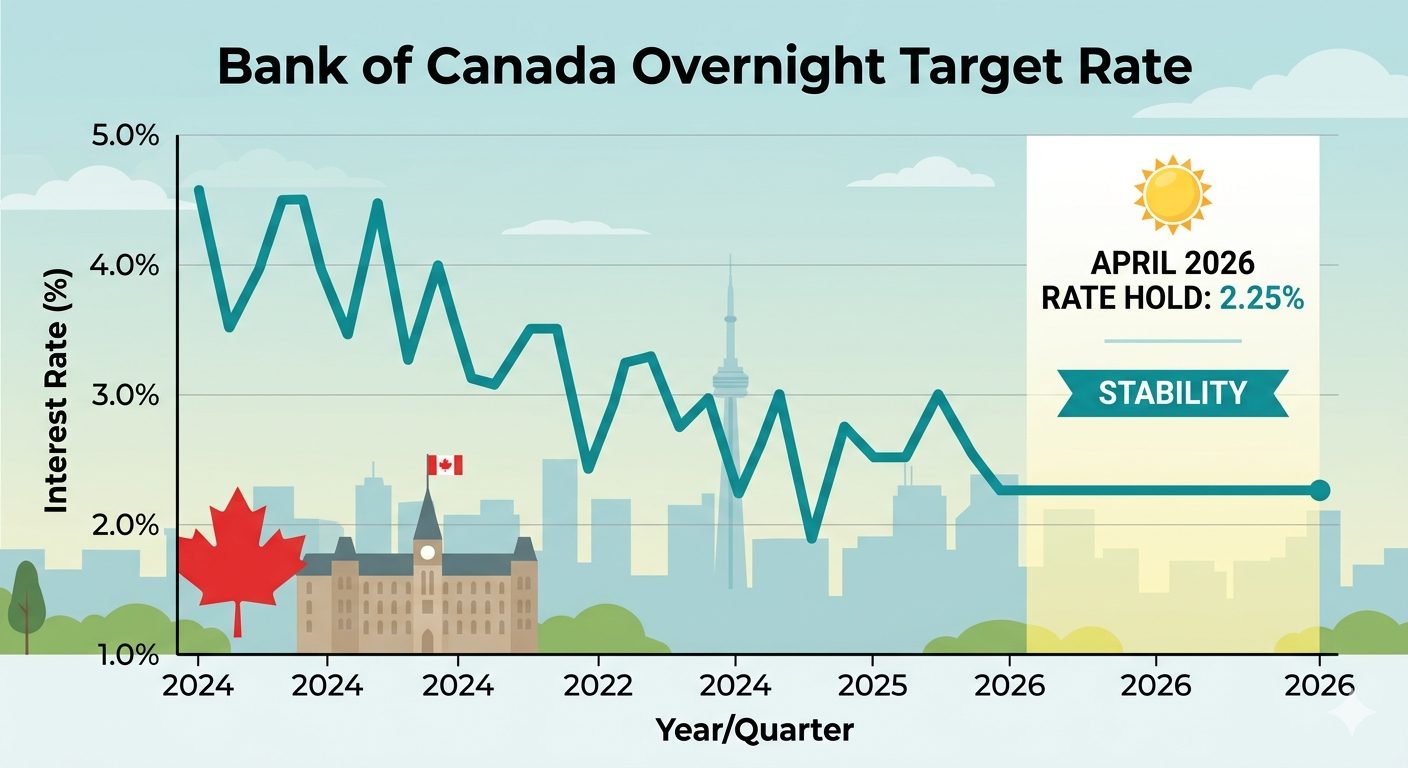

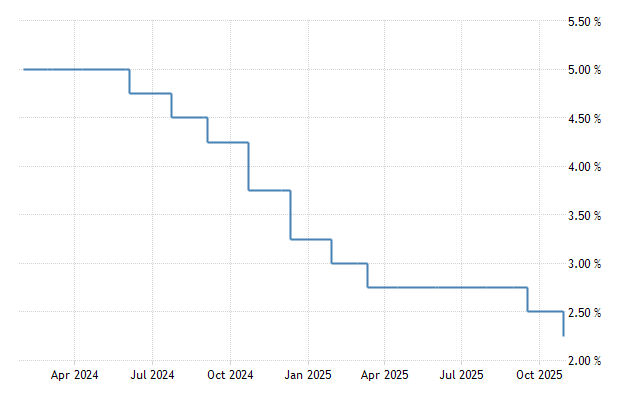

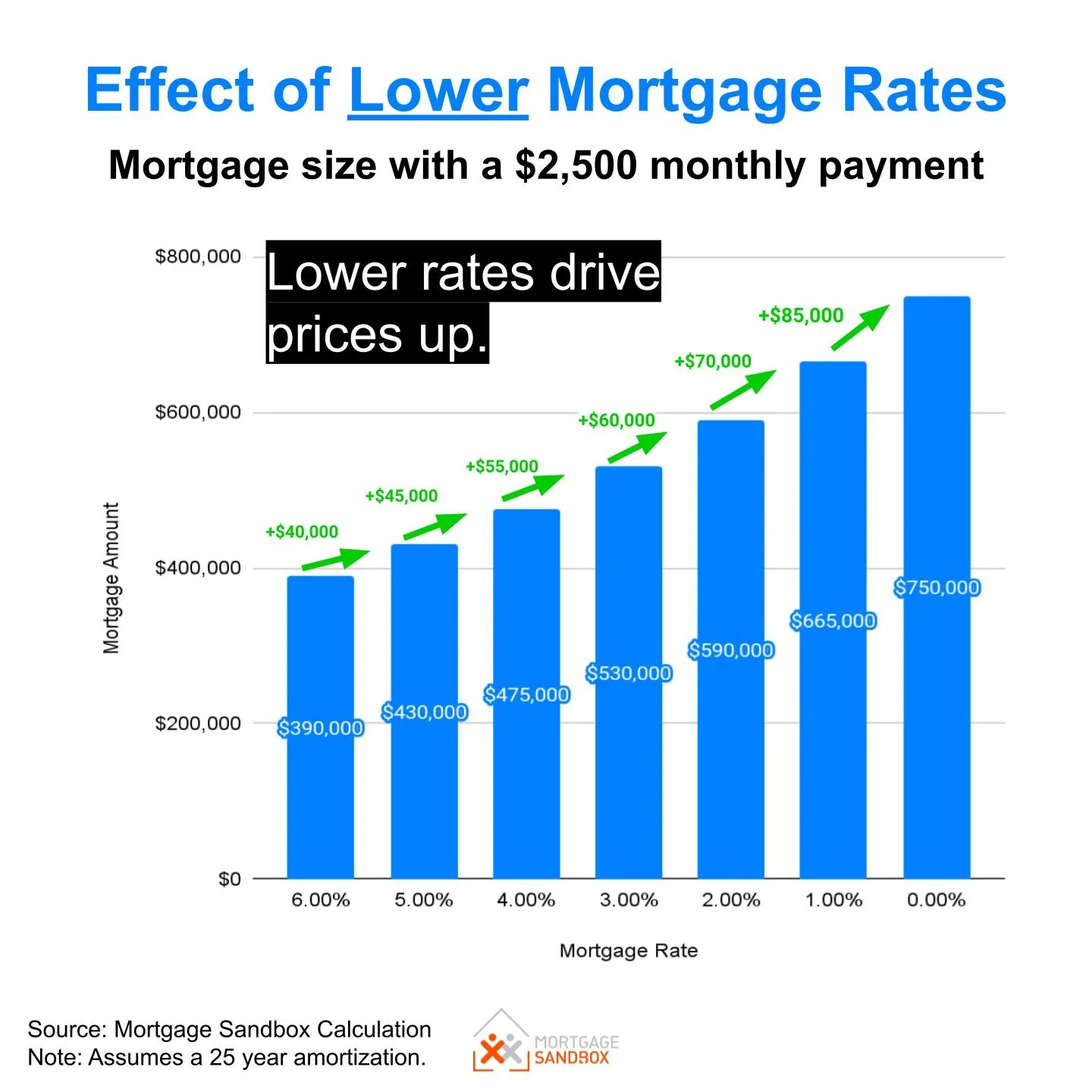

The Bank of Canada (BoC) has officially held its target for the overnight rate at 2.25% today, April 29, 2026. For homeowners, aspiring buyers, and savvy investors, this decision is the “calm within the storm.” While the rate remains steady, the global landscape—shifting from Middle East tensions to new US trade policies—is creating a complex environment for the Canadian housing market.

