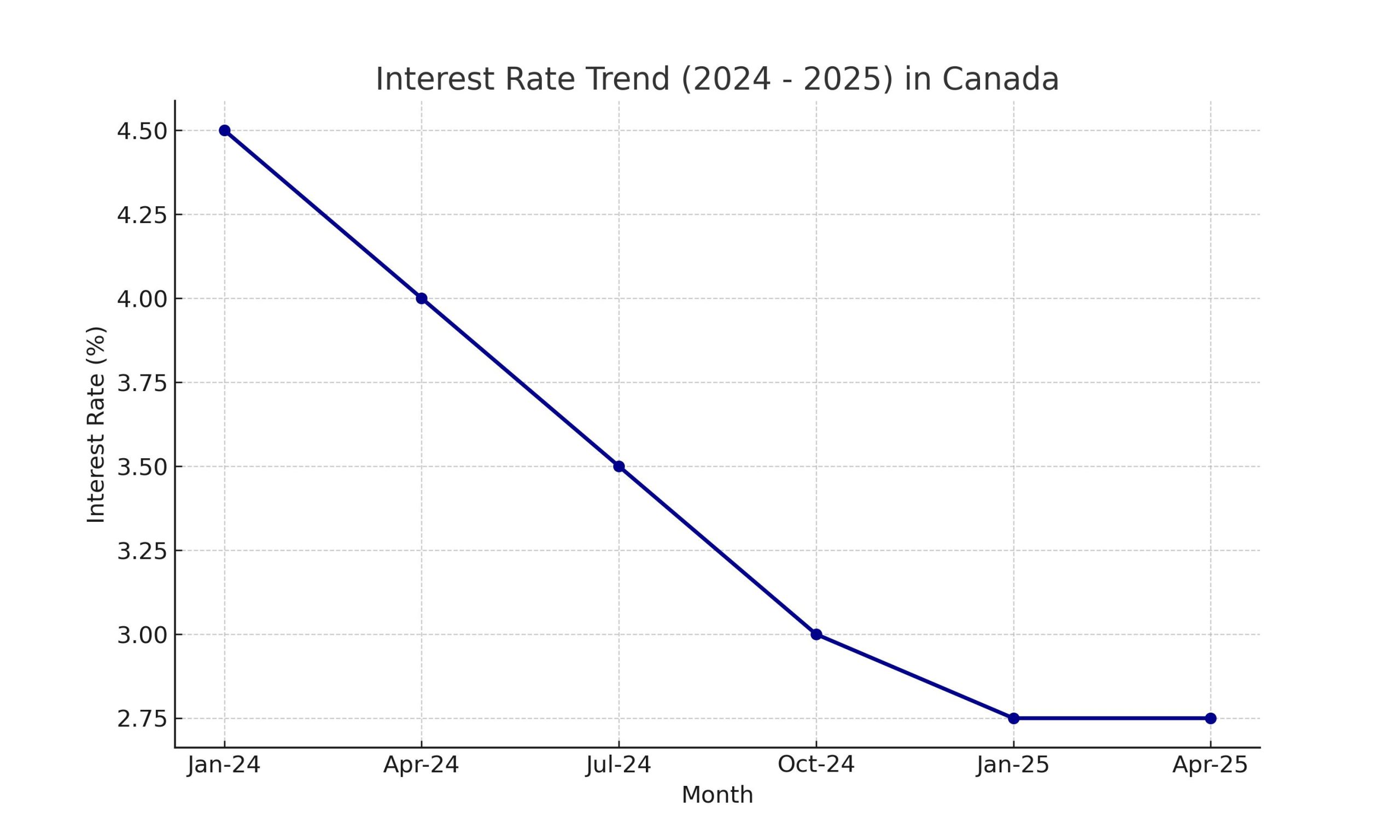

On June 4, 2025, the Bank of Canada (BoC) announced it would maintain its benchmark interest rate at 2.75%. This cautious move reflects concerns over inflation, trade uncertainty, and a moderating labour market. This is a significant moment, marking a continued pause in rate adjustments after previous cuts.

🚦 BoC Hits the “Hold” Button: What Does It Mean For YOU? 🚦

The Bank of Canada’s job is like being the country’s economic pilot: they try to steer us toward stable prices (keeping inflation in check!) and healthy growth. Today’s decision to keep interest rates unchanged at 2.75% tells us a lot about what they’re seeing on their economic dashboard.

🔍 The Big Picture: Why the Hold?

The Bank’s Governing Council decided to keep rates steady because they’re navigating a complex economic landscape. Here’s what they’re seeing:

Global Uncertainty is STILL High: 🌍 Especially concerning is the ongoing back-and-forth with U.S. tariffs and trade negotiations. This creates a big question mark for Canada’s export-driven economy. The Bank needs more clarity on how these trade policies will shake out.

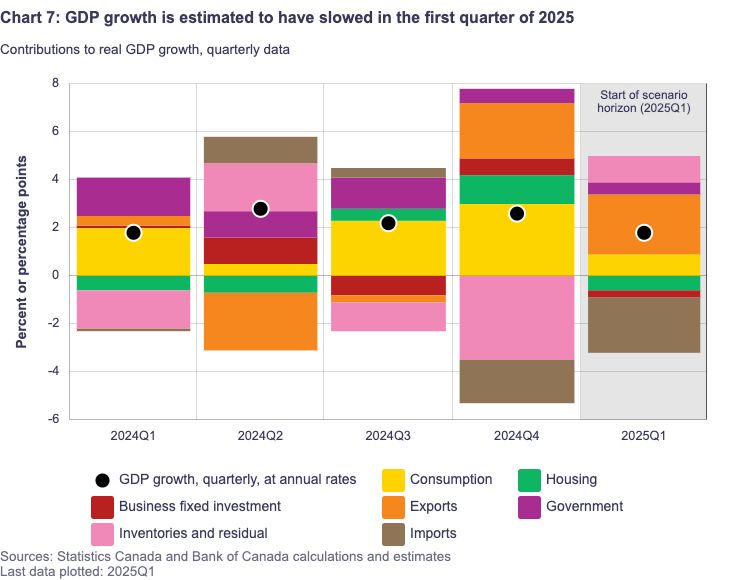

Canadian Economy: Softer, But Not Collapsing! 💪 Canada’s economy grew a bit stronger than expected in the first quarter (2.2% GDP growth!), driven partly by exports to the U.S. and inventory building. However, they expect the second quarter to be weaker as these factors reverse. Consumer spending has slowed, and housing activity is down, particularly resales.

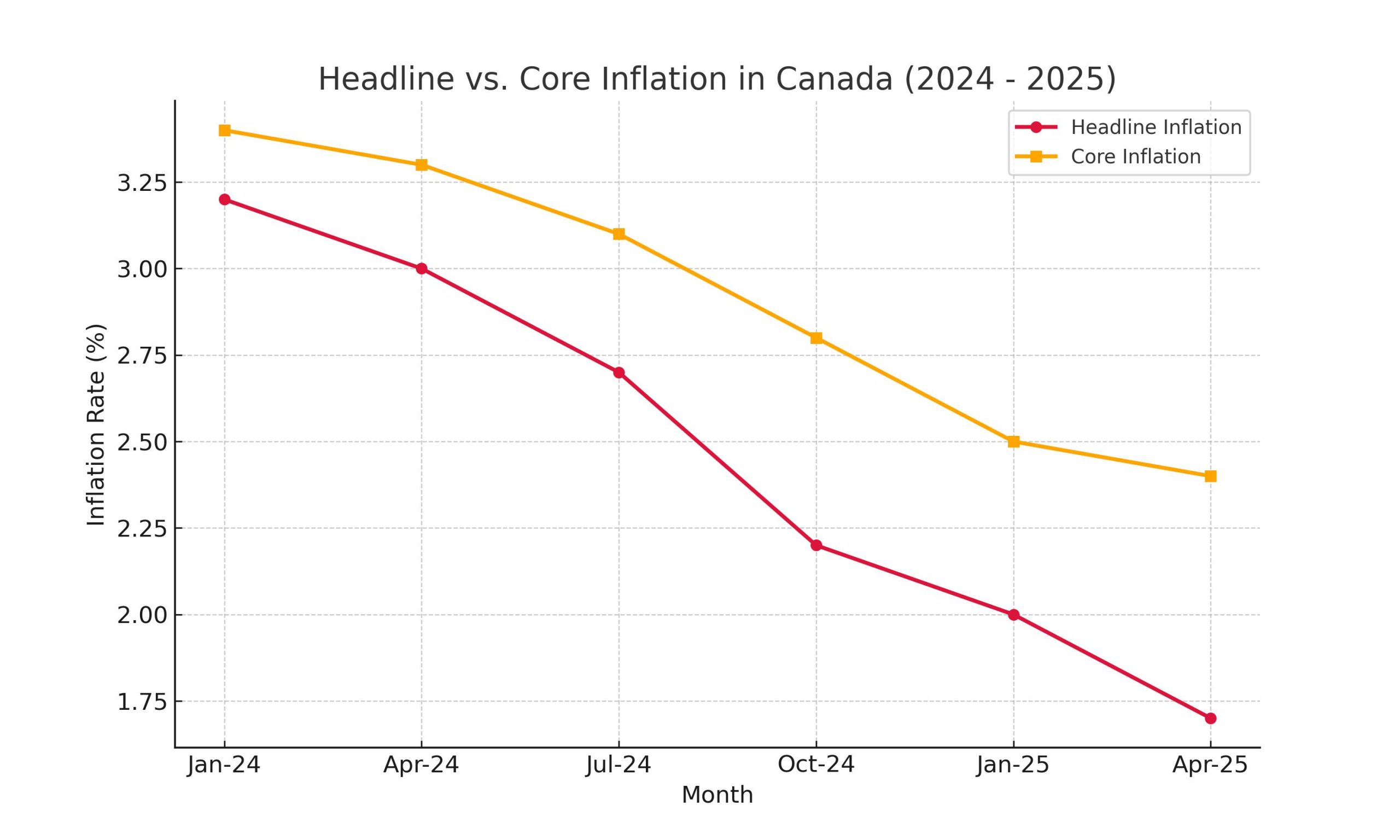

Inflation’s Tricky Dance: 📈 While inflation has generally eased from its peak, the Bank noted “unexpected firmness” in recent inflation data, and their preferred core inflation measures have moved up. Businesses are still expecting tariffs to raise prices, and many plan to pass those costs on. This “stickiness” in inflation is a key reason for the hold.

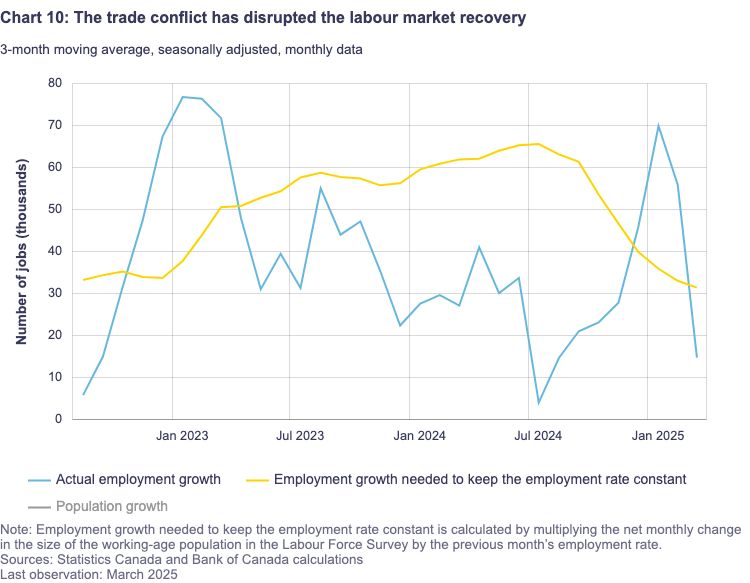

Labor Market Cooling: 🌬️ The job market has shown signs of weakening, especially in sectors tied to trade. The unemployment rate has risen to 6.9%. This typically puts downward pressure on inflation, but the Bank is watching carefully.

In simple terms: The Bank is seeing conflicting signals! The economy isn’t collapsing, but there’s a lot of uncertainty from tariffs and inflation isn’t quite behaving as smoothly as they’d like. So, they’re taking a cautious “wait and see” approach.

📌 Key Highlights

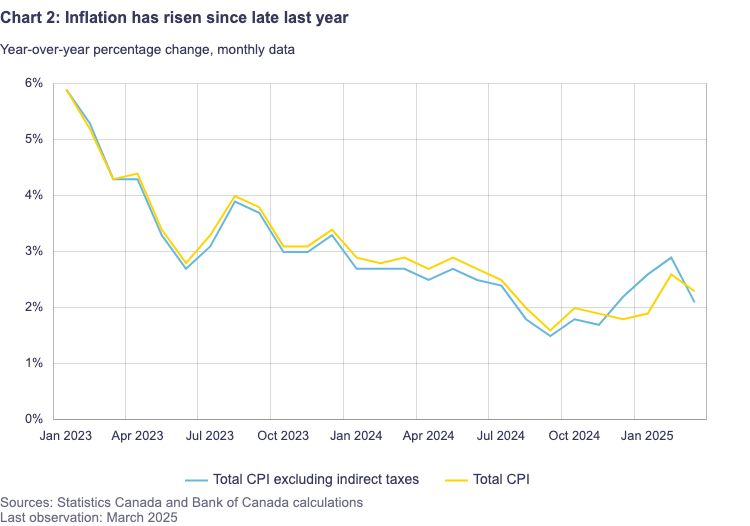

Inflation: Headline inflation fell to 1.7% in April, while core inflation remains sticky.

GDP Growth: The economy expanded by 2.2% in Q1 2025.

Labour Market: Signs of softening with slower wage growth and rising unemployment.

External Pressure: Tariff increases from the U.S. add uncertainty to exports.

Buyers: A continued hold on rates might support affordability — but be mindful of inflation.

Businesses: Exporters should prepare for volatility, especially due to U.S. trade policies.

🏡 What Does This “Hold” Mean for Your Money?

This decision has direct impacts on everyday Canadians. Let’s break it down:

For Borrowers (Especially Variable-Rate Mortgages & HELOCs): 🥳 GOOD NEWS! Your payments linked to the prime rate will stay STABLE for now. No immediate jumps in your monthly costs! This offers a much-needed breathing room. If you’re looking for a new variable mortgage, rates won’t have shifted due to this announcement.

For Savers (HISAs & GICs): 💸 STILL DECENT RETURNS! While not increasing, the rates on high-interest savings accounts and GICs will remain relatively attractive. This is a positive for those looking to grow their cash safely.

For the Housing Market: 🏠 The unchanged rate could bring a degree of stability, preventing further upward pressure on mortgage costs. However, affordability remains a significant hurdle for many, and the Bank noted a “sharp contraction in resales.”

For Businesses: 💼 Borrowing costs remain unchanged, which offers predictability for investment and operational decisions. However, uncertainty from U.S. tariffs and slower domestic demand are still headwinds.

🔮 Looking Ahead: The Bank’s Crystal Ball (Sort Of!)

The Bank of Canada made it clear they are “proceeding carefully” and will be “data-dependent.” This means they’re not committing to any future moves right now. They want to see:

How U.S. trade policy evolves and its real impact on Canadian exports.

How much any economic slowdown spills over into business investment, employment, and household spending.

How quickly cost increases (like from tariffs) are passed on to consumer prices.

How inflation expectations evolve among consumers and businesses.

Key takeaway from Governor Tiff Macklem: While there might be room for future rate cuts if the economy weakens further and price pressures stay contained, the Bank is not providing forward guidance. They are focusing on the actual data as it comes in.

✨ Your Turn!

What are your thoughts on this latest decision from the Bank of Canada? Are you breathing a sigh of relief, or hoping for more changes soon? Share your perspective in the comments below! 👇

The BoC will review its stance again on July 30, 2025. With inflation easing yet core pressures lingering, a potential rate cut remains on the table — but not guaranteed.