As your dedicated real estate partner, I’ve broken down exactly how these macroeconomic shifts will hit your pocketbook and your property value.

1. The “Rate Hold” Breakdown: Stability in Uncertain Times

The Governing Council’s decision to maintain the policy rate at 2.25% (with the Bank Rate at 2.5% and the deposit rate at 2.20%) signals a “wait and see” approach.The Bank is currently balancing a soft domestic labour market against a global surge in energy prices.

For the real estate market, this means mortgage stress tests and variable rates will remain relatively unchanged for the next quarter. However, the Bank noted that CPI inflation rose to 2.4% in March and is expected to hit 3% in April due to gasoline prices.

Expert Insight for Sellers: Stability is a selling feature. With rates holding steady, buyers have more confidence in their monthly payment projections. If you’ve been waiting for a “predictable” window to list, this is it.

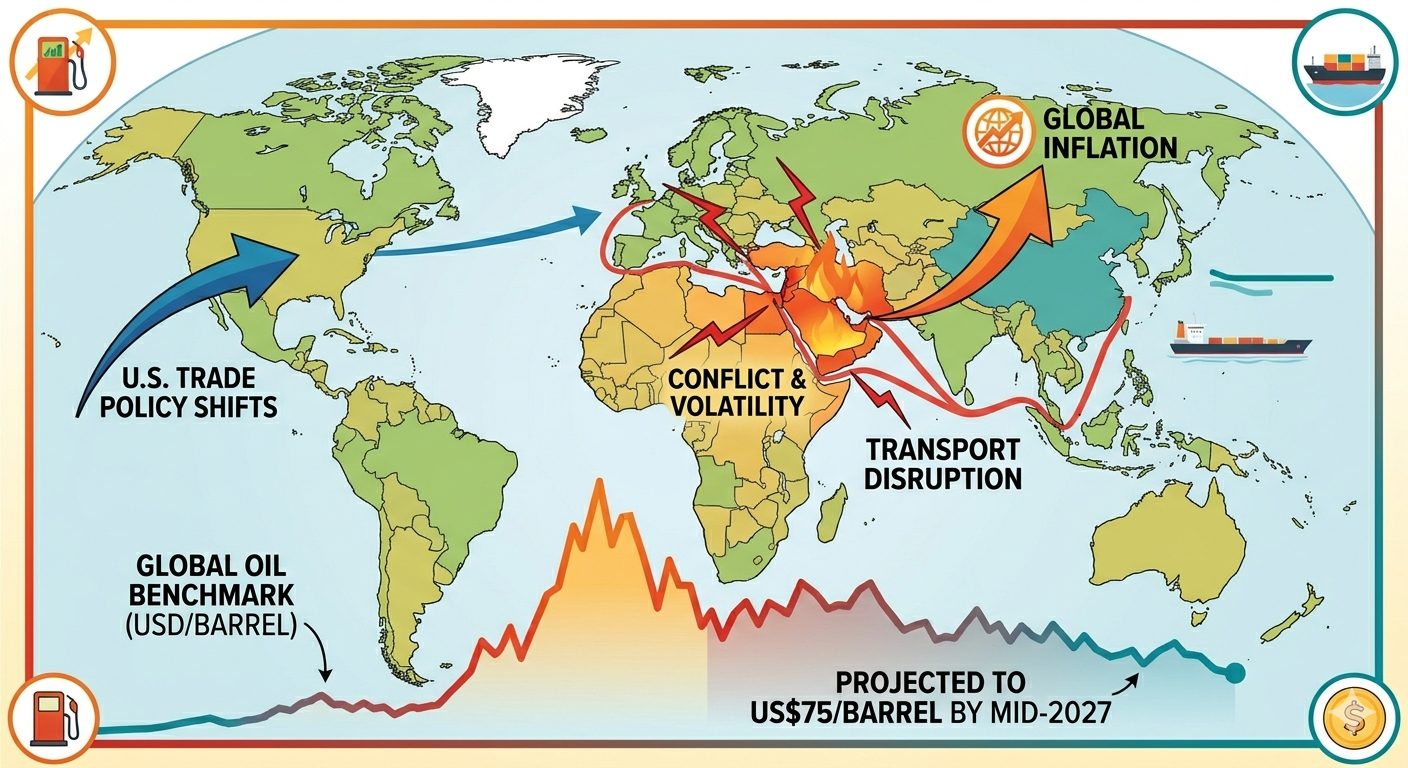

2. Global Volatility: The Iran War and Energy Costs

The ongoing conflict in the Middle East has sent shockwaves through the global economy.With oil prices projected to stay volatile before potentially declining to US$75 per barrel by mid-2027, Canadians are feeling the “gas pump squeeze.”

While higher oil prices actually boost Canada’s national income (as a net exporter), they simultaneously drain the disposable income of average households. This “dual impact” means that while the economy looks okay on paper, the average homebuyer has less cash left over for a mortgage after paying for heat and transport.

Expert Insight for Buyers: Don’t let the headlines scare you into inaction. While energy costs are up, the Bank of Canada expects inflation to return to the 2% target early next year. Locking in a home now before the next growth cycle could be your best long-term move.

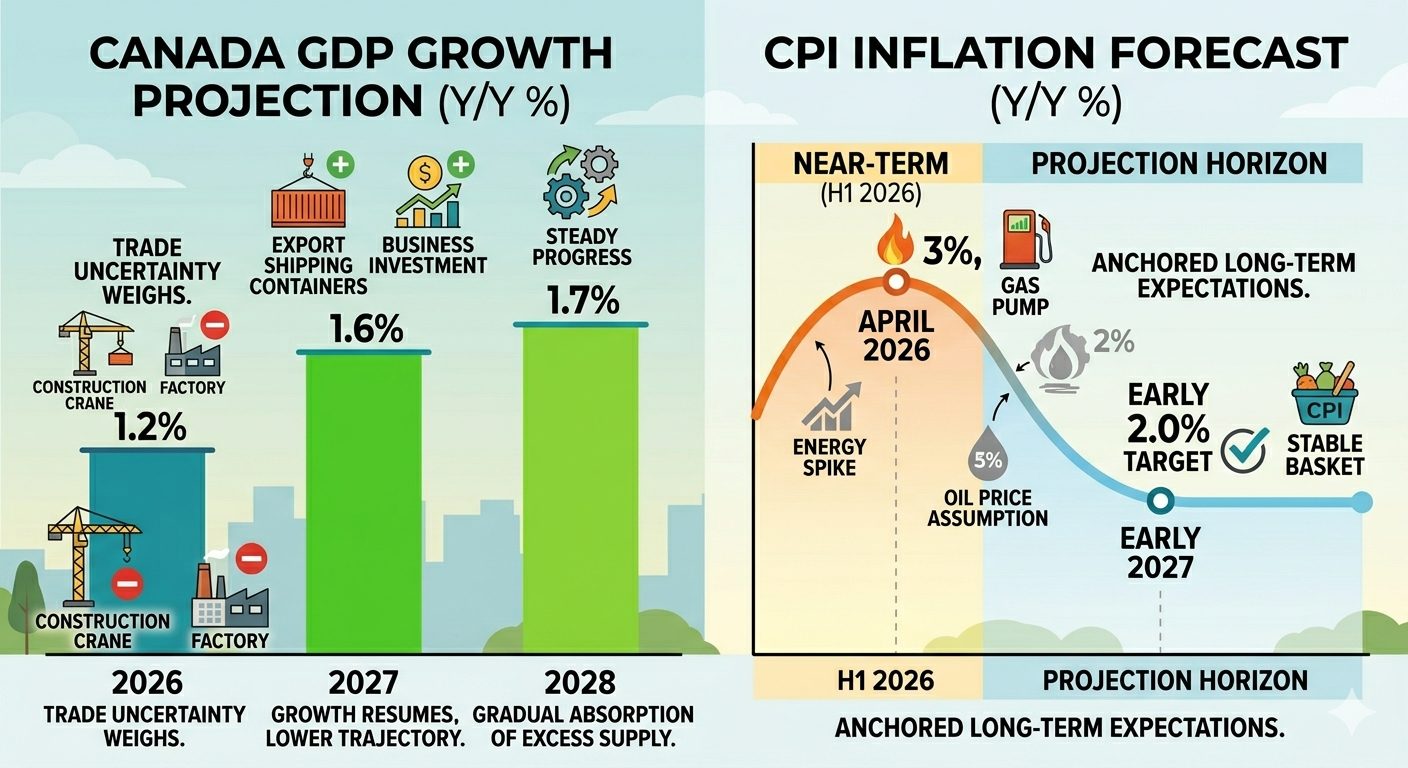

3. The US Trade Factor and the “Soft” Labour Market

The Bank highlighted that US trade policy and tariffs are weighing heavily on Canadian exports and business investment. We are seeing this reflected in a “soft” labour market, with the unemployment rate hovering between 6.5% and 7%.

Economic Indicator

2026 Projection

2027 Projection

GDP Growth

1.2%

1.6%

Inflation (CPI)

~3.0% (Near-term)

2.0% (Early 2027)

Unemployment

6.5% – 7.0%

Stabilizing

The job losses in sectors targeted by US tariffs have led to a cautious sentiment in the housing market. However, with AI-related investments boosting US growth and Canadian businesses adapting to new trade patterns, the BoC expects a gradual recovery.

Expert Insight for Sellers: Pricing strategy is everything in a soft labour market. To attract the most qualified buyers, your home needs to stand out through professional staging and aggressive digital marketing.

The Bank’s report was candid: Housing activity declined in late 2025 and is currently being held back by three factors:

Slow population growth.

General economic uncertainty.

Persistent affordability issues.

However, the “excess supply” in the general economy is being absorbed. As GDP growth rises toward 1.7% by 2028, the demand for housing is expected to outpace supply once again.

Expert Insight for Buyers: “Excess supply” is a phrase buyers love to hear. It means you have more leverage in negotiations than you’ve had in years. This is a rare “Buyer’s Market” window that may close as inflation anchors back to 2%.

The Bank of Canada is “looking through” the immediate spikes in energy prices, meaning they won’t hike rates just because gas is expensive—unless that inflation becomes “persistent.” Their forecast shows inflation returning to the 2% target early next year.

This suggests that 2026 is a “bridge year.” We are transitioning from the volatility of the mid-2020s into a more stable, growth-oriented period for 2027 and 2028.

Final Verdict: Should You Move Now?

For Sellers: You are competing in a market with fewer buyers, but those who are active are serious and benefit from stable rates.

For Buyers: You are in a unique position where “economic uncertainty” is providing you with more options and less competition.

The Bank of Canada is committed to price stability. I am committed to your financial success. Whether you are navigating a job change due to trade shifts or looking to downsize as energy costs rise, I have the data and the strategy to guide you home.

Ready to make your move in the 2026 market? Let’s chat.

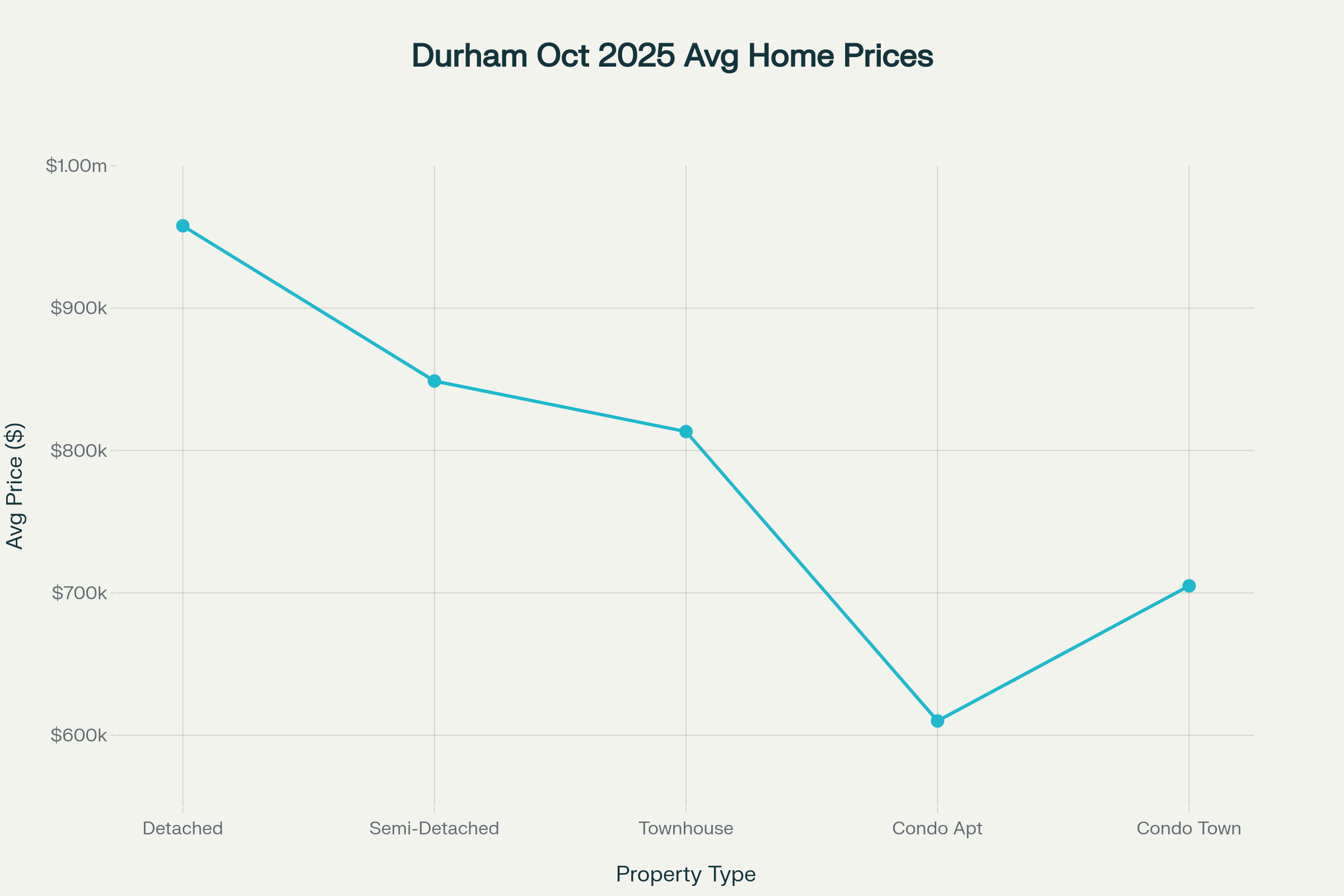

The Durham Region real estate market continues to evolve in early 2026, presenting very different opportunities depending on whether you’re buying or selling. With inventory increasing, prices adjusting, and buyer behaviour shifting, understanding the data behind the headlines is critical before making your next move.