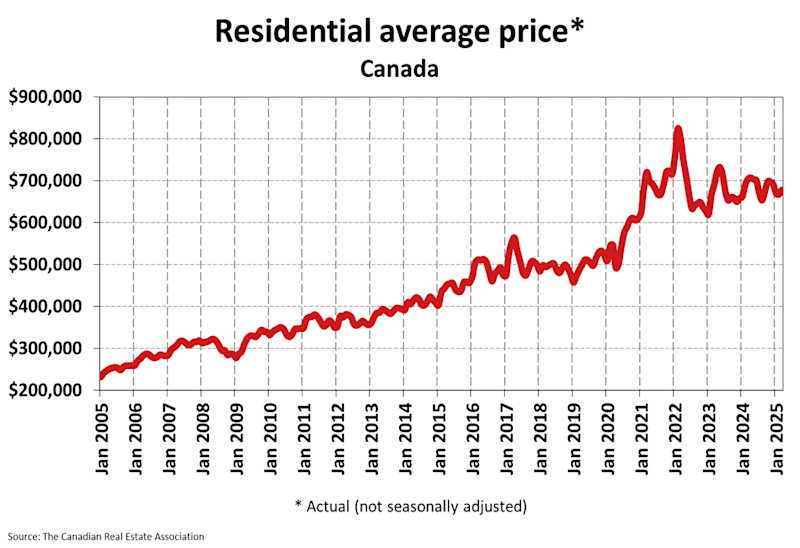

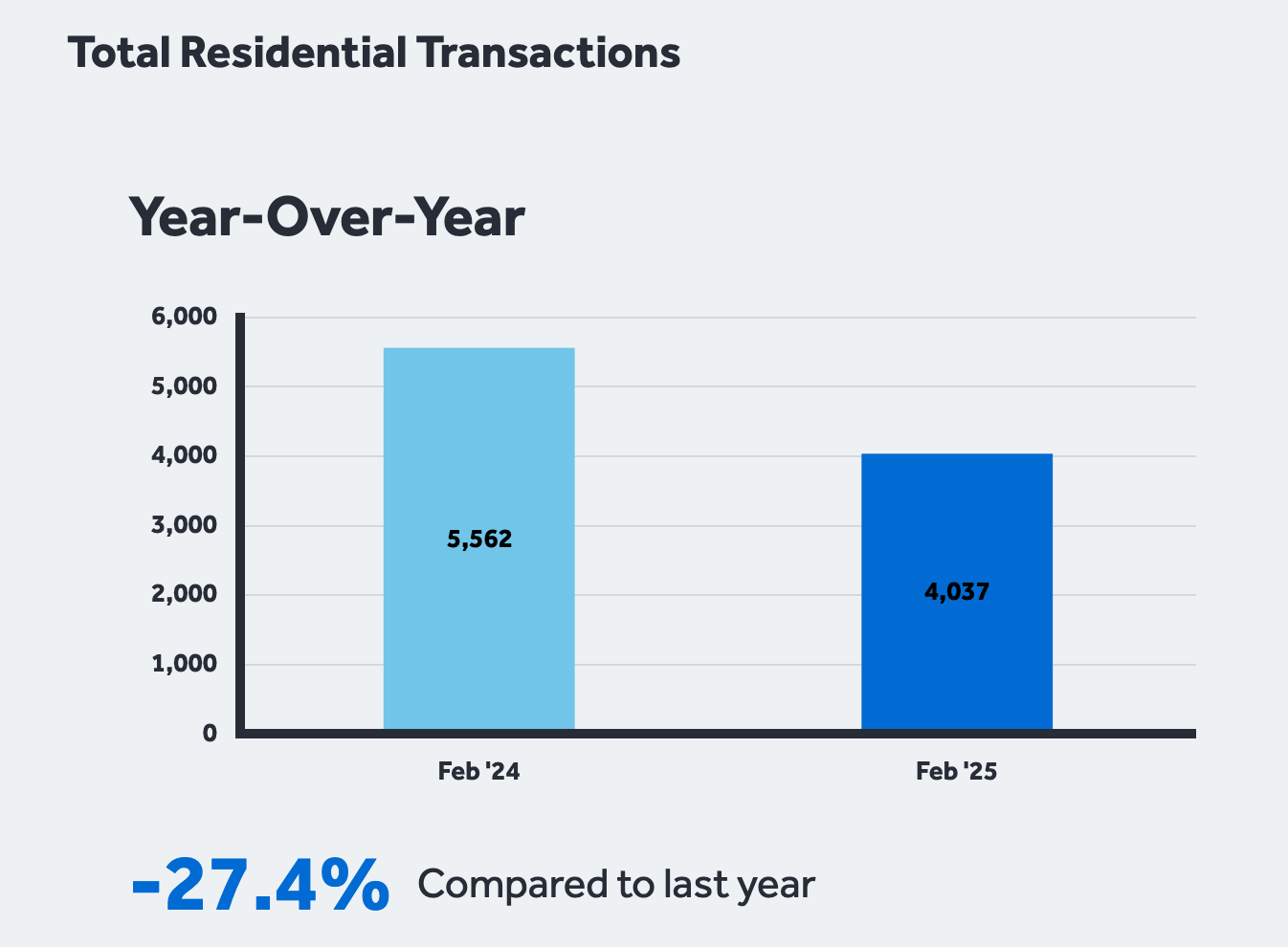

Canadian Housing Market Pauses in April 2025 Amid Shifting Conditions

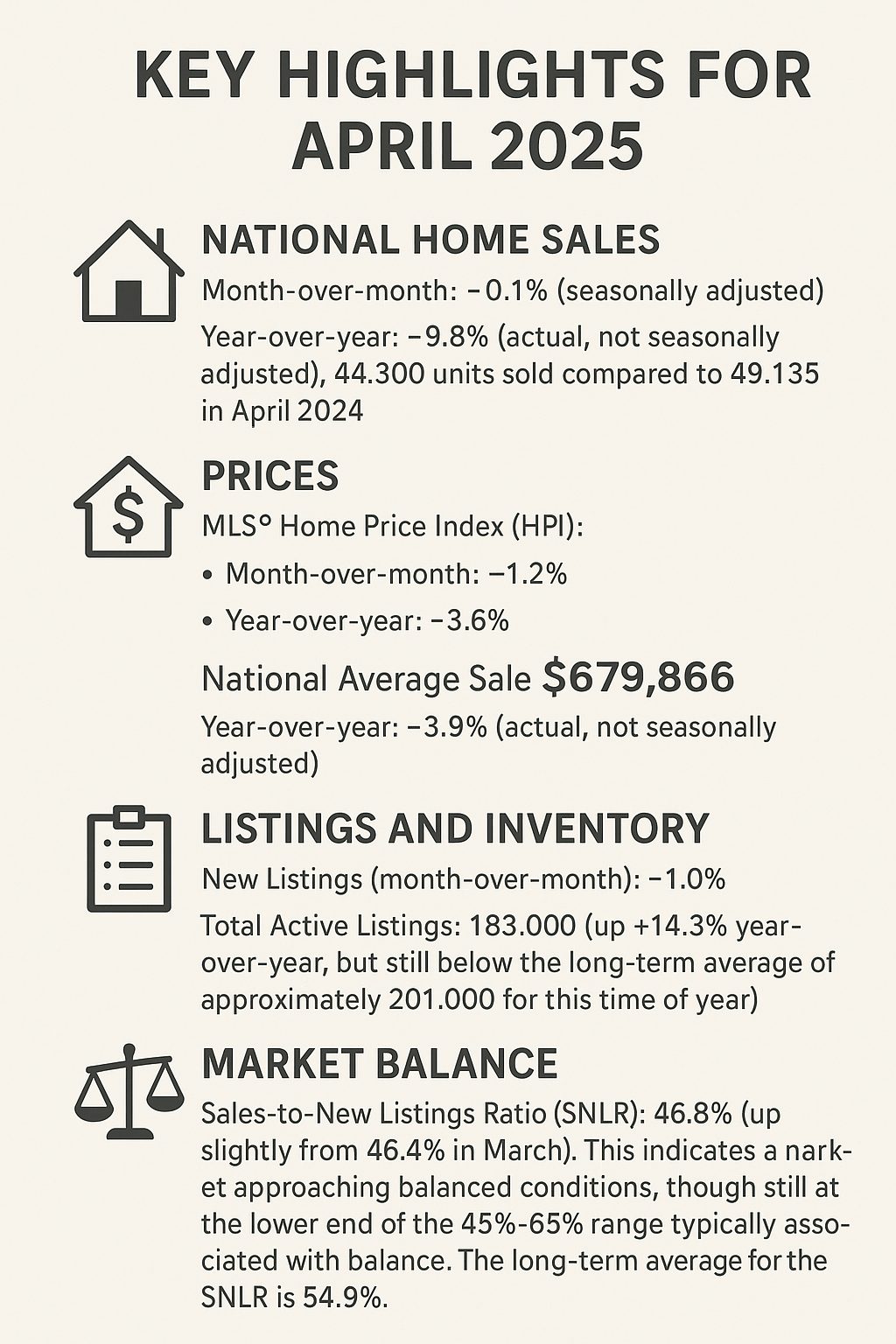

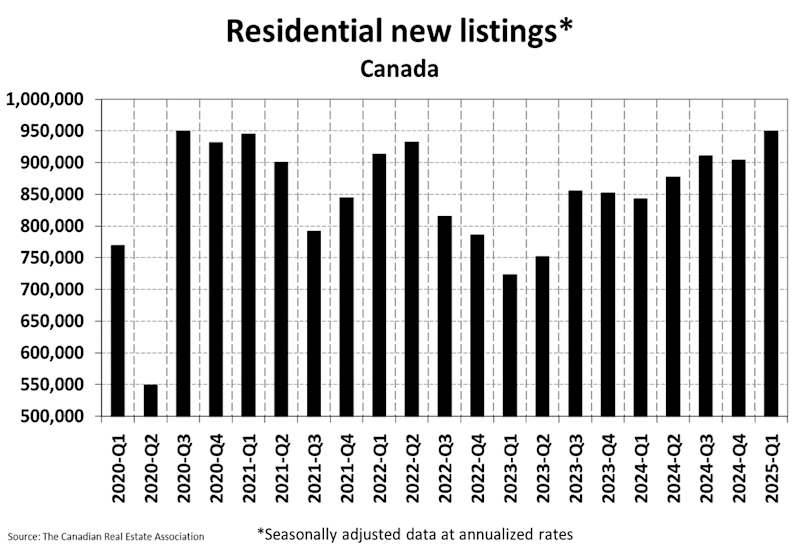

The Canadian housing market showed signs of a pause in its recent slump during April 2025, with national home sales remaining virtually unchanged from March. However, activity remains subdued compared to the previous year, and prices continue to see modest declines. This analysis, based on data released by the Canadian Real Estate Association (CREA), delves into the key trends observed in April. Key Highlights for April 2025:

National Home Sales:

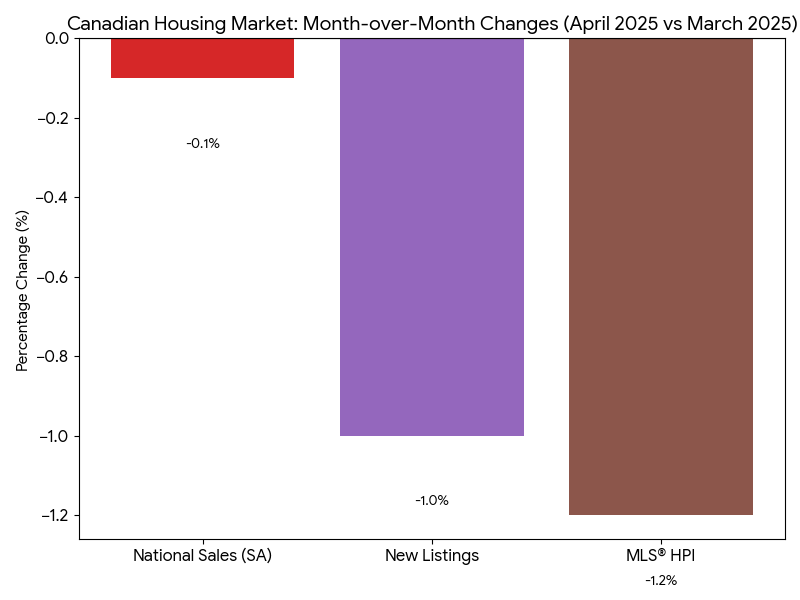

Month-over-month: -0.1% (seasonally adjusted)

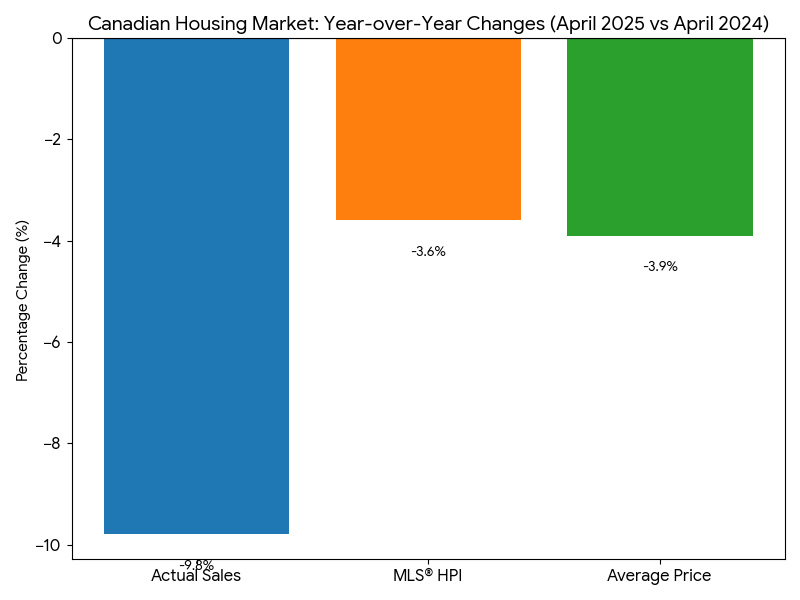

Year-over-year: -9.8% (actual, not seasonally adjusted), with 44,300 units sold compared to 49,135 in April 2024.

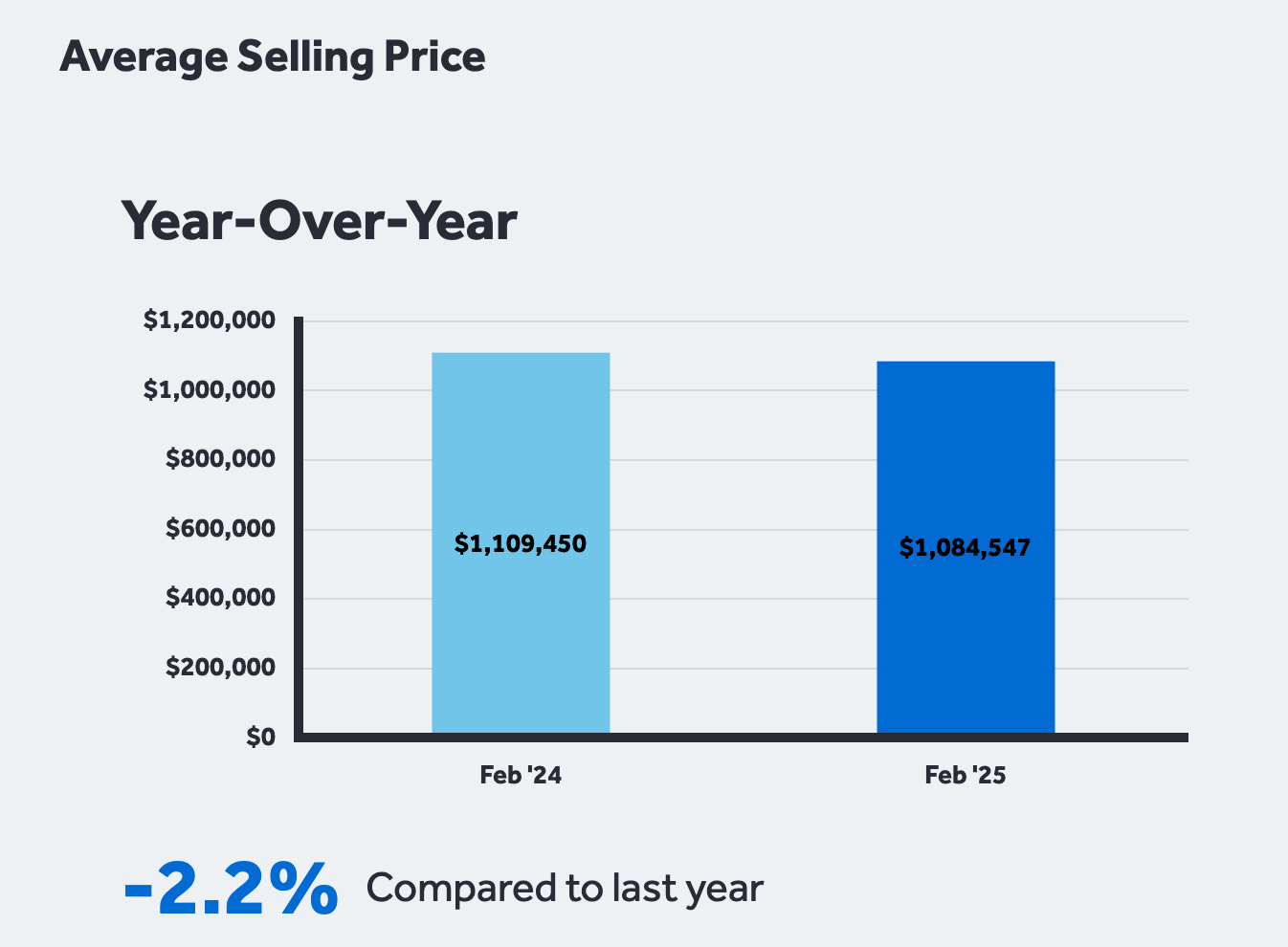

Prices:

MLS® Home Price Index (HPI):

Month-over-month: -1.2%

Year-over-year: -3.6%

National Average Sale Price: $679,866

Year-over-year: -3.9% (actual, not seasonally adjusted)

Listings and Inventory:

New Listings (month-over-month): -1.0%

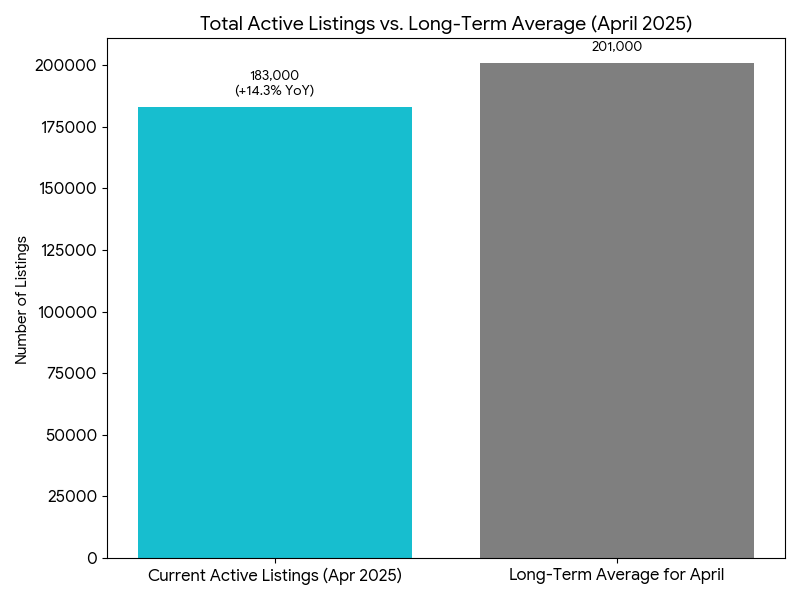

Total Active Listings: 183,000 (up +14.3% year-over-year, but still below the long-term average of approximately 201,000 for this time of year).