In this March 2026 Durham Region Real Estate Market Report, we break down the latest statistics, explain what they really mean, and offer straight‑talk guidance for both buyers and sellers navigating today’s market.

If you’re wondering whether this is the right time to buy, sell, or simply plan your next move, this report will give you the clarity you need.

Market Snapshot – March 2026 at a Glance

Here are the most important numbers from March 2026:

Average Sale Price: $1,031,921

Median Sale Price: $942,500

Total Transactions: 21 sales

New Listings: 63 homes

Average Days on Market: 28 days

Homes Selling Below Asking: 85.7%

Year‑to‑Date Price Change: Down approximately 5% vs. last year

These numbers clearly show a market that has shifted away from the intense seller dominance of previous years and into a more balanced—and in many cases buyer‑favoured—environment.

Get Real Numbers for Your Neighbourhood

📍 Want to know what these trends mean for your specific home or target neighbourhood?

👉 Visit www.GeraldLawrence.ca and request a free, no‑obligation market breakdown customized to your exact location.

Pricing Trends: A Market in Correction, Not Collapse

While the headlines may focus on falling prices, it’s important to understand the context behind the data.

Key Pricing Changes

Average price is down 8.1% year‑over‑year

Median price declined 3.3% year‑over‑year

Month‑over‑month average price dropped 21.1%, largely due to fewer high‑end transactions

This does not indicate a crash. Instead, it reflects:

Higher interest rates limiting purchasing power

Buyers becoming more cautious and selective

Sellers adjusting expectations after aggressive pricing in previous years

What This Means:

✔ Prices are stabilizing closer to true market value

✔ Overpriced homes are sitting longer

✔ Well‑priced homes still sell—often quickly

What the March 2026 Market Means for Buyers

Buyers Are Gaining Leverage

March 2026 data clearly shows a shift in buyer power:

85.7% of homes sold below list price

Only 9.5% sold above asking, compared to 34.5% last year

Days on market are significantly shorter month‑over‑month but still longer year‑over‑year

This means buyers now have: ✅ Negotiating room

✅ Inspection and financing condition confidence

✅ More options with increased listings

Smart Buyer Strategies Right Now

Target homes that have been on the market over 20 days

Look for sellers who have already reduced their price

Negotiate closing costs, repairs, or flexible possession dates

Buy Smarter, Not Harder

🏡 Thinking about buying in Durham Region this year?

👉 Let Gerald Lawrence help you identify undervalued opportunities before they hit the mainstream market.

📩 Contact Gerald today through www.GeraldLawrence.ca

What the March 2026 Market Means for Sellers

Sellers Must Be Strategic

While homes are still selling, the days of “list it and they’ll come” are over.

Key seller signals:

63 new listings in March (up 46.5% month‑over‑month)

Average days on market dropped to 28, but still higher than last year

Only 1 in 10 homes selling above asking

Successful Sellers Are:

✔ Pricing accurately from day one

✔ Preparing homes professionally (staging, repairs, presentation)

✔ Marketing aggressively across digital platforms

Overpricing is the #1 reason listings fail in this market.

What Is Your Home Really Worth in 2026?

📈 Online estimates are outdated and misleading in today’s market.

👉 Request a custom home value assessment from Gerald Lawrence at www.GeraldLawrence.ca

Sales Volume & Buyer Confidence

Transaction volume rose 61.5% month‑over‑month, showing renewed buyer activity as confidence begins to return.

However:

Sales are still 27.6% lower than March last year

Year‑to‑date sales are down nearly 30%

This tells us buyers are active—but cautious. Decisions today are driven by value, not fear of missing out.

List‑to‑Sale Price Ratio: The New Reality

Average Sale‑to‑List Price: 96.3%

Median Sale‑to‑List Price: 97.0%

This market rewards: ✅ Competitive pricing

✅ Strong negotiation skills

✅ Professional representation

This is no longer a guessing game. Precision matters.

Durham Region Outlook for Spring & Summer 2026

Looking ahead:

Inventory is expected to remain elevated

Interest rate stability will drive modest buyer confidence

Well‑priced homes in desirable areas will continue to sell

Investors and move‑up buyers are watching closely

The market is normalizing—not weakening.

Plan Your Next Move With Confidence

📅 Whether you’re buying, selling, or planning ahead for 2026–2027:

👉 Book a confidential strategy session with Gerald Lawrence today at www.GeraldLawrence.ca

Final Thoughts: Strategy Beats Timing the Market

The March 2026 Durham Region real estate market rewards those who:

Understand the data

Adapt to changing conditions

Work with experienced local professionals

There is opportunity on both sides of the transaction—but only with the right strategy.

Ready to Take the Next Step?

🚀 Buying or selling in Durham Region?

👉 Visit www.GeraldLawrence.ca today for expert advice, personalized insights, and results‑driven real estate guidance.