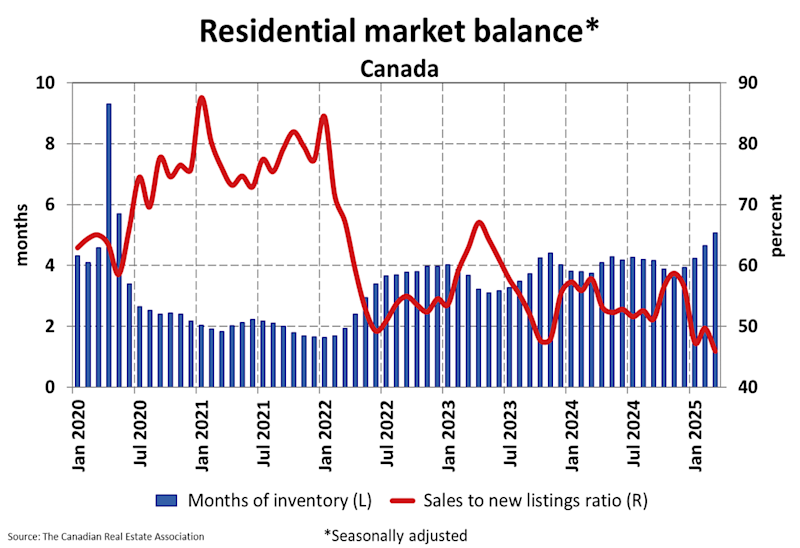

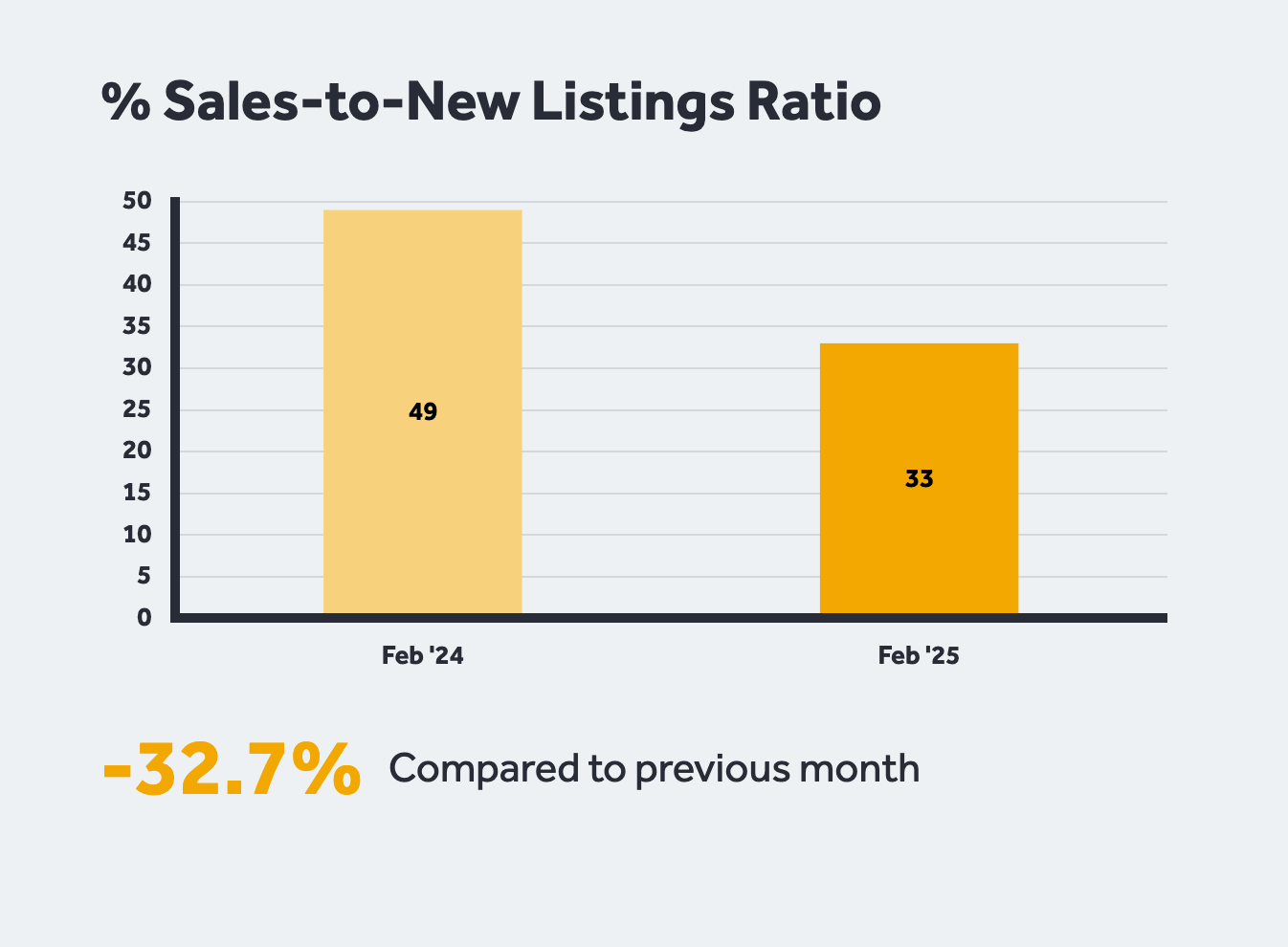

Market Balance:

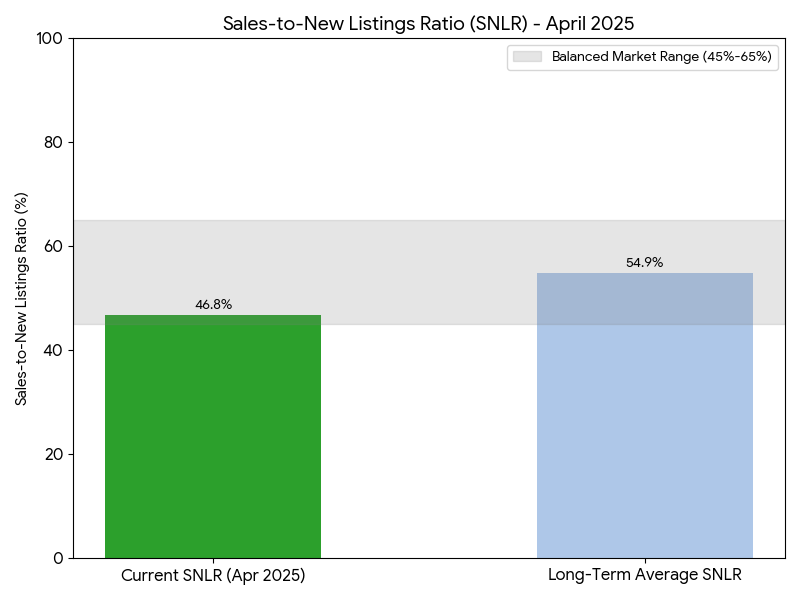

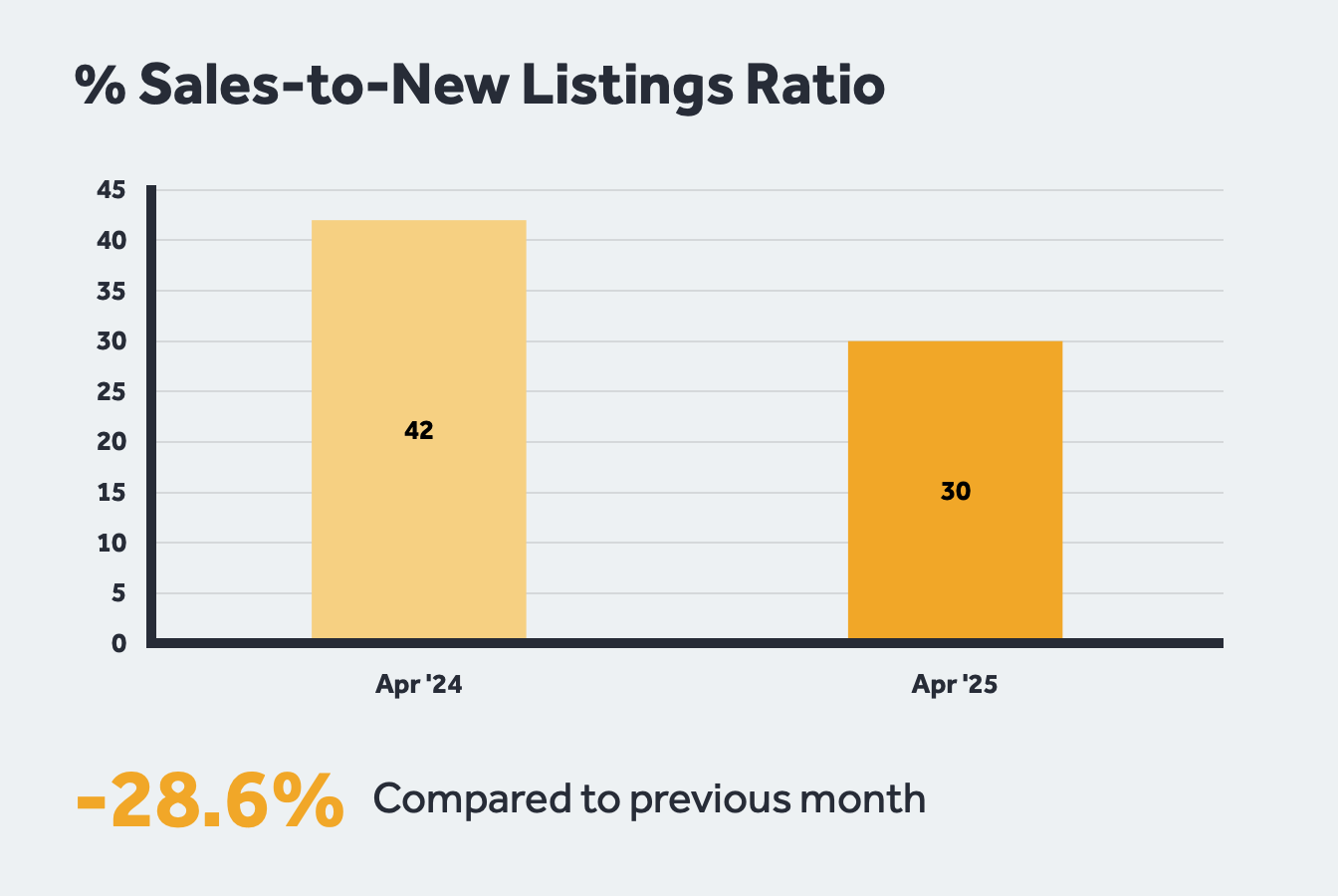

Sales-to-New Listings Ratio (SNLR): 46.8% (up slightly from 46.4% in March). This indicates a market approaching balanced conditions, though still at the lower end of the 45%-65% range typically associated with balance. The long-term average for the SNLR is 54.9%.

Months of Inventory: 5.1 months, which is in line with the long-term average of five months. A seller’s market is typically below 3.6 months, and a buyer’s market above 6.4 months.

Detailed Analysis:

The April 2025 data suggests a stabilization in sales activity after several months of decline. Shaun Cathcart, CREA’s Senior Economist, noted that the market is returning to the “quiet markets we’ve experienced since 2022,” with factors like “tariff uncertainty taking the place of high interest rates in keeping buyers on the sidelines.”

While sales activity paused its descent on a month-over-month basis, the year-over-year comparison still shows a significant drop, indicating that the market is considerably cooler than in April 2024. Price pressures continue, with both the MLS® HPI and the national average sale price registering year-over-year declines.

The month-over-month decrease in the HPI suggests that price adjustments are ongoing. The number of newly listed propertiesdipped slightly in April compared to March. However, the total number of homes available for sale has increased notably from a year ago, offering more choice to potential buyers.

Despite this increase, total inventory remains below long-term averages. The sales-to-new listings ratio moving slightly up to 46.8% and 5.1 months of inventory suggest the national market is largely balanced, albeit with regional variations. Regional Variations: The national figures mask significant regional differences. CREA reports indicate:

Ontario and British Columbia: These more expensive markets are generally experiencing larger price pullbacks and higher inventory levels, with sales potentially decreasing more significantly.

Maritimes, Quebec, Manitoba, and Saskatchewan (Prairies, East Coast): These traditionally more affordable regions are seeing some price resilience or even increases, along with tighter inventory conditions.

Valérie Paquin, CREA Chair, emphasized this divergence: “The number of homes for sale across Canada has almost returned to normal, but that is the result of higher inventories in B.C. and Ontario, and tight inventories everywhere else.” Visual Summary: The following charts illustrate some of the key trends: Total Active Listings vs. Long-Term Average (April 2025) This chart compares the total number of homes available for sale at the end of April 2025 against the typical long-term average for that time of year. It also notes the year-over-year change in active listings. This chart compares the total number of homes available for sale at the end of April 2025 (183,000, up 14.3% year-over-year) against the typical long-term average for that time of year (approximately 201,000). It shows that while listings have increased from last year, they still haven’t reached the historical average for April. Sales-to-New Listings Ratio (SNLR) – April 2025 This chart shows the SNLR for April 2025, comparing it to the long-term average and the thresholds for different market conditions (buyer’s, balanced, seller’s).

This chart shows the Sales-to-New Listings Ratio (SNLR) for April 2025 at 46.8%. It compares this to the long-term average SNLR of 54.9% and highlights the range typically considered a “balanced market” (45% to 65%). The current SNLR sits at the lower end of this balanced range, indicating that while the market isn’t strongly favouring buyers or sellers, it’s leaning slightly towards conditions that could offer buyers more leverage than if the ratio were higher.

Analysis:

April 2025 data points to a stabilization in sales activity following several months of declining figures. According to CREA’s Senior Economist, Shaun Cathcart, “the 2025 Canadian housing story would best be described as a return to the quiet markets we’ve experienced since 2022, with tariff uncertainty taking the place of high interest rates in keeping buyers on the sidelines.”

This suggests that while the sharp decline in sales may have paused, underlying caution persists among market participants. The year-over-year decrease in home sales by nearly 10% underscores that the market remains significantly cooler than in the spring of 2024. This slowdown in activity is accompanied by ongoing price adjustments.

Both the MLS® HPI and the national average sale price saw year-over-year decreases, with the HPI also declining month-over-month, indicating continued downward pressure on home values. On the supply side, new listings saw a slight dip from March to April. However, the total number of homes available for sale has risen substantially compared to the previous year, giving prospective buyers more options.

Despite this increase, overall inventory levels have not yet reached their long-term averages for this time of year. The national market, as indicated by the SNLR and months of inventory, appears to be in a state of balance. However, this national picture is an aggregation of varied local conditions. Regional Variations: The Canadian housing market is not monolithic, and significant regional differences persist:

Ontario and British Columbia: These provinces, particularly their more expensive urban centers, are generally experiencing more pronounced price pullbacks. Inventory levels are higher, and sales activity has seen more significant declines compared to other parts of the country.

Prairie Provinces (Alberta, Saskatchewan, Manitoba) and Atlantic Canada (Maritimes, Newfoundland and Labrador), and Quebec: In contrast, many markets in these regions are demonstrating more resilience. Some are even witnessing modest price growth and continue to experience tighter inventory conditions relative to demand.

CREA Chair Valérie Paquin highlighted this disparity, stating, “The number of homes for sale across Canada has almost returned to normal, but that is the result of higher inventories in B.C. and Ontario, and tight inventories everywhere else.” This underscores the importance of understanding local market dynamics when considering buying or selling property. Visual Summary of Key Market Indicators: The following charts provide a visual representation of some of the key changes in the Canadian housing market for April 2025: Canadian Housing Market – Year-over-Year Changes (April 2025 vs April 2024) This chart illustrates the percentage change in actual home sales, the MLS® Home Price Index, and the national average sale price compared to April of the previous year. All key metrics show a decline, highlighting the cooling trend. Canadian Housing Market – Month-over-Month Changes (April 2025 vs March 2025)

This chart displays the percentage change in seasonally adjusted national home sales, new listings, and the MLS® Home Price Index compared to the preceding month. It shows a near flatline in sales, a slight decrease in new listings, and a continued modest decline in the HPI. In conclusion, the Canadian housing market in April 2025 was characterized by a pause in the recent sales slump, ongoing price moderation, and a nationally balanced market that masks significant regional variations. Factors such as economic uncertainty, including trade tariff concerns, continue to influence buyer and seller behavior.

The decision to sell your home is significant, and the current market presents a nuanced landscape. While national prices have seen some moderation and sales activity, though stabilizing month-over-month, remains below last year’s levels, there are compelling reasons to consider listing, especially if your circumstances align. Why This Might Be a Good Time for You to Sell:

Stabilizing Market Activity: After a period of decline, national sales activity showed signs of pausing its slump in April. This could indicate that buyers who were on the sidelines are beginning to re-engage, potentially creating a window of opportunity before any further significant market shifts.

Inventory Levels Offer a Mixed Picture: While total active listings are up year-over-year (meaning more competition than last year), they still remain below the long-term average for this time of year in many areas. A well-priced and well-presented home can still capture significant attention.

Regional Strengths Persist: If your property is located in markets like the Prairies, Quebec, or parts of Atlantic Canada, you might find conditions are still relatively strong with resilient pricing and tighter inventories. Even in markets like Ontario and BC that have seen more significant price adjustments, unique properties in desirable locations can still attract motivated buyers.

Capture Current Price Levels: While prices have dipped from their peak, they are still substantial in many regions compared to historical levels. If you’re concerned about further price erosion, selling now could allow you to lock in your property’s current value. Waiting doesn’t guarantee a better outcome, especially if national price trends continue their modest decline.

Motivated Buyers Are Still Active: Serious buyers are always in the market. Those active now are likely navigating current conditions with clear intentions, potentially leading to smoother transactions if you connect with the right one.

To maximize your success, it’s crucial to:

Price Strategically: Overpricing in this market can lead to your home sitting longer. Work closely with a local real estate professional to set a competitive and realistic price based on the very latest comparable sales.

Ensure Your Home Shines: With more choice for buyers than last year, presentation matters more than ever. Invest in staging, decluttering, and addressing any necessary repairs.

Be Flexible: Understand that negotiation might be more common. Being open to reasonable offers and conditions can facilitate a successful sale.

If your personal and financial goals align with a move, listing now allows you to capitalize on the current buyer interest and potentially transition to your next property with more clarity than in a more volatile market.

For prospective homebuyers, the April 2025 market data reveals an environment that offers several advantages compared to the frenetic conditions of the recent past. If you’re financially prepared, this could be an opportune time to make your move. Why This Might Be a Good Time for You to Buy:

Increased Choice and Less Frenzy: The 14.3% year-over-year increase in total active listings means you have more properties to choose from. With national sales down 9.8% compared to last April, there’s generally less competition for each home, reducing the likelihood of intense bidding wars.

Price Moderation Offers Better Value: Both the MLS® Home Price Index and the national average sale price have declined year-over-year (by -3.6% and -3.9% respectively). This softening of prices can make homeownership more accessible and potentially offer better long-term value.

More Balanced Market Conditions: Key indicators like the Sales-to-New Listings Ratio (46.8%) and Months of Inventory (5.1 months) point towards a more balanced national market. This environment typically affords buyers more time for due diligence, less pressure to make rushed decisions, and potentially more room for negotiation on price and conditions.

Favourable Conditions in Certain Regions: If you are looking in markets like Ontario or British Columbia, you may find more significant price pullbacks and a greater willingness from sellers to negotiate, creating specific buying opportunities.

Opportunity for Long-Term Investment: Housing is a long-term investment. Entering the market during a period of price stabilization or modest decline can be advantageous for buyers with a long-term horizon, as you’re potentially buying at a more sustainable price point.

Stable Interest Rate Environment (Relatively Speaking): While interest rates remain a key consideration, the acute uncertainty around rapid rate hikes has somewhat subsided. This allows for more predictable mortgage planning. Shaun Cathcart of CREA noted “tariff uncertainty taking the place of high interest rates in keeping buyers on the sidelines,” suggesting some buyers might be adapting to the current rate environment.

To make the most of the current market, consider the following:

Get Pre-Approved for a Mortgage: Know your budget definitively. This will strengthen your negotiating position.

Work with an Experienced Buyer’s Agent: They can help you identify suitable properties, understand local micro-market conditions, and guide you through the negotiation process.

Don’t Try to Perfectly Time the Bottom: It’s nearly impossible to buy at the absolute lowest point. Focus on finding a home that meets your needs and budget in a market that is offering more favorable conditions than seen in quite some time.

If you have a stable financial situation and a long-term perspective, the current market conditions provide a window of opportunity to purchase a home with more choice, less pressure, and potentially better value.

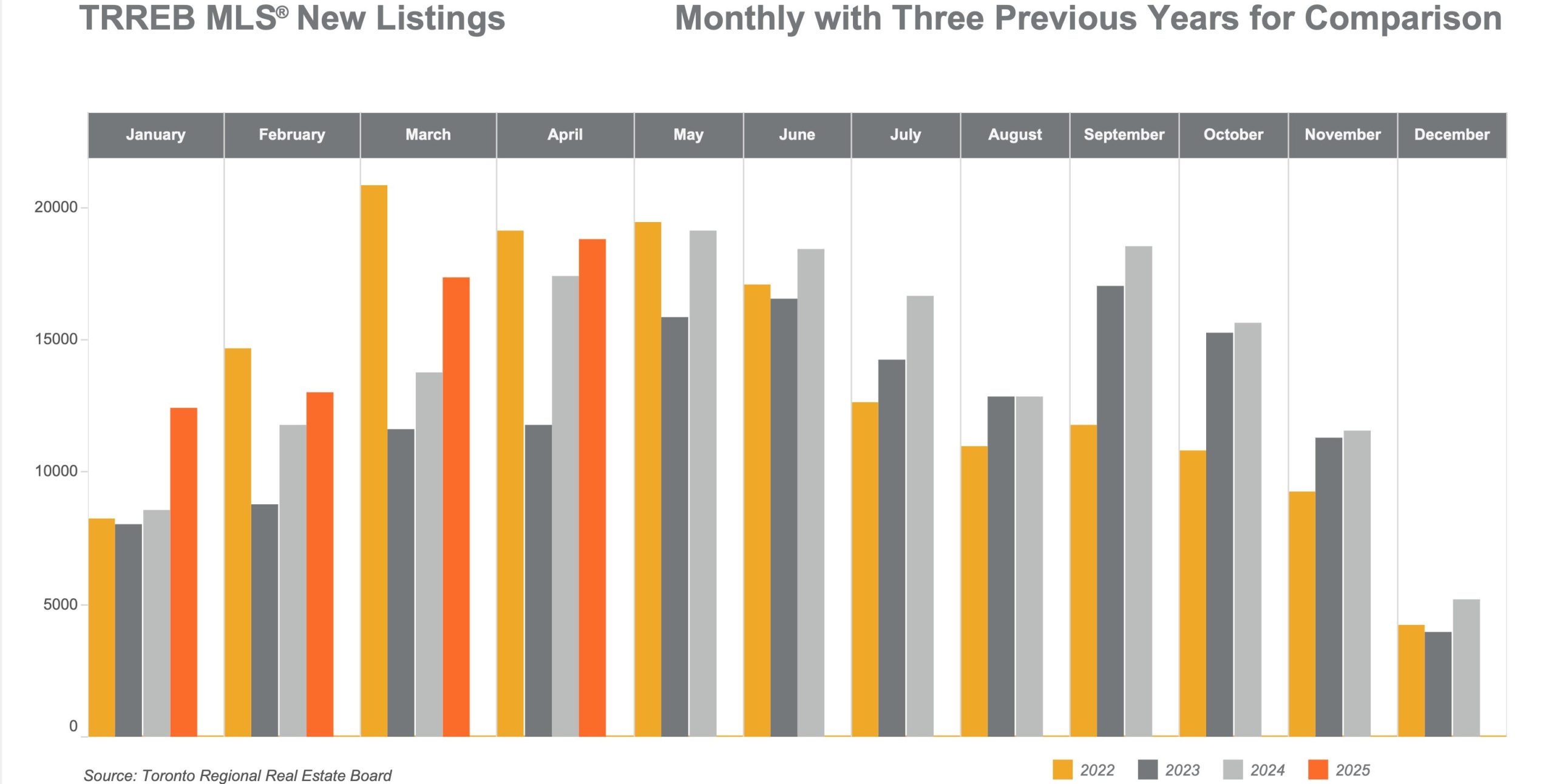

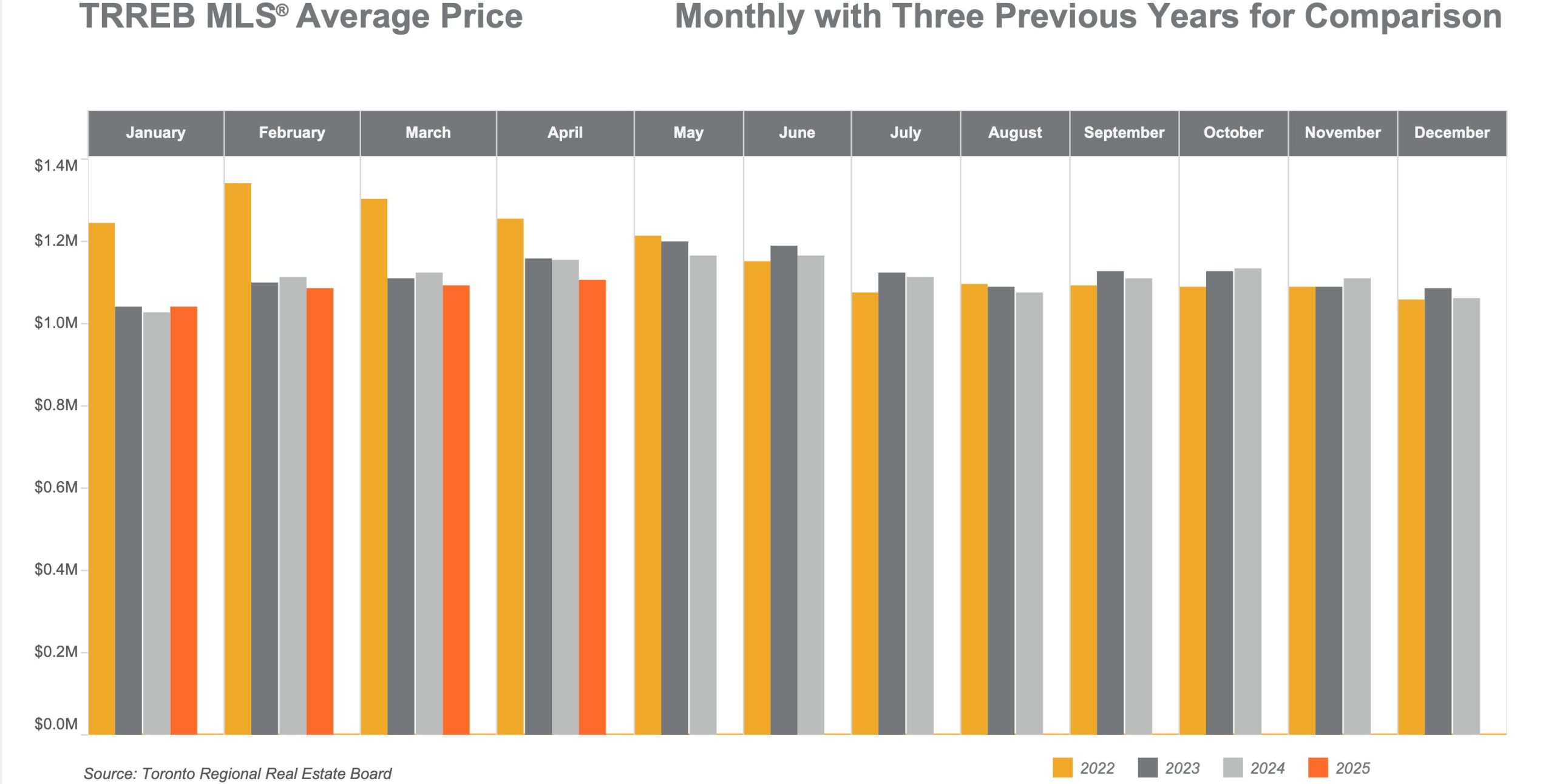

The Greater Toronto Area (GTA) real estate market continued to evolve in April 2025, reflecting broader economic pressures, buyer psychology, and seasonal trends. Whether you’re a homeowner, investor, or first-time buyer, understanding current housing data is critical.

In this article, we break down the latest TRREB Market Watch statistics, offer insight into price fluctuations, sales activity, and what this all means for your next move in the real estate market.

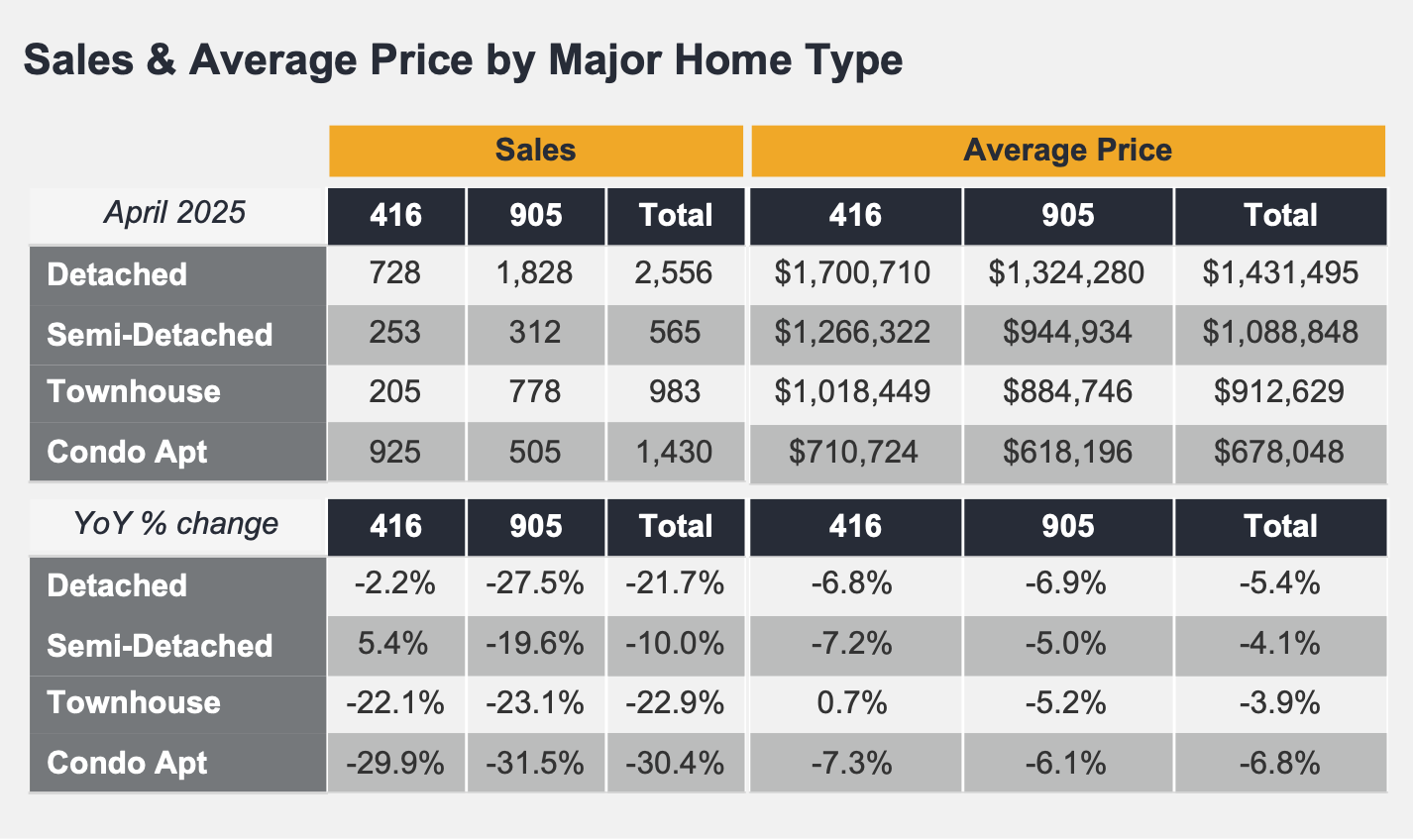

Here’s a detailed look at real estate sales and prices by home type across the 416 (Toronto) and 905 (suburban) areas.

📊 Sales & Average Price by Property Type

Type

Sales

(416)

Sales

(905)

Total

Sales

Avg Price

(416)

Avg Price

(905)

Detached

1,430..

2,556..

3,986..

$1,431,495..

$1,324,280..

Semi-Detached.

505

778

1,283

$1,088,848

$944,934

Townhouse

312

925

1,237

$912,629

$884,746

Condo Apt

983

728

1,711

$678,048

$618,196

💬 Year-over-Year Price Change by Property Type

Detached: -6.9%

Semi-Detached: -5.0%

Townhouse: -5.2%

Condo Apartment: -6.1%

📉 Across all segments, buyers gained greater leverage due to elevated real estate inventory levels and improved affordability through moderated mortgage rates.

📉 What’s Behind the Dip in Sales?