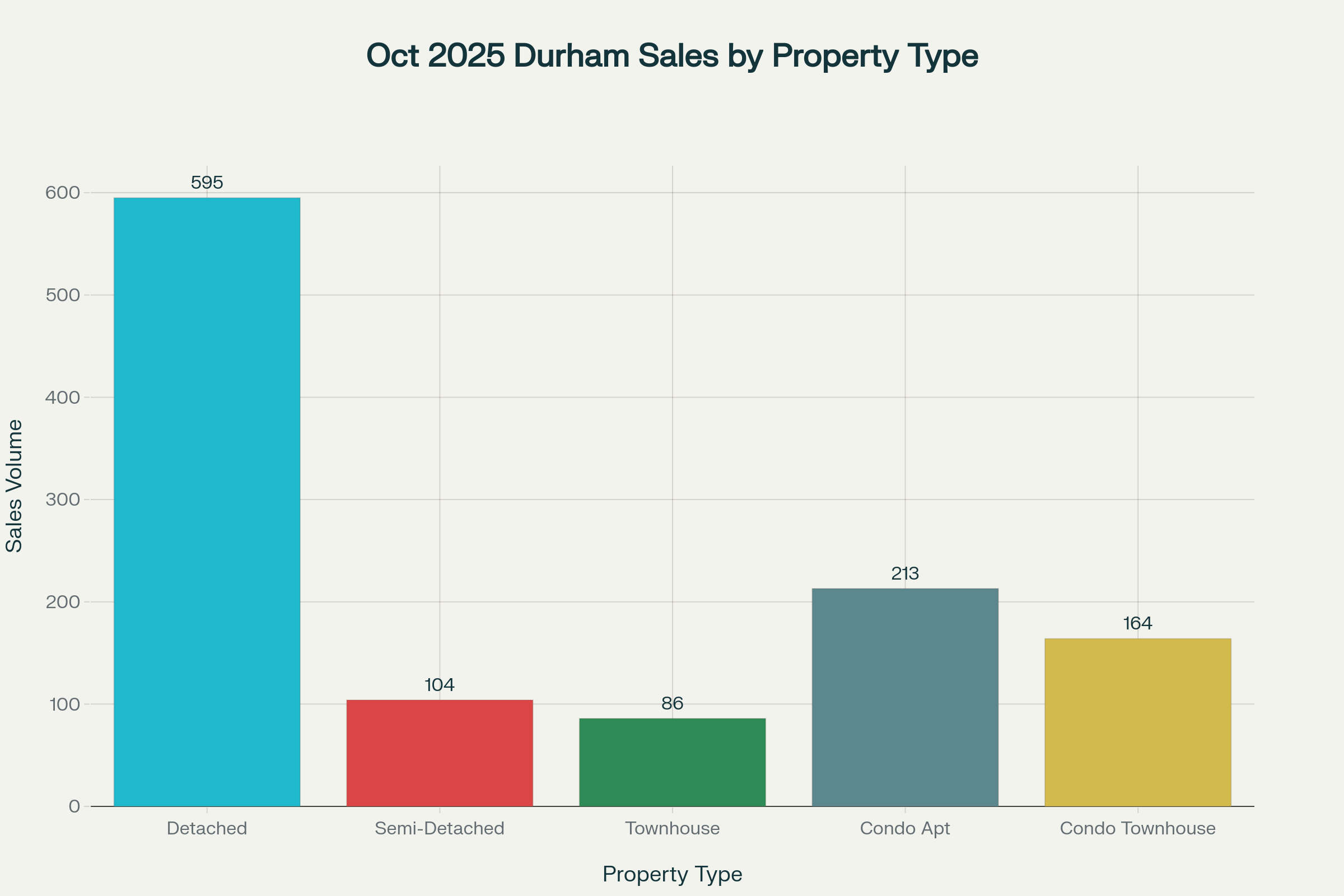

The spring market has officially arrived. In the real estate world, March is often the “bellwether” month—the period that sets the tone for the remainder of the year. The March 2026 data reveals a market defined by increased velocity, high inventory turnover, and a notable shift in buyer-seller leverage.

If you are navigating the current landscape, these numbers aren’t just statistics; they are the roadmap to your next big financial decision.

1. Price Analysis: The “Correction” Continues

While we saw a modest uptick in prices from February to March, the Year-over-Year (YoY) and Year-to-Date (YTD) figures show a cooling trend that is actually providing much-needed stability to the market.