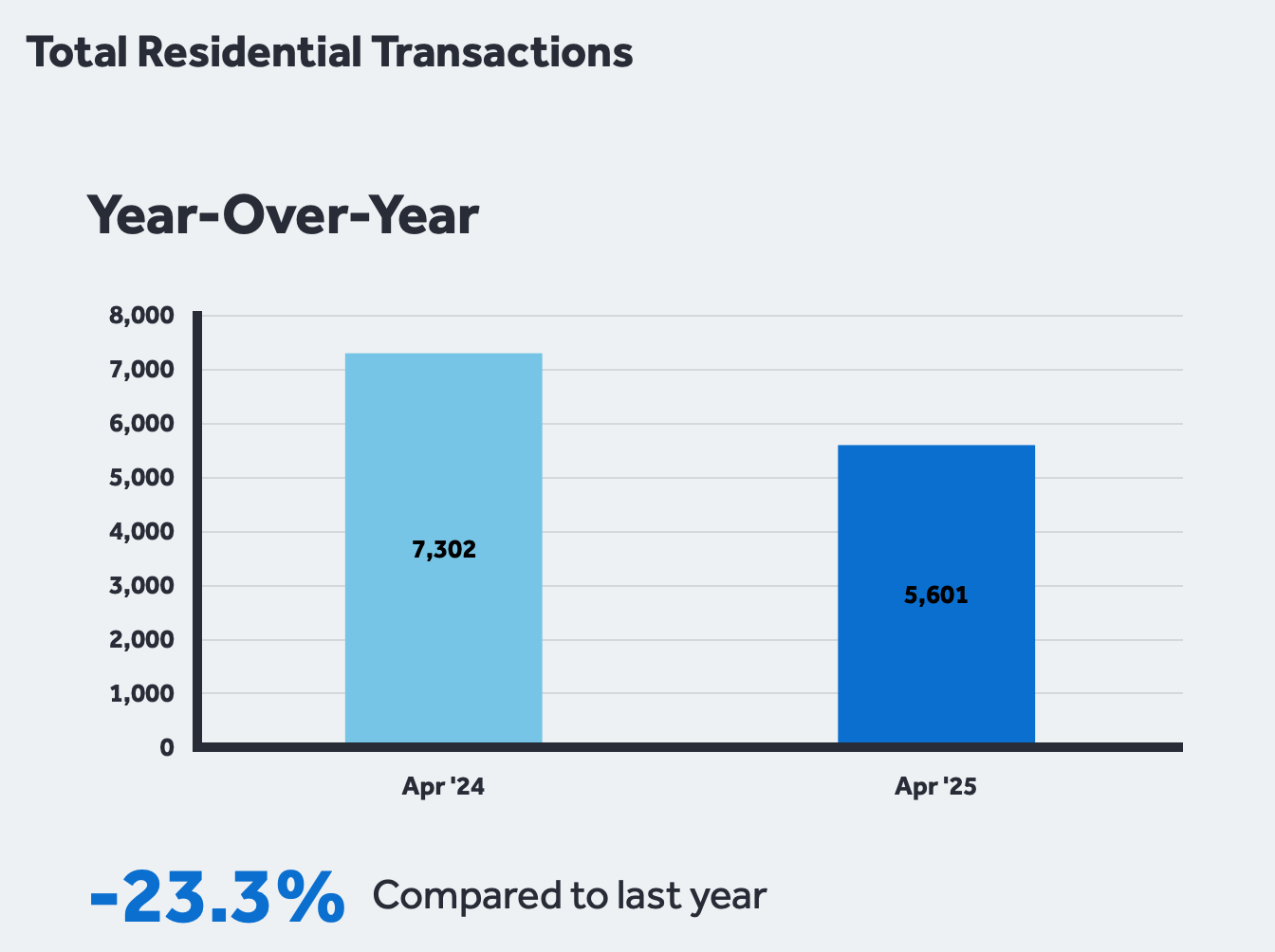

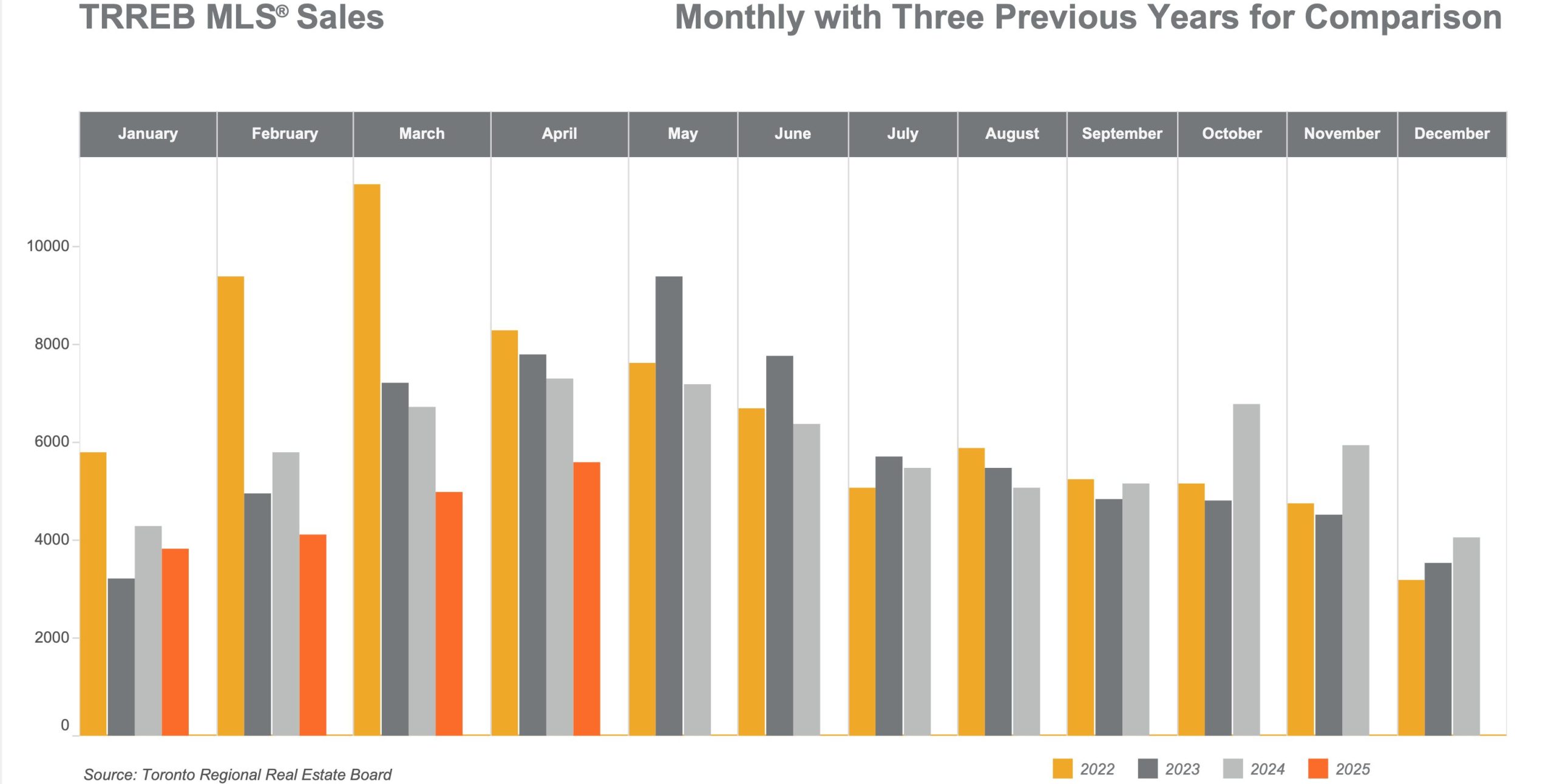

Despite following a typical seasonal uptick from March, April 2025 real estate sales fell 23.3% year-over-year. This hesitation is largely attributed to:

Economic uncertainty: Following the federal election, many are monitoring the Canada-U.S. trade relationship, which may impact consumer confidence.

Improved inventory: Buyers now have more choices, leading to longer decision-making timelines.

📊 Economic Indicators Snapshot

Indicator

Value

Trend

Inflation (CPI YoY)

2.8%(Apr 2025)

↑ from 2.3% Mar

Toronto Unemployment Rate

5.0%(Apr 2025)

↑ from 4.8% Mar

Bank of Canada Overnight Rate

2.750%

↔ steady

Prime Lending Rate

6.45%

↔ steady

5-Year Fixed Mortgage Rate

5.09% avg.

↓ slightly

🌍 Regional Trends: Urban vs. Suburban

The 905 regions (e.g., Durham, York, Peel) showed resilience in price stability while urban centers like Toronto (416) saw sharper price drops, especially in condo segments.

🏙 Toronto (416):

Condos down 6.1%

Detached prices remain highest at $1.43M

🏘 Suburbs (905):

Balanced activity

Greater affordability attracted more buyers despite market cooling

There’s growing demand for properties with some backyard space and/or additional buildings, especially among buyers moving from subdivision homes in City Centers. If you’re thinking of selling and your property fits this profile, now may be the perfect time to connect with qualified buyers.

📈 Chart: TRREB Sales Activity YoY

Real Estate Sales are down, but opportunities are up for savvy buyers and well-prepared sellers.

🤝 Let’s Talk: Free Market Evaluation

If you’re wondering about your home’s value in today’s changing market, I offer a FREE, no-obligation market evaluation that can help you decide if now is the right time to sell.

Whether you’re staying local or heading outside of the city to York Region or Durham Region and the Kawarthas, I can guide your move with real insights and connections to active, qualified buyers.

Summary

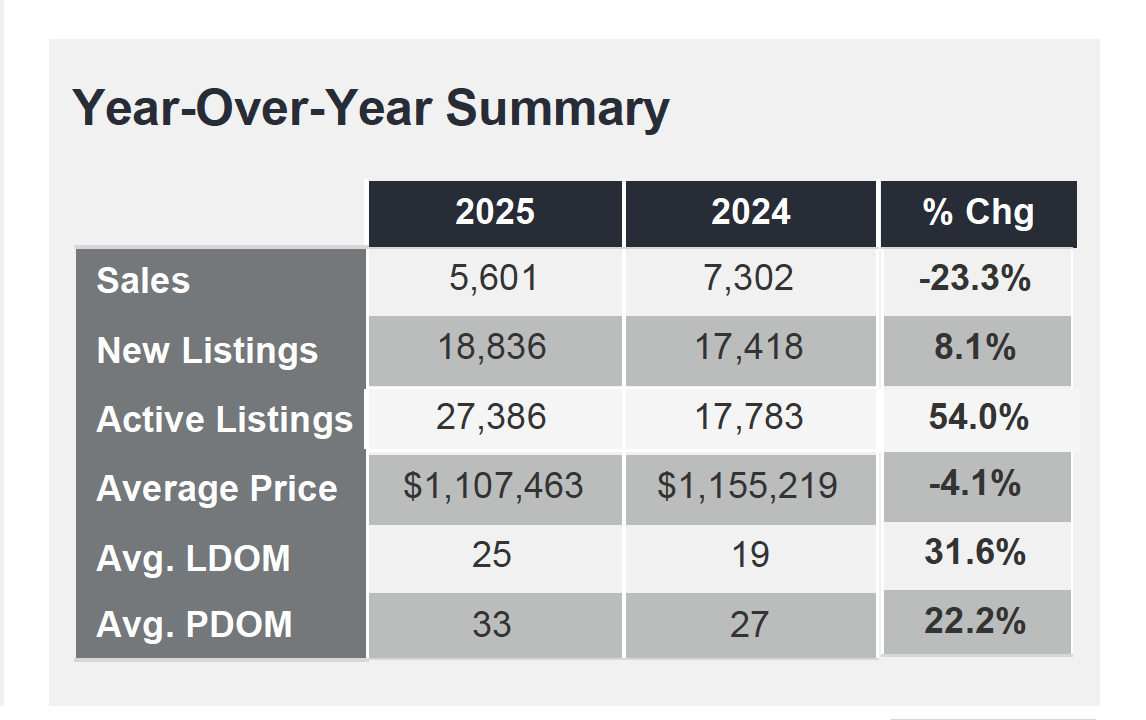

In April 2025, the Greater Toronto Area (GTA) real estatemarket saw a continued seasonal rise in activity from March, but overall real estate sales remained significantly lower than the same period in 2024. TRREB reported a 23.3% year-over-year drop in home sales, with only 5,601 transactions completed.

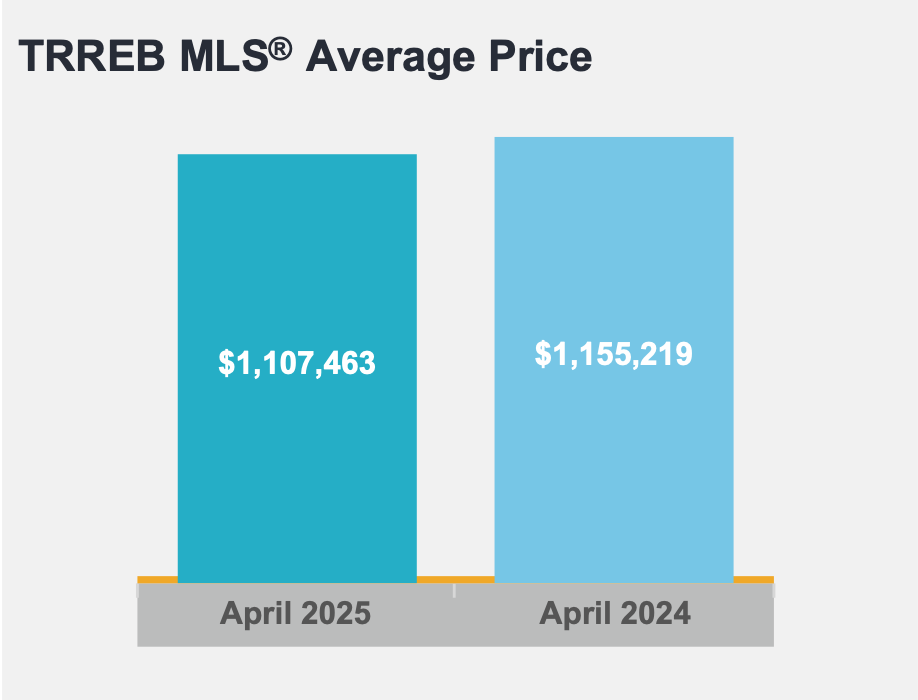

At the same time, new real estate listings rose by 8.1%, providing buyers with greater inventory and more negotiating power. The average home price fell by 4.1% to $1,107,463, while the MLS® Home Price Index Composite dropped 5.4% year-over-year, reflecting buyers’ cautious stance amid high borrowing costs and economic uncertainty following the recent federal election.

Elevated inventory and moderating mortgage rates contributed to more affordable housing options across the GTA. Detached, semi-detached, and condo apartment segments all experienced price declines, with detached homes in the 416 region averaging over $1.43 million.

Meanwhile, broader economic indicators showed continued inflation and employment growth, although real GDP growth remained uneven across timeframes. As households monitor developments in Canada’s trade relations and monetary policy, the GTA market is positioned for possible shifts in buyer sentiment should confidence improve and borrowing conditions ease.

Sales are lower largely due to buyer hesitation around high interest rates and economic uncertainty following the recent federal election and the ongoing trade war.

2. Is this a good time to buy real estate in the GTA?

Yes, if you’re financially ready. There’s less competition and more choice, giving buyers leverage in negotiations.

3. How can I make my home more attractive to buyers?

Highlight key features such as land, workshops, finished basements, or upgrades. Price competitively and stage professionally.

4. What’s the best area within an hour or two of Toronto to find land with buildings?

Areas north and east of York Region and Durham Region —such as Uxbridge, Clarington, Georgina, Brock, and parts of Kawartha Lakes—are growing in popularity among buyers looking for space and utility.

It gives you an accurate sense of your home’s current market value, helping you plan with confidence. No strings attached.

📝 Final Thoughts

The GTA housing market is shifting, but with the right guidance, you can take full advantage of today’s conditions—whether you’re buying your dream rural property or selling your urban home.

📩 Let’s connect to discuss your goals and how I can help you navigate the market confidently.

Thinking about selling your rental or secondary property? Before you do, it’s critical to understand how capital gains tax can affect your bottom line. This guide explains what you need to know, what’s changed, and how to plan ahead.

Capital Gains in Canada: What Real Estate Investors Need to Know

Thinking about selling your rental or secondary property? Before you do, it’s critical to understand how capital gains tax can affect your bottom line. This guide explains what you need to know, what’s changed, and how to plan ahead.

Capital gains taxation is an important consideration for property owners and investors across Canada, particularly those holding secondary residences and rental properties.

Understanding how capital gains work, the implications for your tax obligations, and how strategic planning can mitigate liabilities is essential for making informed financial decisions.

What Are Capital Gains?

Capital gains occur when an asset, such as real estate, is sold for more than its adjusted cost base (ACB), which includes the purchase price plus certain costs like legal fees, renovations, and selling expenses.

In Canada, 50% of a capital gain is taxable and added to the seller’s income for the year. This is known as the capital gains inclusion rate.

For instance, if a property is sold for $1 million and the ACB is $600,000, the gain is $400,000, of which $200,000 would be taxable.

The Impact on Real Estate, Including Rental Properties

The principal residence exemption allows homeowners to shelter the full capital gain from tax if certain criteria are met.

However, secondary residences and rental properties do not qualify for this exemption.

When selling a rental property, the taxable portion of the gain is added to your total income, potentially pushing you into a higher tax bracket.

Additionally, if Capital Cost Allowance (CCA) was claimed on the property to offset rental income, a portion of that may be recaptured and taxed as income, not a capital gain.

This creates a tradeoff between the benefit of reducing taxes annually versus facing higher taxes upon sale.

Balancing Timing and Tax Efficiency

One of the key challenges for property owners is timing the sale of a secondary property. Selling in a year when your other income is lower can reduce the overall tax impact.

Conversely, selling during a high-income year could significantly increase your marginal tax rate, resulting in a larger tax bill.

Tax planning strategies can help balance this tradeoff:

Deferring the sale to a year with lower income

Using capital losses to offset gains

Transferring ownership to a spouse in a lower tax bracket (with caution, due to attribution rules)

These strategies highlight the importance of personalized tax planning, particularly when dealing with sizable capital assets like real estate.

Looking Ahead: Potential Tax Changes

In the 2024 federal budget, the government announced its intention to increase the capital gains inclusion rate from 50% to 66.67% for gains over $250,000, effective January 1, 2026.

This would have had significant implications for investors holding high-value assets, especially real estate.

The proposed change introduced further complexity, requiring even more careful consideration of timing and asset disposition.

This decision has been welcomed by many in the investment and real estate sectors, as it preserves the current planning frameworks and alleviates concerns of increased tax burdens on large asset sales.

Real-World Example

Consider a scenario where an Ontario investor sells a secondary rental property for $1 million in 2025.

The original purchase price was $500,000, with $50,000 in eligible improvements and $40,000 in selling expenses, bringing the adjusted cost base to $590,000.

The capital gain is $410,000, and 50%—or $205,000—is taxable. Assuming the seller falls into the 33% marginal tax bracket, the tax owing on the gain could be approximately $67,650.

Had the proposed inclusion rate increase to 66.67% been implemented in 2026, the taxable portion would have been $273,347, with an estimated tax burden closer to $90,000—illustrating the significant impact such a policy change could have had.

Making Informed Decisions

The decision to sell a secondary residence or rental property in Canada carries notable tax consequences. Capital gains tax, while only applied to 50% of the gain (for now), can substantially affect your net proceeds. Properly accounting for selling expenses, potential CCA recapture, and the timing of the sale are all vital to reducing your tax liability.

For real estate investors, the key lies in understanding how the rules apply, what tradeoffs exist, and how to plan effectively. Working with a financial advisor or tax professional can help navigate these complexities, ensuring that your investment decisions align with both your financial goals and the tax landscape.

Need personalized guidance?Contact Gerald Lawrenceto book a private consultation and learn how to maximize your returns when selling investment properties.

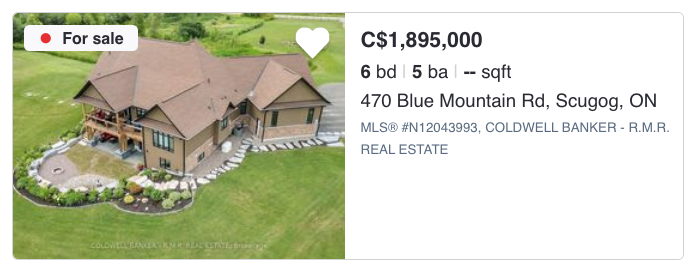

Detached Properties For Sale UNDER $500,000 Canadian Dollars in the GTA

Detached homes priced under $500,000 in the Greater Toronto Area (GTA) are becoming increasingly scarce, yet they offer an exceptional opportunity for savvy buyers. In a market where the average detached property often costs well over $1 million, finding homes at this price point seems like a dream come true. However, these homes typically come with unique characteristics—many are fixer-uppers, stigmatized properties, estate sales, power of sale listings, or are deliberately priced low to ignite competitive bidding wars.

Despite these complexities, more than 30 such properties are currently listed across the GTA. The majority of these homes are found in Oshawa, Georgina, and Clarington—particularly in Newcastle and Bowmanville. Other regions like Brock, Scugog, Toronto, and Halton host only a handful of listings. Most are 2-bedroom bungalows, with some including 2 bathrooms, while the smaller group of 3-bedroom homes is split between those with 1 or 2 bathrooms.

Below, we break down the types of properties typically found in this price range, including their advantages, disadvantages, and potential caveats you should be aware of before making a purchase.

1. Fixer-Uppers

Fixer-uppers are homes in need of renovation or repair, often priced lower to reflect the investment required to bring them up to modern standards.

Financing can be trickier as lenders may demand repairs upfront

Caveats: Many of these homes will require detailed property condition disclosures. Always opt for a home inspection, even if it’s waived contractually, and budget for surprises.

2. Stigmatized Properties

These are homes where a death, crime, or other psychologically impactful event occurred, which may deter some buyers.

Advantages:

Significantly reduced price

Less competition from other buyers

Disadvantages:

Potential difficulty reselling in the future

Emotional discomfort depending on the situation

Caveats: In Ontario, sellers aren’t always legally required to disclose stigmas unless directly asked. It’s wise to conduct your own research or work with a local realtor who knows the history of the area.

3. Estate Sales

An estate sale occurs when the owner has passed away and their estate is selling off the home, often as-is.

Advantages:

More room for negotiation with motivated sellers

Can be priced below market to ensure a quick sale

Disadvantages:

Typically sold “as-is,” with no updates or repairs

Probate processes can delay closing

Caveats: There may be limited documentation on the property’s history, and disclosure can be minimal. You may also need to work through legal intermediaries rather than traditional sellers.

4. Power of Sale Properties

These occur when lenders seize and sell homes after mortgage defaults.

Advantages:

Priced below market value for a fast sale

Quicker closing processes in many cases

Disadvantages:

Sold without warranty or guarantee of condition

Minimal negotiation leverage

Caveats: Lenders are legally obligated to disclose any known defects, but they may not know much about the property’s condition. Buyers must conduct thorough due diligence and often accept “as-is” terms.

5. Deliberately Underpriced Listings for Bidding Wars

Some properties are intentionally priced below market value to spark a bidding war.

Advantages:

May appear to be a great deal at first glance

Occasionally, buyers snag a win if competition is low

Disadvantages:

Final sale price often exceeds listing price

Pressure to waive conditions (like inspections or financing) to stay competitive

Caveats: Fast-paced offers leave little time for proper evaluation. This high-pressure environment can lead to overpaying or skipping essential steps like due diligence.

Where These Properties Are Found

Let’s take a look at where the bulk of these listings are appearing (as at the time of this blog article):

The overwhelming majority are 2-bedroom homes, some with two bathrooms. Three-bedroom options are limited, and only half of those offer a second bathroom.

Who’s Buying These Properties?

Given their affordability and potential for future value, these listings are drawing attention from a range of buyers:

Contractors looking to flip or rebuild

Investors eyeing rental returns

First-time homebuyers seeking an entry point into the market

Landlords expanding their rental portfolios

Because of the heightened interest and reduced inventory, these homes don’t tend to last long on the market. In some cases, properties receive multiple offers within just a few days.

Important Disclosures and Legal Considerations

It’s essential to understand that many of these properties come with specific disclosure requirements. You may encounter:

Property-related disclosures: Structural issues, previous damages, or material latent defects.

Legal disclosures: Probate timelines, rights of way, and power of sale regulations.

Lender disclosures: For power of sale homes, lenders often provide limited information.

Buyers should always consult a qualified real estate agent and legal professional before proceeding. A property inspection, title search, and review of the seller’s disclosures are critical steps you shouldn’t skip.

👉 Click here or leave your email to receive a curated list of available properties, complete with photos, descriptions, and neighbourhood insights—delivered directly to your inbox.

These listings move fast—don’t miss your chance to grab a home in this rare price bracket!

Canada is one of the most immigrant-friendly countries in the world, and Ontario, being its most populous province, is often the first stop for newcomers. But buying a home or condo in Ontario-especially if you’re new to Canada or returning after time abroad-can feel like navigating a maze. Fortunately, it’s not only doable, but with the right guidance, it can also be smooth, strategic, and exciting. In this comprehensive guide, we’ll walk you through the entire home-buying journey-from understanding your eligibility as a non-citizen, to landing the keys to your first Canadian property. Along the way, you’ll gain insider tips, explore available resources, and learn how to avoid the common pitfalls many immigrants and expats face. Whether you’re a permanent resident, skilled worker, international student, or a Canadian returning from abroad, this article is for you.

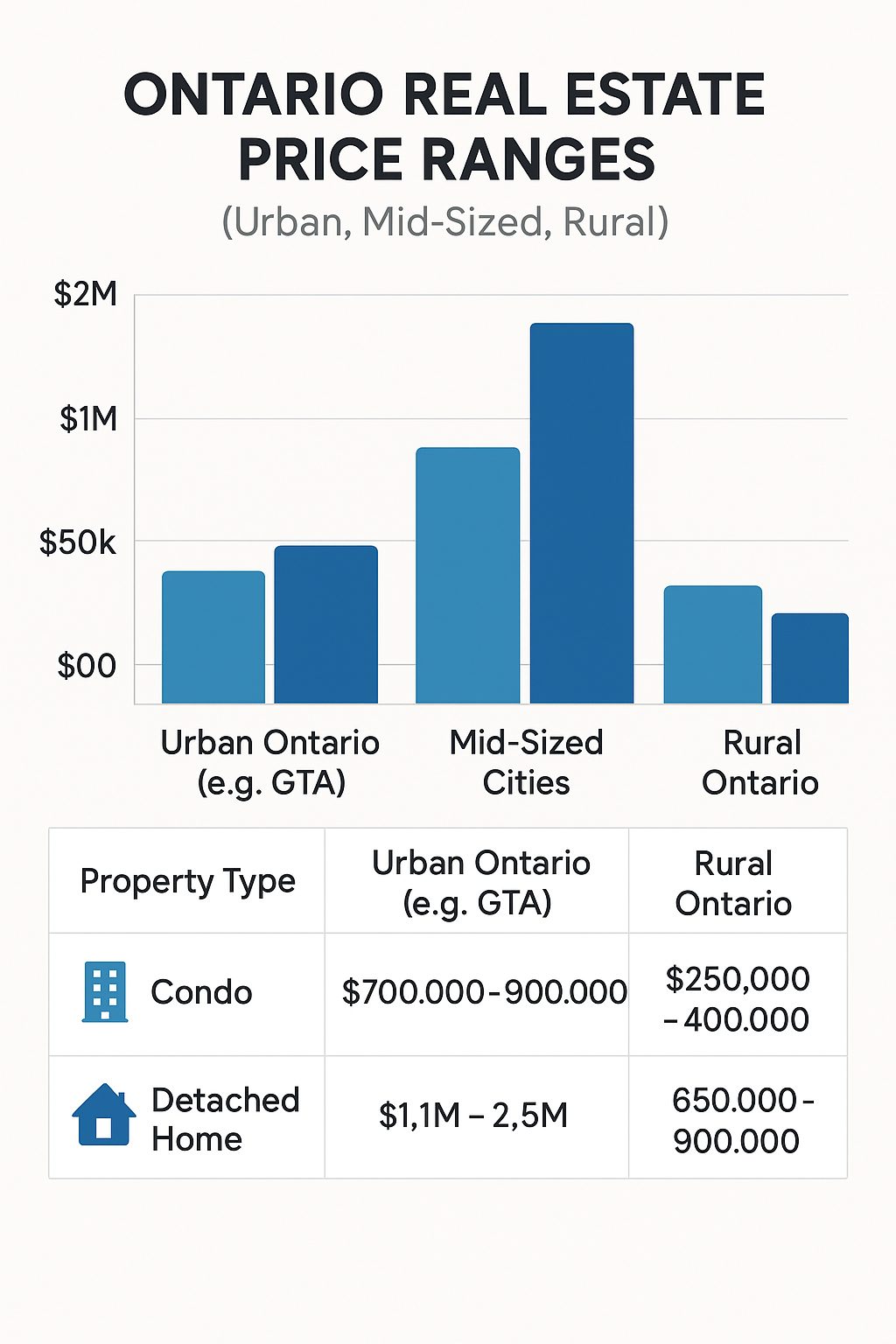

Understanding the Canadian Real Estate Market

Before diving into the home-buying process, it’s essential to understand Ontario’s real estate environment. Key Market Trends (2024):

Ontario’s market has experienced high demand driven by immigration, limited supply, and low-interest periods. Whether you’re buying for your family or investing long-term, knowing local prices helps you plan smarter.

Key Housing Types in Ontario

Detached Homes: Ideal for families needing more space. Comes with land and higher taxes.

Condos: Popular among newcomers due to lower maintenance. Great in city centers.

Townhouses: A middle ground-affordable, moderately spacious, and often part of planned communities.

Tip:Condos in Toronto or Ottawa are often the starting point for immigrants due to convenience, cost, and lifestyle perks.

Do Immigrants Need Citizenship to Buy Property?

Short answer: No. Anyone can buy property in Canada, regardless of immigration status. But, if you’re a non-resident, you may face:

Ontario charges 25% tax on property purchases in designated areas by foreign nationals. However, you may be exempt if:

You’re a permanent resident

You’re a Canadian citizen returning home

You apply for a rebate after obtaining PR

Always consult a real estate lawyer about your tax position.

Working with Real Estate Professionals in Ontario

1. Realtor: Helps you find, negotiate, and close the deal 2. Mortgage Broker: Finds you the best rate-even with limited Canadian credit 3. Lawyer: Handles title transfer, tax forms, and legal review Ask if they have experience working with newcomers or expats. It can save you thousands and plenty of stress.

Step-by-Step Buying Process in Ontario

Step

Description

Pre-Approval

Secures your buying power

Home Search

Online listings, open houses

Offer & Negotiation….

Make a conditional offer

Home Inspection

Professional assessment of condition

Final Financing

Mortgage locked in

Legal Closing

Lawyer finalizes paperwork

Key Transfer

Move-in day!

Conditional Offers: Why They Matter

Newcomers often skip inspections or financing conditions due to urgency. That’s risky. Protect yourself by including:

Financing condition (5 days)

Inspection clause

Lawyer review

Even in a hot market, a bad deal is worse than no deal.

What if You’re Still Abroad?

Buying remotely is possible with:

Digital signings (DocuSign)

Video showings

Power of attorney

Remote lawyer services

This is especially useful for returning expats planning months in advance.

❌ Overextending your budget ❌ Trusting one agent without checking credentials ❌ Skipping due diligence ❌ Not understanding local bylaws, condo rules, or neighborhood dynamics

Post-Purchase To-Do List

Set up utilities: Hydro, Gas, Internet, Waste pickup

Apply for municipal taxes: Your lawyer usually registers this

Insurance: Home, contents, and liability insurance

Join the community: Local libraries, schools, healthcare, and social clubs

Real Stories from Newcomers

“We bought our first condo in Mississauga after just 8 months in Canada. Our realtor explained everything, and the mortgage broker worked miracles with my international income.” – Arjun & Priya from India“I moved back after 12 years in the UAE. It felt overwhelming at first, but I got a great townhouse in Ottawa. Don’t underestimate the paperwork!” – Linda, Returning Canadian Expat

FAQs

Can immigrants buy homes in Canada without PR? Yes! Even temporary visa holders can purchase, though financing and taxes may differ.

What is the Non-Resident Speculation Tax? An extra 25% tax for foreign buyers in parts of Ontario-rebate possible after PR.

Are expats returning to Canada considered non-residents? Sometimes. You may be treated as a non-resident until you re-establish ties like income or address.

Do I need a job in Canada to qualify for a mortgage? Typically yes, or proof of sufficient income abroad with proper documentation.

Can I buy a home while living abroad? Absolutely, using remote tools and professionals like lawyers and realtors.

How long does the process take? Generally, 2-3 months from mortgage pre-approval to closing.

Conclusion: Your Next Chapter Starts Here

Buying a home or condo in Ontario as an immigrant or expat isn’t just a financial decision-it’s an emotional milestone. It means stability. It means roots. It’s the first brick in your Canadian dream. With planning, the right team, and this roadmap, you’re more than ready to take that step. Download Our Free Checklist:Home Buying Guide for Immigrants & Expats in Ontario

Relocating to a new country comes with its own share of exciting opportunities and practical challenges. One of the most crucial tasks for any newcomer to Canada is learning how to build Canadian credit as a newcomer. Your credit score can open doors—or close them. From getting your first apartment to financing your future home, your credit history is a powerful tool in your new life.

So, how can you, as a newcomer with no Canadian credit history, build a strong credit score from scratch? It’s easier than you think—but only if you take the right steps from the beginning.

Understanding the Canadian Credit System

Before you can build credit, you need to understand what it is. In Canada, your credit report is a detailed record of how you’ve used credit over time, while your credit score is a number that summarizes your creditworthiness. The higher the score (which ranges from 300 to 900), the better.

There are two major credit bureaus in Canada: Equifax and TransUnion. They collect and maintain your credit information, and you have the right to request your credit report from both for free.

Why Credit History Matters in Canada

In Canada, your credit history influences more than just your ability to borrow money. It can affect:

Rental approvals

Employment offers

Insurance rates

Interest rates on loans

Having no credit is almost as limiting as having poor credit, so building it should be a priority.

Get Started: Apply for a SIN and Bank Account

Your Social Insurance Number (SIN) is your gateway to almost all financial activity in Canada. Get it as soon as possible, then open a Canadian bank account. Many banks offer newcomer packages that include low-fee accounts and advice tailored to immigrants.

Get a Secured Credit Card

This is the single most recommended tool for newcomers. A secured credit card requires you to put down a refundable deposit that acts as your credit limit. As you use the card and make payments on time, your credit score begins to build. Some of the best providers for secured cards include:

Capital One Guaranteed Mastercard

Home Trust Secured Visa

Neo Financial Secured Card

Become an Authorized User

If you have a trusted family member or friend with good credit, ask them to add you as an authorized user on their credit card. Their positive history will help build your own, though not all lenders report authorized user activity—check first.

Try a Credit Builder Loan

A credit builder loan is like a savings plan that builds your credit. You “repay” the loan monthly, but the funds are held in a locked savings account until the term ends. Once done, you receive the full amount, and your positive payment history is reported to the credit bureaus.

Always Pay On Time and Keep Balances Low

Credit scoring models heavily favor on-time payments and low credit utilization (ideally under 30%). Even one late payment can lower your score significantly.

Use autopay features or calendar reminders to stay on top of your bills.

Check Your Score Regularly

Knowing your score is half the battle. You can check your Canadian credit score and report for free using tools like:

Credit Karma Canada

Borrowell

Equifax/TransUnion (annually)

Avoid These Common Mistakes

Newcomers often fall into traps such as:

Applying for too many credit products at once

Maxing out credit cards

Closing old accounts too soon

Avoid these, and your score will rise steadily.

Use Utility and Cell Phone Bills to Your Advantage

Some services now allow you to report on-time utility or cell phone payments to credit bureaus. Look into programs like Rent Advantage or KOHO Credit Building for this purpose.

Keep Building Over Time

Building credit is a marathon, not a sprint. Keep your accounts open, diversify your credit types, and stay consistent. In time, you’ll be eligible for lower-interest loans, better credit cards, and larger financial opportunities.

Frequently Asked Questions

How long does it take to build credit in Canada as a newcomer? With consistent habits, you can begin seeing a credit score in as little as 3 to 6 months. A good score typically takes 12+ months to develop.

Can I transfer my credit history from my home country to Canada? Usually no. Canadian credit bureaus do not recognize international credit history. You must start fresh.

Do all landlords and employers check credit scores in Canada? Not all, but many do—especially in major cities. A good credit score boosts your credibility.

Is a credit score of 650 good in Canada? Yes, 650 is considered fair. A score above 700 is good, and 750+ is excellent.

Will checking my credit score lower it? Not if you use soft checks like Borrowell or Credit Karma. Hard inquiries from loan or card applications can lower it slightly.

What’s the best first credit card for newcomers in Canada? The Home Trust Secured Visa and Neo Secured Card are great starters. Look for cards with low fees and no income requirements.

Conclusion

Building credit in Canada as a newcomer isn’t just possible—it’s highly achievable with the right knowledge and tools. By starting with secured cards, making timely payments, and using tools designed for immigrants, you can build a strong financial foundation that supports your new life in Canada.

Remember, your credit score is a reflection of your financial habits. Keep them clean, consistent, and controlled, and the opportunities in your new homeland will follow.

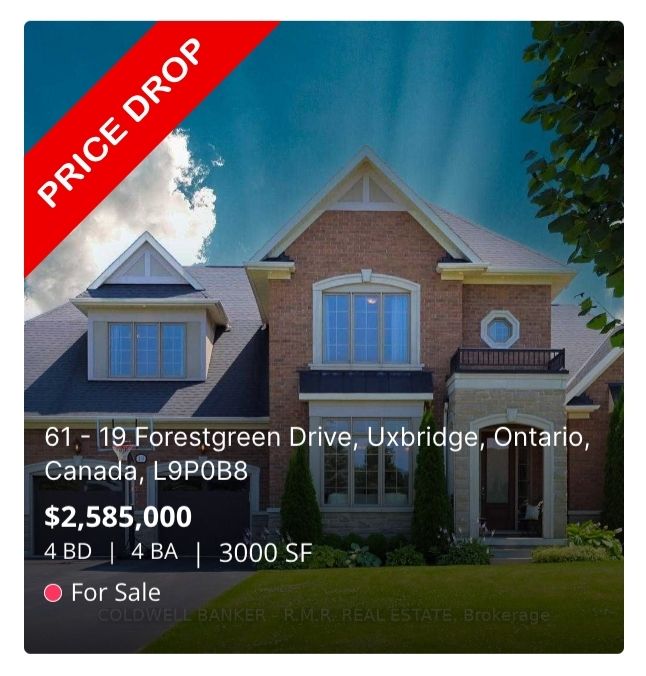

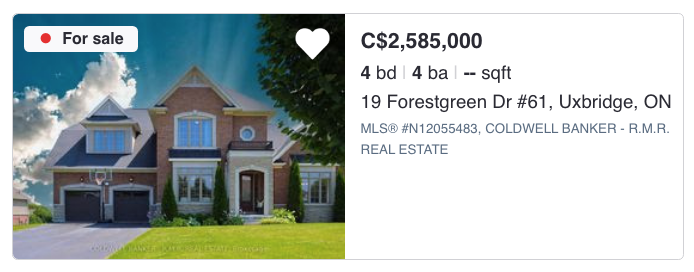

Welcome to 19 Forestgreen Drive, an exquisite estate nestled within the prestigious gated community of The Estates of Wyndance in Uxbridge, Ontario.

This luxurious Sheffield model home, perched atop the community's highest point, offers unparalleled privacy and breathtaking panoramic views.

Situated on the largest lot in the neighborhood, spanning 1.17 acres, this residence epitomizes elegance and sophistication.

Exceptional Design and Craftsmanship

Step inside to discover a harmonious blend of classic design and modern amenities.The main level boasts hardwood floors, wainscoting, and intricate tray and waffle ceilings, creating an ambiance of refined luxury.