Breaking Down the Numbers

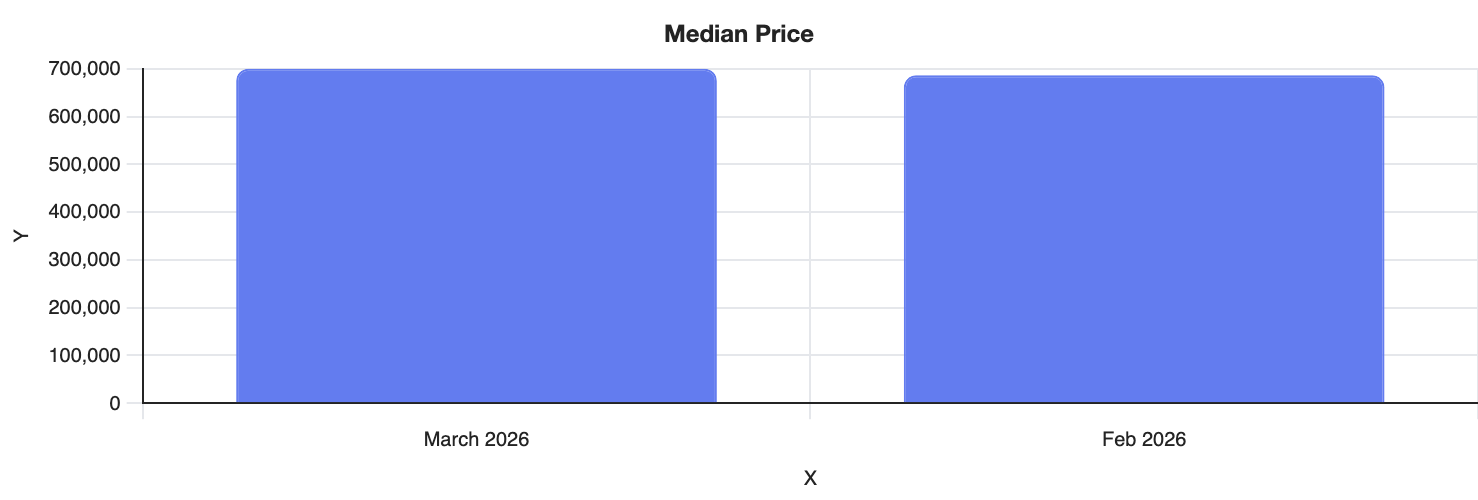

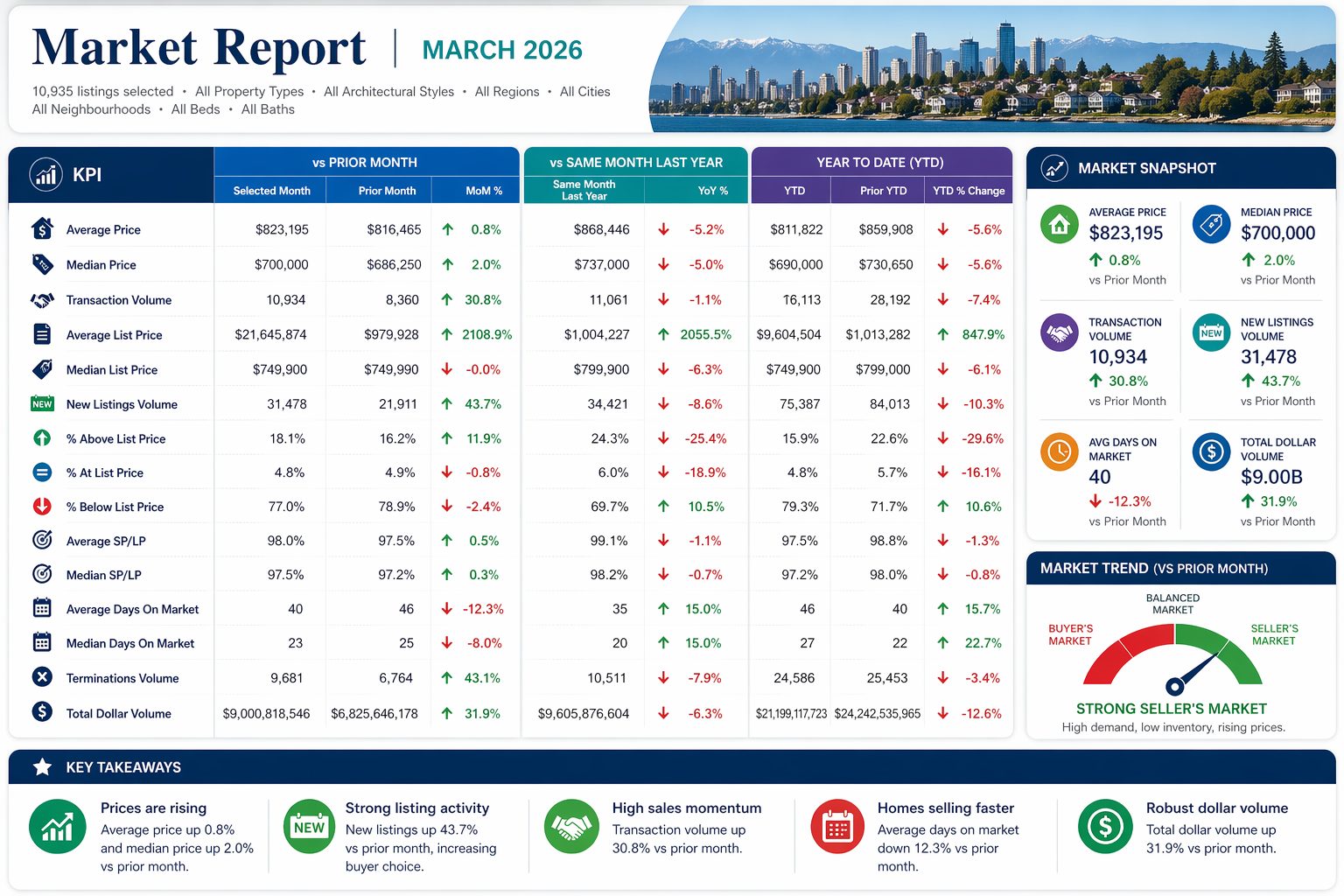

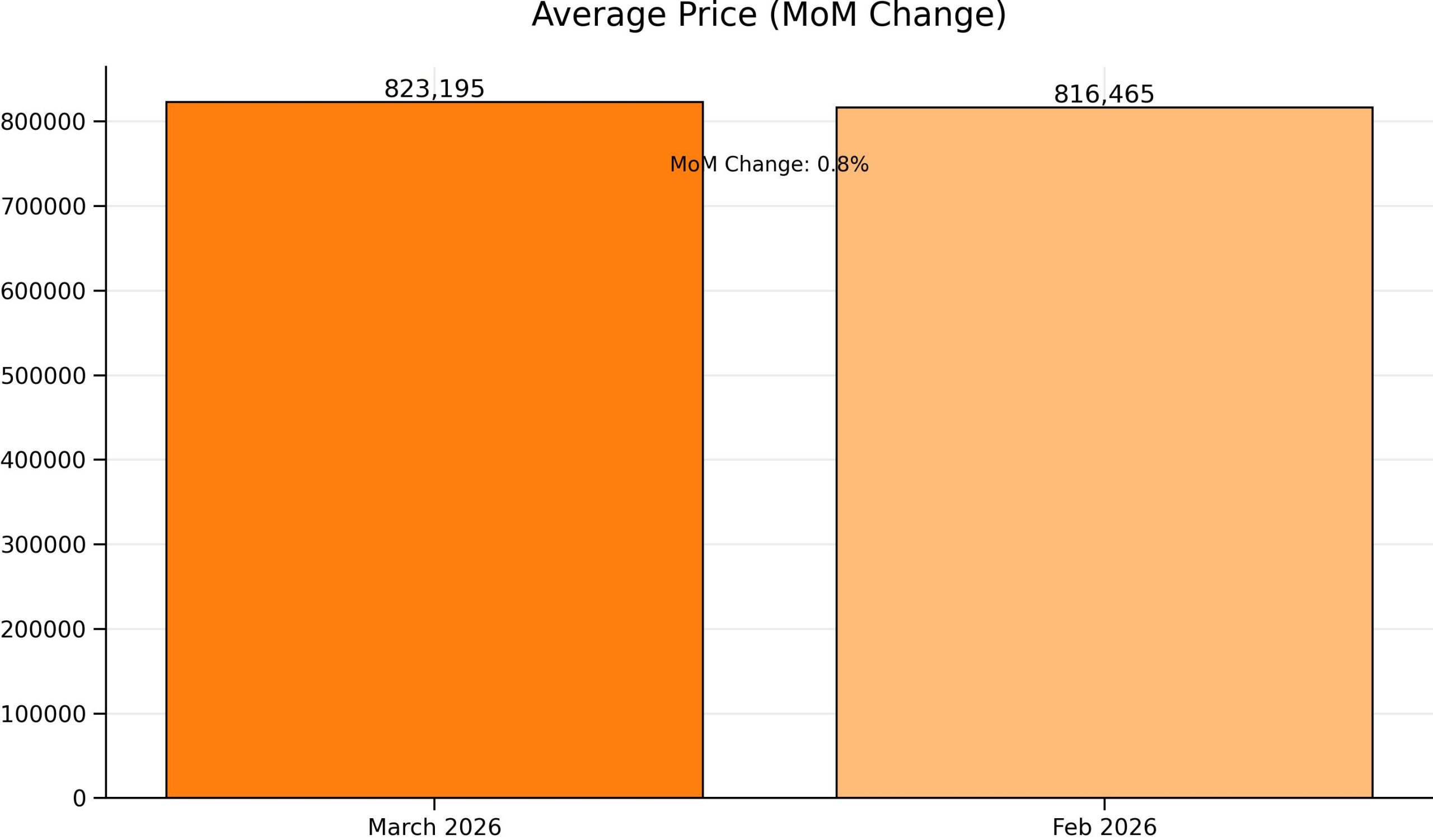

Average Sale Price: At $823,195, we are seeing a steady 0.8% increase over last month. However, we are down 5.2% from the $868,446 average seen in March 2025.