The gourmet kitchen is a chef's dream, featuring top-of-the-line stainless steel appliances, granite countertops, and a spacious center island.

Adjacent to the kitchen, the breakfast area opens to an expansive covered deck, perfect for enjoying picturesque skyline views.

The living room, adorned with a captivating double-sided gas fireplace, offers a cozy retreat for relaxation.

Spacious and Versatile Living

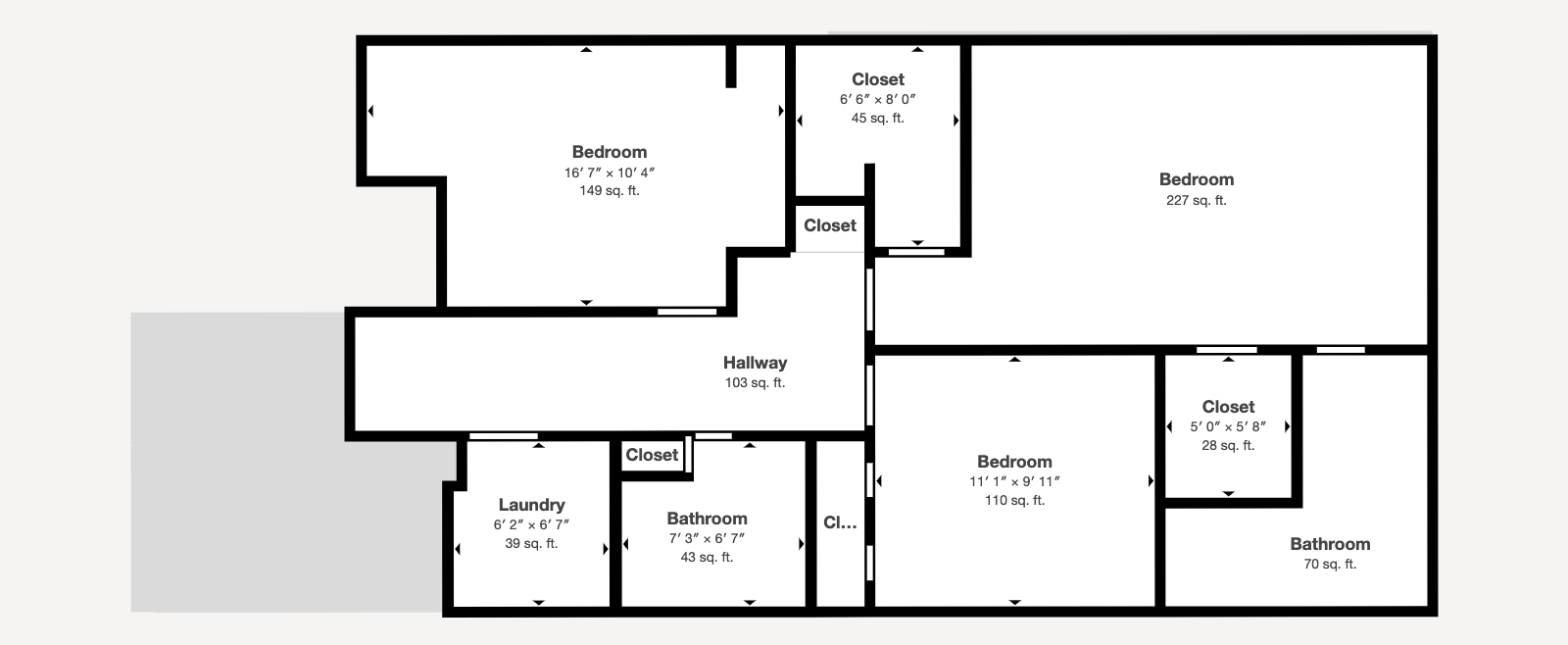

This 2-storey home encompasses 4 bedrooms and 4 bathrooms, providing ample space for family and guests.

The primary bedroom features a 5-piece ensuite and his-and-hers closets, while additional bedrooms offer generous proportions and access to well-appointed bathrooms.

The walk-out basement presents an opportunity to create an in-law suite, complete with space for up to two additional bedrooms, a full kitchen, living area, and a pre-existing rough-in for a 4-piece bathroom.

The three-car tandem garage ensures ample space for vehicles and storage needs.

Exclusive Community Amenities

Residents of The Estates of Wyndance enjoy a host of premium amenities, including:

Monthly fees of $553.91 cover water, sewer, snow clearing of roads, road maintenance, landscaping, community fencing, street and park lights, insurance, and access to the aforementioned facilities.

Prime Location

Located in Rural Uxbridge, this home offers the tranquility of country living with convenient access to nearby amenities.

The area boasts over 220 kilometers of seasonally managed trails, attracting cyclists, hikers, and nature enthusiasts.

Nearby schools include Uxbridge Secondary School and Stouffville District Secondary School, providing excellent educational opportunities for families.

Property Video

Community Video

Investment Potential

This property represents a significant investment in a rapidly appreciating area.

Uxbridge has seen a consistent population increase in recent years, as more potential buyers discover the tranquil way of life found in such a scenic place.

Don't miss the opportunity to own this exceptional property.Contact me today to schedule a private tour and experience the unparalleled luxury of 19 Forestgreen Drive.Your dream home awaits.

Bank of Canada Holds Steady Amid US Trade Turmoil: Decoding the Latest Monetary Policy Report

The Bank of Canada, in its announcement on April 16, 2025, elected to maintain its target for the overnight rate at 2.75%, alongside the Bank Rate at 3% and the deposit rate at 2.70%.

This decision arrives at a pivotal moment for the Canadian economy, as it grapples with the significant and unpredictable shifts in United States trade policy, which continue to cast a shadow of uncertainty over economic prospects.

The April Monetary Policy Report (MPR), released concurrently, underscores the substantial challenges in forecasting GDP growth and inflation for both Canada and the global economy amidst this evolving trade landscape.

The report outlines two distinct scenarios that explore potential future paths, contingent on the direction of US trade policy.

🛍️ Recommendation for Buyers:

With the Bank of Canada holding its key interest rate, mortgage rates may remain relatively stable in the short term, offering buyers a chance to breathe and plan strategically. This is an opportune moment to:

Get pre-approved while fixed-rate options remain appealing.

Take advantage of less volatility in borrowing costs, especially if you’ve been sitting on the sidelines waiting for clarity.

Act early if you’re eyeing a property—if inflation cools further, rates may begin to decline, sparking increased competition.

📌 Tip: Locking in a rate hold with your lendernow can shield you from potential upticks while giving you time to shop with confidence.

🏡 Recommendation for Sellers:

For sellers, a rate hold brings welcome stability to the market. Buyers are less hesitant, and there’s reduced fear of sudden rate hikes derailing deals. This creates an environment where:

Buyer confidence is likely to improve, especially in the entry-to-mid level segments.

You may benefit from a more predictable negotiation landscape with fewer financing surprises.

Listing sooner rather than later could help you get ahead of any surge in inventory should rates eventually drop.

📌 Tip: Work with a REALTOR® (yes, like me 😄) to position your home competitively and highlight value—especially with buyers now able to stretch their budgets a little further.

On April 16, 2025, the Bank of Canada decided to keep its benchmark interest rate unchanged at 2.75%. This move follows a series of seven consecutive reductions in the key rate, implemented to support economic activity as trade tensions began to escalate.

The Bank Rate was held at 3%, and the deposit rate remained at 2.70%. This decision to pause rate cuts was anticipated by a slight majority of economists, reflecting the delicate balance the central bank must strike between supporting growth and managing potential inflationary pressures stemming from trade disruptions.

The next scheduled announcement regarding the overnight rate target is set for June 4, 2025. The Bank's decision to refrain from further easing monetary policy at this time suggests a cautious stance, allowing policymakers to observe how the unfolding trade situation impacts the Canadian economy.

This approach acknowledges the limitations of monetary policy as a tool to directly address the uncertainties inherent in international trade disputes.

"The Bank of Canada today maintained its target for the overnight rate at 2.75%, with the Bank Rate at 3% and the deposit rate at 2.70%."

The significant reorientation of US trade policy and the unpredictable nature of tariffs have injected a high degree of uncertainty into the economic outlook, both domestically and internationally.

This unpredictability has diminished the prospects for robust economic growth and has simultaneously elevated expectations for inflation. The financial markets have reacted sharply to the stream of tariff-related announcements, including implementations, postponements, and ongoing threats of further escalation, contributing significantly to the prevailing atmosphere of uncertainty.

This environment of pervasive uncertainty poses considerable challenges for accurately forecasting the trajectory of GDP growth and inflation, not only for Canada but for the global economy as a whole.

The interconnectedness of the Canadian and US economies amplifies the impact of these policy shifts, creating a climate where businesses and consumers alike are hesitant to make long-term commitments, potentially leading to a deceleration in economic activity.

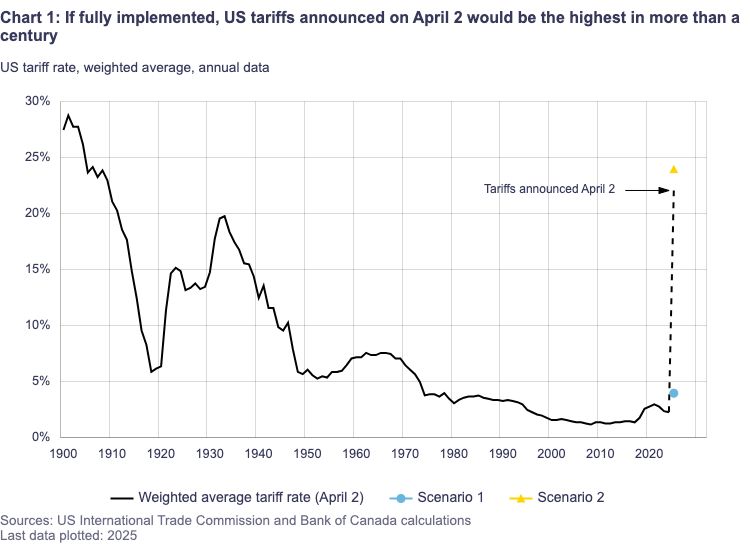

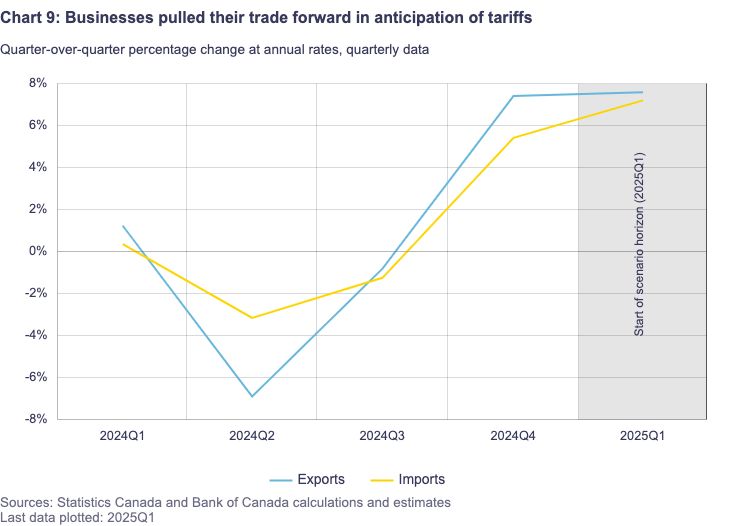

In light of the significant uncertainty surrounding US trade policy, the April MPR presents two illustrative scenarios to explore potential economic pathways.

Scenario 1: High Uncertainty, Limited Tariffs This scenario posits a situation where uncertainty remains elevated concerning US trade policy, but the actual implementation of tariffs is limited in scope. Under these conditions, the Canadian economy is projected to experience a temporary weakening in its growth trajectory.

However, despite this temporary slowdown, inflation is expected to remain anchored around the Bank of Canada's target of 2%. Even with a limited imposition of tariffs, the sustained high level of uncertainty can still act as a deterrent to economic activity, as businesses and households may adopt a more cautious approach to spending and investment.

The fact that inflation is projected to remain near the target suggests that any upward price pressures from the limited tariffs are likely to be counterbalanced by other factors, such as the anticipated weakening in economic growth or the removal of the consumer carbon tax.

Scenario 2: The Protracted Trade War The second scenario outlines a much more severe outcome, where a protracted trade war ensues, leading to a significant and sustained disruption to international trade.

In this case, the Bank of Canada anticipates that the Canadian economy would fall into recession within the current year. Furthermore, inflation is projected to rise temporarily above 3% in the following year. A prolonged trade war, characterized by widespread tariffs and potential retaliatory measures, would severely impact Canadian businesses and consumers.

The resulting economic contraction would likely lead to job losses and reduced household spending. The temporary surge in inflation would be driven by higher import costs due to tariffs and disruptions to global supply chains.

It is important to note that these two scenarios represent only a fraction of the possible outcomes, and the actual evolution of US trade policy could take many other forms.

The unprecedented nature and rapid pace of the shifts in US trade policy contribute to a significant degree of uncertainty surrounding the economic consequences, making it unusually challenging to predict the precise impacts.

Examining the global economic landscape, the Bank of Canada's report highlights varying conditions across major economies. In the United States, there are indications of a slowdown in economic activity, accompanied by increasing policy uncertainty and a decline in overall sentiment. Simultaneously, inflation expectations have been on the rise.

The Euro Area experienced modest economic growth in early 2025, with the manufacturing sector continuing to exhibit weakness. China's economy demonstrated strength at the close of 2024, but recent data suggests a moderate deceleration in its growth momentum.

Financial markets have experienced considerable turbulence due to the ongoing uncertainty surrounding trade policies. This extreme market volatility is contributing to the overall sense of economic unease.

Notably, global oil prices have fallen significantly since January, primarily reflecting diminished prospects for global economic growth in the face of these trade tensions. In contrast, the Canadian dollar has recently appreciated in value, largely driven by a broad weakening of the US dollar.

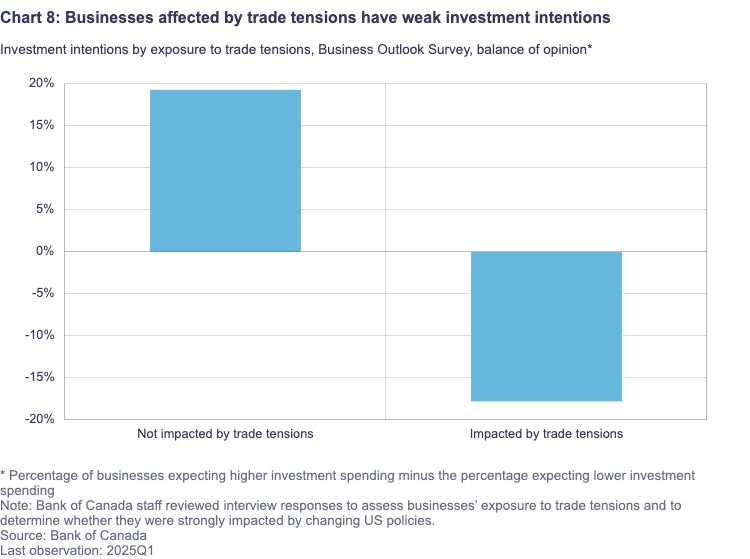

Within Canada, the economy is showing signs of a slowdown as the uncertainty surrounding tariff announcements weighs on both consumer and business confidence. Data from the first quarter of 2025 indicate a weakening in consumption, residential investment, and business spending.

The ongoing trade tensions are also disrupting the recovery of the labor market, with employment declining in March and businesses reporting intentions to curtail hiring. Furthermore, wage growth continues to exhibit signs of moderation.

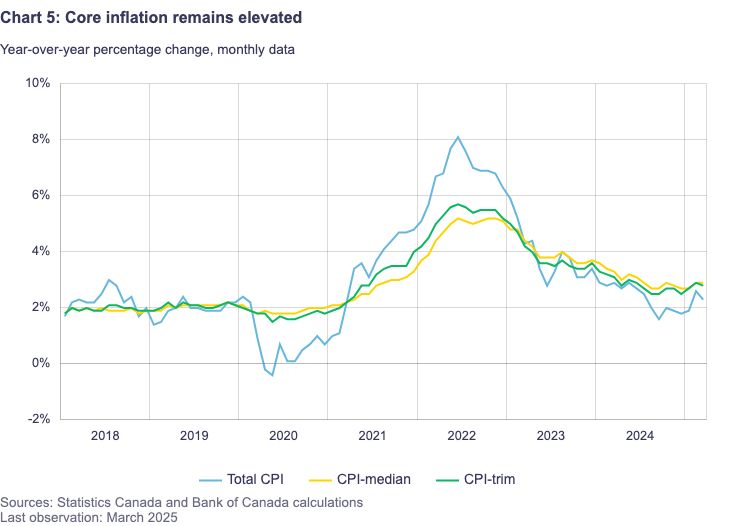

Canada's inflation rate stood at 2.3% in March, a decrease from February's 2.6% but still above the 1.8% recorded at the time of the January MPR. The recent uptick in inflation is partly attributed to a rebound in goods price inflation and the cessation of the temporary GST/HST suspension.

Looking ahead, the removal of the consumer carbon tax starting in April is expected to exert downward pressure on CPI inflation for a year. Additionally, lower global oil prices are anticipated to dampen inflation in the near term.

However, the potential for tariffs and supply chain disruptions to drive up certain prices remains a concern. Consequently, short-term inflation expectations have edged upward as businesses and consumers foresee higher costs arising from trade conflicts and supply chain issues, while longer-term inflation expectations remain relatively stable.

The Bank of Canada's Governing Council will continue its careful evaluation of the interplay between the downward pressures on inflation stemming from a potentially weaker economy and the upward pressures resulting from increased costs.

Their primary objective is to ensure that Canadians maintain confidence in price stability throughout this period of global economic turbulence. This necessitates a strategy that supports economic growth while diligently controlling inflation.

"Governing Council will proceed carefully, with particular attention to the risks and uncertainties facing the Canadian...source

In conclusion, the Bank of Canada has opted to maintain its key interest rate amid significant uncertainty stemming from US trade policy. The April MPR outlines two potential scenarios, one involving limited tariffs and the other a protracted trade war, each with distinct implications for Canadian economic growth and inflation.