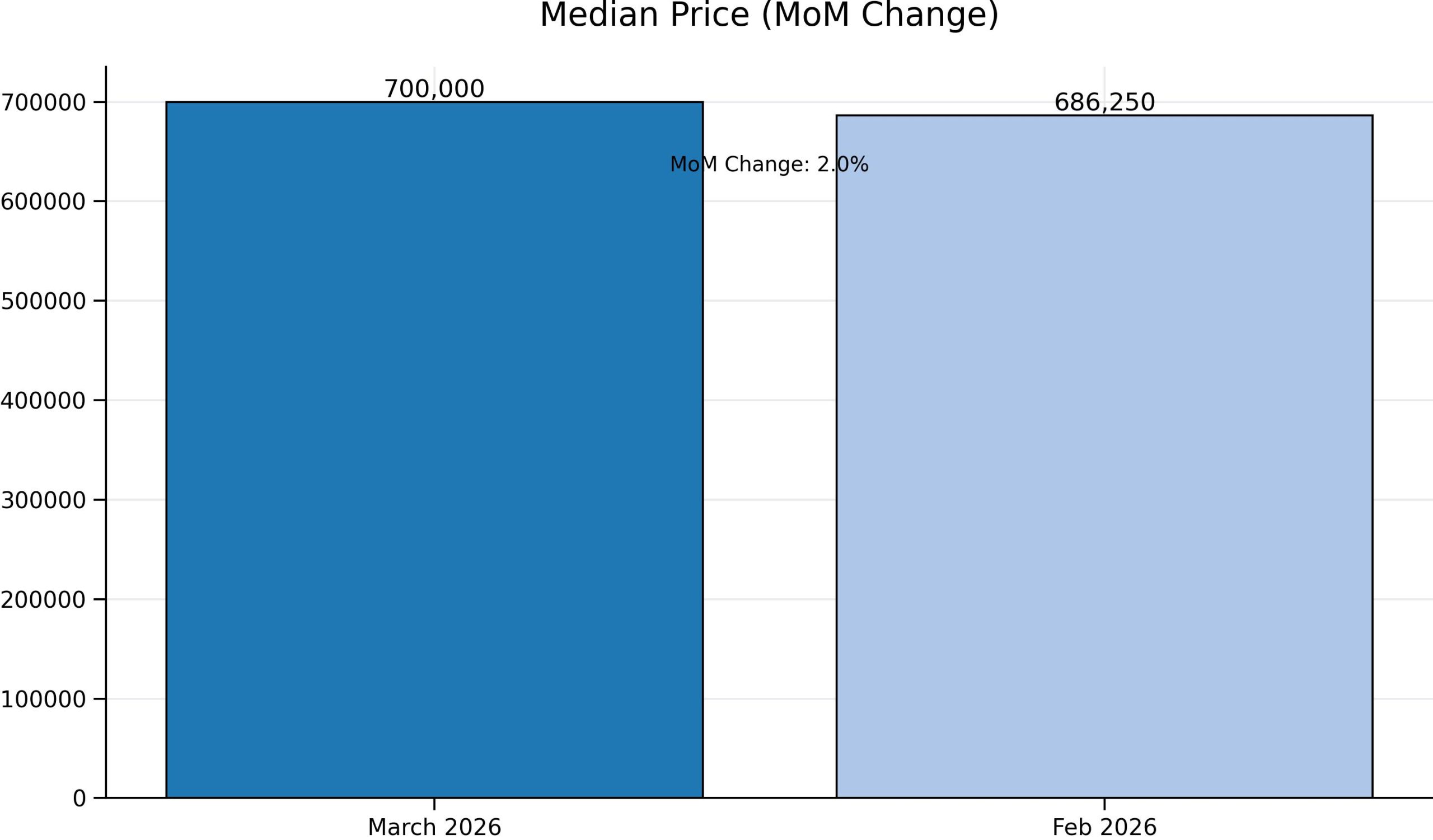

Median Sale Price: This is often a more accurate “middle-of-the-road” indicator. The median price rose 2.0% month-over-month to $700,000.

The List Price Anomaly: You may notice the Average List Price skyrocketed to over $21 million. This is a statistical anomaly caused by ultra-luxury inventory hitting the market, which skews the “average” but not the “median.”

The Takeaway for Sellers: Pricing is a delicate art right now. Over-shooting the market leads to terminations, while pricing at the “sweet spot” ensures you remain part of the successful transaction volume.

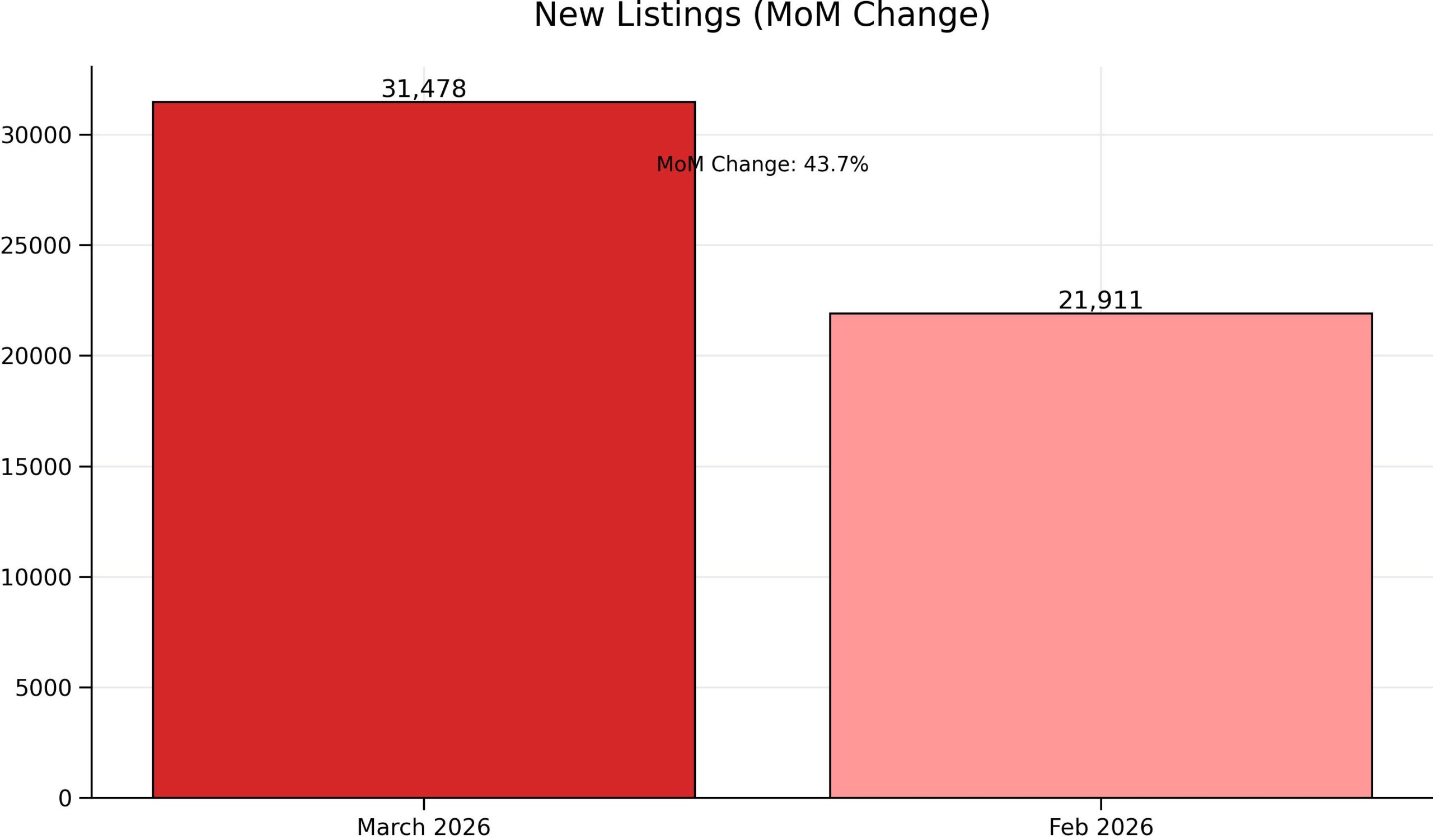

The most striking data point this month is the massive influx of activity. Both buyers and sellers emerged from winter hibernation with a vengeance.

The Volume Velocity

Metric

March 2026

MoM Change

What it Means

New Listings

31,478

+43.7%

A huge selection of homes for buyers.

Transaction Volume

10,934

+30.8%

Buyers are active and absorbing inventory.

Terminations

9,681

+43.1%

Sellers are quickly pivoting if their initial strategy fails.

The high termination volume suggests that the market is unforgiving of overpricing. Sellers who don’t see immediate traction are choosing to pull their listings and rethink their strategy rather than sitting stagnant on the market.

3. The “List-to-Sale” Reality Check

One of the most vital metrics for managing expectations is the Sales Price to List Price (SP/LP) ratio. In March 2026, the median SP/LP sat at 97.5%.

Where do the Sales Fall?

Below List Price (77.0%): The vast majority of transactions involved a negotiation. Buyers are successfully finding value below the asking price.

Above List Price (18.1%): Multiple offer scenarios still exist, but they are becoming the exception rather than the rule, down significantly from 24.3% last year.