While the global economic outlook presents a mixed picture, the Canadian economy is already showing signs of slowing in response to trade tensions. The factors influencing inflation are multifaceted, with the removal of the carbon tax and lower oil prices potentially offsetting some of the upward pressure from tariffs. The Bank of Canada remains committed to navigating this period of uncertainty with a focus on maintaining price stability for Canadians.

Scenario

Key Assumptions

Impact on Canadian GDP Growth (2025)

Impact on Canadian GDP Growth (2026)

Impact on Canadian Inflation (2025)

Impact on Canadian Inflation (2026)

Other Key Impacts

Scenario 1: High Uncertainty, Limited Tariffs

High uncertainty, most tariffs negotiated away by end of 2026

Weakens temporarily

Moderate expansion

Around 2%

Below 2%

Scenario 2: The Protracted Trade War

Long-lasting global trade war with additional US and global tariffs added

The Ontario real estate market, particularly in the Greater Toronto Area (GTA), has always been influenced by various economic factors such as interest rates, foreign investments, and government policies. However, one less commonly discussed factor is the role of tariffs. These import taxes, especially on construction materials, significantly impact housing costs, affordability, and investment strategies.

2. Understanding Tariffs

Tariffs are government-imposed taxes on imported goods. They are often used to protect domestic industries, retaliate against foreign trade policies, or generate government revenue. While tariffs can have broad economic implications, their effects on real estate are particularly profound when applied to materials such as steel, aluminum, and lumber—key components in construction.

3. History of Tariffs in Canada

Canada has a history of imposing and responding to tariffs, often in reaction to U.S. trade policies. Over the years, tariffs on construction materials have fluctuated based on trade agreements such as NAFTA and its successor, the USMCA. Understanding the historical context of these tariffs provides insight into their recurring impact on real estate markets.

4. Major Tariffs Affecting Real Estate

Steel and Aluminum Tariffs

Steel and aluminum are crucial in high-rise construction and infrastructure development. Tariffs on these materials increase costs for developers, affecting the pricing of new housing projects in the GTA.

Lumber Tariffs

Lumber tariffs have a direct effect on homebuilding costs. Since many GTA homes are built with wood framing, increased costs lead to higher home prices.

Other Construction Materials

Tariffs on items such as glass, appliances, and plumbing fixtures also contribute to rising construction expenses.

5. How Tariffs Increase Construction Costs

Higher tariffs mean increased costs for builders, who pass these expenses onto buyers. This phenomenon leads to:

Increased Home Prices: Higher costs of raw materials make homes more expensive.

Reduced Housing Supply: Developers may delay or cancel projects due to inflated costs.

Longer Construction Timelines: Increased expenses can lead to financial constraints, slowing down construction projects.

6. The Role of U.S.-Canada Trade Relations

Since much of Ontario’s building materials are imported from the U.S., changes in American trade policies significantly affect Canada’s real estate market. Political shifts and renegotiated agreements like the USMCA dictate tariff rates and their subsequent impact.

7. Foreign Investment and Tariffs

Foreign investors often look for cost-effective opportunities. Rising tariffs may deter international buyers from investing in the GTA market, affecting demand and price trends.

8. Tariffs’ Effect on New Developments

Real estate developers in Ontario, especially in the GTA, are directly impacted by tariffs. Increased costs often lead to:

Smaller Developments: Builders may opt for fewer units to mitigate expenses.

Higher Pre-construction Pricing: Buyers must pay more for homes even before they’re built.

Shifts in Material Sourcing: Developers may seek alternative suppliers to cut costs, potentially compromising quality.

9. Impact on Home Prices and Affordability

With rising construction costs due to tariffs, housing affordability in the GTA becomes a major issue. First-time buyers struggle to enter the market, and existing homeowners see fluctuating property values.

10. How Tariffs Influence Mortgage Rates

While tariffs don’t directly affect mortgage rates, they contribute to inflation. In response, the Bank of Canada may adjust interest rates, indirectly influencing mortgage affordability.

11. Impact on Homebuyers

Increased Costs

Higher home prices mean buyers need larger down payments and higher mortgage approvals.

Limited Choices

A reduced supply of new builds leaves fewer options for prospective homeowners.

Market Timing Concerns

Uncertainty surrounding tariffs makes it difficult for buyers to predict when to enter the market.

12. Impact on Sellers

Changing Buyer Demand

Higher prices may limit the pool of eligible buyers, leading to longer listing times.

Price Adjustments

Sellers may need to adjust their expectations based on market fluctuations caused by tariffs.

13. Government Policies and Responses

To counteract tariff effects, the Canadian government may introduce:

Subsidies for Builders

Tax Breaks for First-time Buyers

Negotiated Trade Agreements to Reduce Tariffs

14. Economic Forecasts and Market Predictions

Experts suggest that unless tariffs decrease, the GTA real estate market will continue experiencing high prices and limited affordability. However, government intervention and alternative supply strategies could mitigate these effects.

15. Strategies for Buyers and Sellers

For Buyers

Monitor Market Trends: Stay informed about tariff changes.

Consider Alternative Housing Options: Condos may be more affordable than single-family homes.

Secure Mortgage Pre-approval Early: Lock in lower rates before they rise.

For Sellers

Price Competitively: Adjust listing prices to attract buyers.

Highlight Home Features: Showcase value beyond pricing.

Be Open to Negotiation: Buyers may seek flexibility due to rising costs.

16. Case Studies and Real-Life Examples

Case Study 1: Condo Development in Downtown Toronto

A developer faced higher costs due to steel tariffs, resulting in a 15% price increase for pre-construction units.

Case Study 2: First-Time Buyer in Mississauga

A couple struggled with affordability as new home prices surged, leading them to opt for a resale property instead.

17. Conclusion and Final Thoughts

Tariffs have a profound impact on the Ontario real estate market, particularly in the GTA. Buyers and sellers must stay informed and adopt strategic approaches to navigate these economic challenges. While tariffs create obstacles, government policies and market adaptability can help mitigate long-term effects.

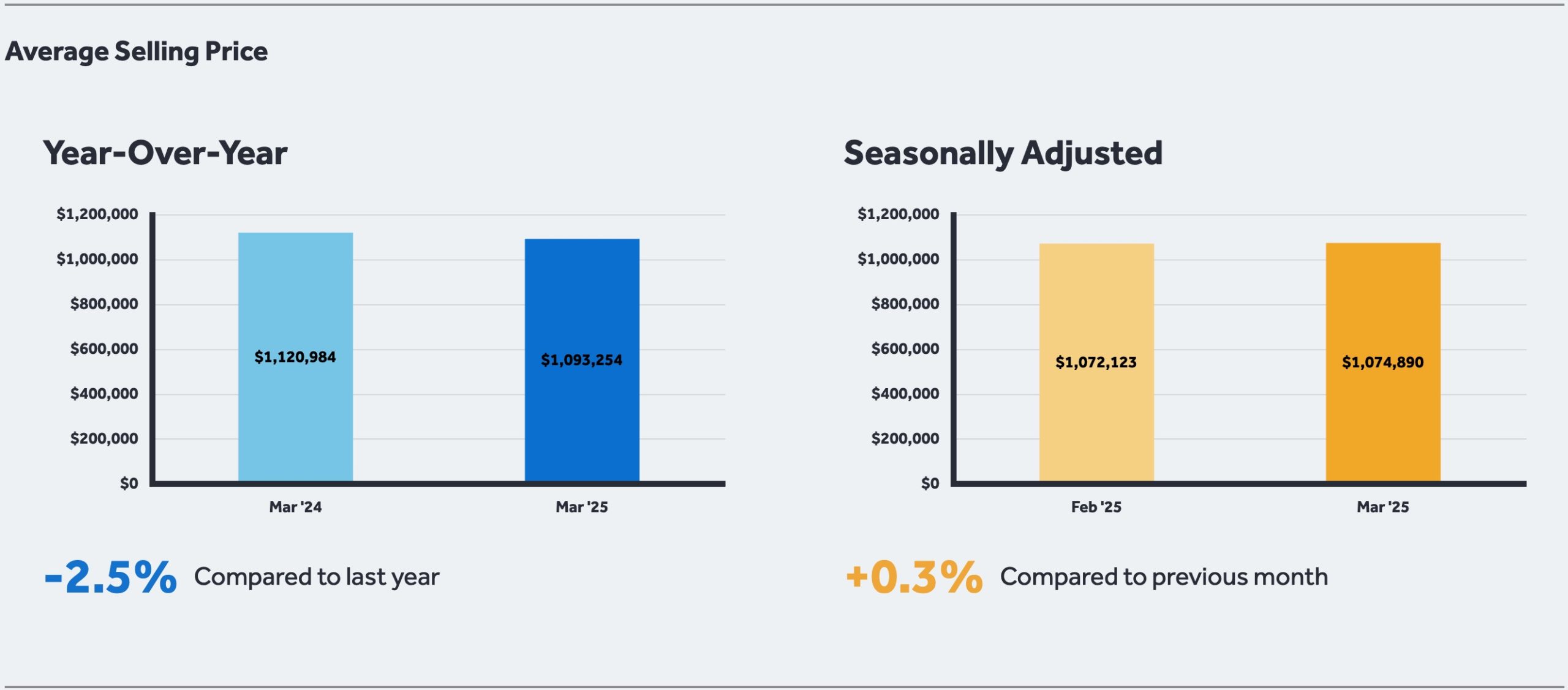

The Greater Toronto Area (GTA) real estate market in March 2025 has presented a landscape marked by improved affordability and a broader selection of properties for prospective homebuyers. This shift is attributed to declining borrowing costs, moderated home prices, and a surge in new listings.

However, underlying economic uncertainties, particularly related to international trade tensions and the impending federal election, have influenced buyer sentiment and market dynamics.

Key Market Indicators

In March 2025, GTA REALTORS® reported 5,011 home sales through the Toronto Regional Real Estate Board’s (TRREB) MLS® System, representing a 23.1% decrease compared to March 2024. Conversely, new listings rose by 28.6% year-over-year, totaling 17,263 properties.

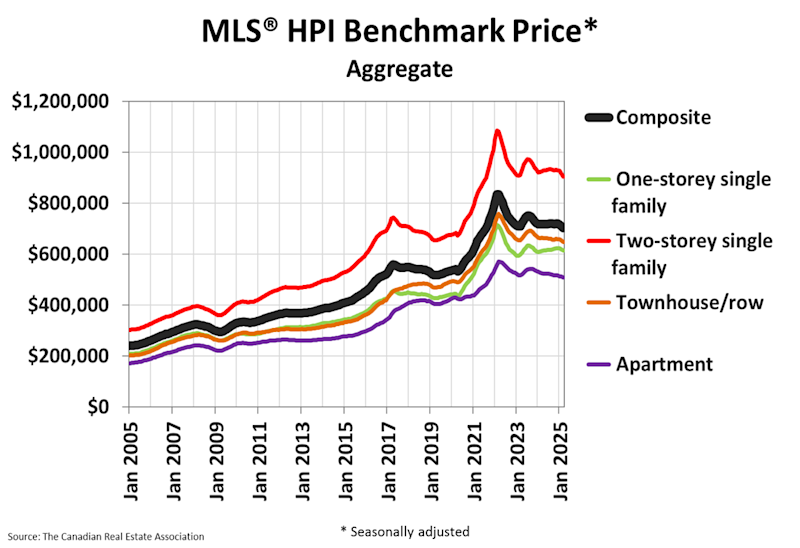

The MLS® Home Price Index Composite benchmark declined by 3.8% annually, while the average selling price decreased by 2.5% to $1,093,254.

The following table summarizes these key metrics:

Metric

March 2024

March 2025

Year-over-Year Change

Home Sales

6,519

5,011

-23.1%

New Listings

13,423

17,263

+28.6%

MLS® HPI Composite Benchmark Price .

N/A

N/A

-3.8%

Average Selling Price

$1,120,000

$1,093,254

-2.5%

Affordability and Borrowing Costs

The decline in both home prices and borrowing costs over the past year has enhanced affordability for potential homeowners. TRREB President Elechia Barry-Sproule noted, “Homeownership has become more affordable over the past 12 months, and we expect further rate cuts this spring.”

The Bank of Canada’s recent interest rate reductions have played a pivotal role in lowering borrowing costs, thereby making monthly mortgage payments more manageable for households. This trend is expected to continue, providing further relief to buyers.

Impact of Economic Uncertainty

Despite improved affordability, economic uncertainties have led many potential buyers to adopt a cautious approach. TRREB’s Chief Information Officer Jason Mercer stated, “Given the current trade uncertainty and the upcoming federal election, many households are likely taking a wait-and-see approach to home buying.”

The introduction of a 10% baseline tariff on all U.S. imports by President Donald Trump has heightened trade tensions, potentially impacting Canada’s economy and, consequently, consumer confidence in the housing market.

Market Dynamics: Supply and Demand

The substantial increase in new listings has expanded the inventory available to buyers, granting them greater negotiating power. This influx of supply, coupled with tempered demand due to economic uncertainties, has contributed to the observed decline in home prices. The following chart illustrates the trend in new listings and home sales over the past year:

Chart: Total New Listings and Sale-to-New Listings Ratio for March 2024 / March 2025

Housing Policy and Future Outlook

Housing remains a focal point in the political arena, with federal parties emphasizing its importance in their platforms. TRREB CEO John DiMichele highlighted, “Building this housing will be a key economic driver moving forward.”

The upcoming federal election and potential policy changes are expected to influence market conditions. Buyers and sellers alike are advised to stay informed about policy developments that may impact housing affordability and availability.

Conclusion

The GTA real estate market in March 2025 reflects a complex interplay of improved affordability, increased housing choices, and economic uncertainties. Prospective buyers benefit from lower prices and borrowing costs, alongside a wider selection of properties.

However, factors such as trade tensions and political developments continue to shape market dynamics. Stakeholders are encouraged to monitor these trends closely and consult with real estate professionals to navigate this evolving landscape effectively.

– Overview of Canada’s housing crisis

– Government’s response to the crisis

Understanding the GST Elimination

– Definition of GST

– Details of the GST elimination policy

Advantages for First-Time Homebuyers

– Financial savings

– Increased affordability

– Encouragement of homeownership

Impact on Builders

– Reduction in construction costs

– Incentives for new projects

– Potential challenges

Effects on the Real Estate Market

– Increase in housing supply

– Stabilization of housing prices

– Market dynamics

Potential Challenges and Considerations

– Regional disparities

– Long-term sustainability

– Monitoring and evaluation

Frequently Asked Questions (FAQs)

– Six common questions and answers

Conclusion

– Summary of key points

– Future outlook

Published: March 20, 2025

Introduction

Canada is currently facing a significant housing crisis characterized by soaring demand, limited supply, and escalating prices. In response, the federal government has introduced a pivotal measure aimed at alleviating these challenges: the elimination of the Goods and Services Tax (GST) for first-time homebuyers on homes priced at or below $1 million. This article delves into the intricacies of this policy, exploring its advantages for first-time homebuyers, implications for builders, and its broader impact on the real estate market.

Understanding the GST Elimination

Definition of GST

The Goods and Services Tax (GST) is a federal tax applied to most goods and services sold in Canada. Typically set at 5%, this tax contributes to the overall cost of purchasing a home, thereby affecting affordability.

Details of the GST Elimination Policy

On March 20, 2025, Prime Minister Mark Carney announced the removal of the GST for first-time homebuyers purchasing homes valued at or under $1 million. This initiative is designed to reduce upfront costs, potentially saving buyers up to $50,000, thus making homeownership more attainable for many Canadians.

The most immediate benefit of this policy is the substantial financial savings. By eliminating the 5% GST on eligible homes, first-time buyers can save a significant amount, which can be redirected towards other expenses such as home improvements, furnishings, or reducing mortgage principal.

Removing the GST lowers the overall purchase price of homes, thereby enhancing affordability. This reduction in cost can enable more young people and families to enter the housing market, fulfilling their aspirations of homeownership.

Encouragement of Homeownership

This tax relief serves as an incentive for individuals who were previously hesitant due to high costs, encouraging a new wave of homeowners and promoting economic stability through increased property ownership.

Impact on Builders

√ Reduction in Construction Costs

For builders, the elimination of GST on homes under $1 million can lead to reduced construction costs. This reduction can improve profit margins or allow for more competitive pricing, thereby stimulating the construction industry.

√ Incentives for New Projects

Lower costs and increased demand from first-time buyers can motivate builders to initiate new projects, contributing to an increase in housing supply across the country.

√ Potential Challenges

While the policy presents opportunities, builders may face challenges such as ensuring quality amidst rapid construction and navigating regional market variations that could affect project viability.

Effects on the Real Estate Market

Increase in Housing Supply

The anticipated surge in construction projects is expected to boost the housing supply, addressing the current shortage and aligning supply more closely with demand.

Stabilization of Housing Prices

An increased supply of homes can lead to a stabilization of housing prices, making the market more accessible and reducing the pressure on buyers.

Market Dynamics

The policy may lead to shifts in market dynamics, including changes in investment patterns and a potential reevaluation of property values in various regions.

Potential Challenges and Considerations

Regional Disparities

The impact of the GST elimination may vary across regions, with urban areas potentially experiencing different effects compared to rural communities.

Long-Term Sustainability

While the policy addresses immediate affordability issues, considerations regarding its long-term sustainability and effectiveness in solving the housing crisis are crucial.

Monitoring and Evaluation

Continuous monitoring and evaluation are essential to assess the policy’s impact and make necessary adjustments to ensure it meets its objectives.

Frequently Asked Questions (FAQs)

Who qualifies as a first-time homebuyer under this policy?

A first-time homebuyer is typically defined as an individual who has not owned a home in the past four years. Specific eligibility criteria may vary, so it’s advisable to consult official guidelines.

Does the GST elimination apply to both new and resale homes?

The policy primarily targets new home purchases; however, details regarding its application to resale homes should be confirmed with official sources.

Are there any regional restrictions on the GST elimination?

The GST elimination is a federal policy applicable nationwide, but regional housing markets may experience varying impacts.

How does this policy affect mortgage qualification?

While the GST elimination reduces the purchase price, mortgage qualification still depends on factors such as income, credit score, and debt levels.

Will this policy lead to a decrease in housing prices?

The policy aims to stabilize housing prices by increasing supply, but actual price movements will depend on various market factors.

Is the GST elimination a temporary measure?

As of the announcement, the policy is intended as a permanent measure, but future governments may reassess its continuation.

Conclusion