At List Price (4.8%): A small fraction of homes sell exactly for the “sticker price.”

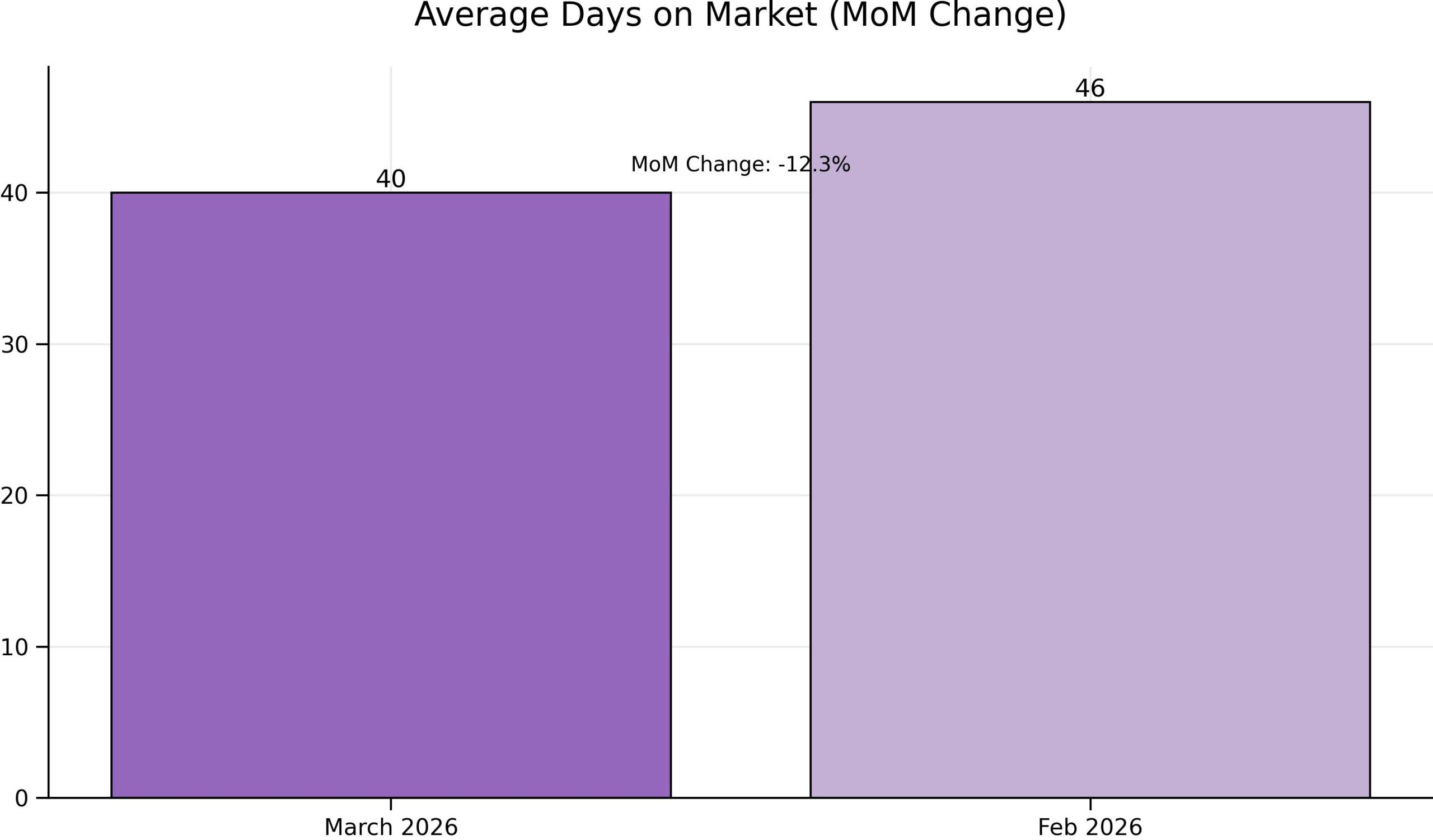

4. Time is of the Essence: Days on Market (DOM)

How long will it take to sell? The “Days on Market” metric is shrinking as we move deeper into the spring, but it remains higher than the frenetic pace of 2025.

Average DOM: 40 Days (A 12.3% decrease from last month).

Median DOM: 23 Days.

The “23-Day Rule”: In this market, the first three weeks are your “Golden Window.” If your property hasn’t seen a serious offer within 23 days, the data suggests it may be time to look at your pricing or presentation.

Don’t leave your timeline to chance. I specialize in aggressive marketing strategies that cut through the noise. Start your journey at www.GeraldLawrence.Realtor.

5. Strategic Guide for Buyers and Sellers

For the 2026 Home Seller

The market is active, but buyers are disciplined. To win, you must:

Stage for Success: With 31,000+ new listings to compete with, your home must be “magazine ready.”

Monitor the “Total Dollar Volume”: Total volume is down 12.6% YTD, meaning there is less total capital moving through the system. You need an agent who knows how to capture the serious buyers who are ready to act.

Use the Data: Don’t guess. Use the 97.5% median sale-to-list ratio to price your home strategically from day one.

For the 2026 Home Buyer

This is the most “buyer-friendly” spring we have seen in years.

Leverage the Terms: Since 77% of homes sell below list, you have the power to negotiate not just price, but conditions (inspections, financing, etc.).

Move on the Median: Since the median DOM is 23 days, you have time to do your due diligence, but you shouldn’t dawdle on high-quality listings.

Watch the YTD Trends: Prices are down 5.6% YTD compared to last year. Your purchasing power is effectively higher than it was twelve months ago.

6. Closing Summary: The Big Picture

The March 2026 report paints a picture of a vibrant, high-volume market that has finally moved away from the “panic buying” of years past. We are entering an era of Rational Real Estate, where data-driven decisions and professional representation are the difference between a “Sold” sign and a “Terminated” listing.

Ready to make your move in Ontario?

The market waits for no one, and neither should you. Whether you’re looking to capitalize on the 43.7% increase in new listings or you want to position your home for a top-dollar sale, I have the experience and the data to get you there.

If you’ve been priced out of the GTA, Northumberland County — including Cobourg, Port Hope, Grafton, Baltimore, and Canton—continues to offer one of the last remaining opportunities to purchase real estate under $500,000 within commuting distance to Toronto.

As a REALTOR®, I can confidently say: this price point is competitive—but still very achievable with the right strategy.

photo credit: Centris.ca

Don’t miss out on the best deals under $500K in Northumberland County. 👉 Visit http://www.GeraldLawrence.Realtoror call/text 416-556-0238 to get instant access to new listings before they hit the market. Follow for updates: @YorkDurhamHomes

Market Snapshot (Why $500K Still Exists Here)

Here’s what the data tells us about affordability in the area:

Median home price in Cobourg is around $500K, meaning entry-level opportunities still exist

In Port Hope, the median price is closer to ~$735K, but smaller homes and condos fall well below that

Balanced market conditions (5+ months inventory) mean buyers have negotiation leverage

Price Positioning in Northumberland

$300K ┤ Condos / Studios

$400K ┤ Small homes / Fixer-uppers $500K ┤ Entry-level detached / Townhomes ← TARGET RANGE

$700K ┤ Typical detached homes

$900K ┤ Premium / Waterfront

Thinking of selling? Find out what your home could sell for in today’s market. 👉 Get your free home evaluation athttp://www.GeraldLawrence.Realtoror call 416-556-0238 today. Stay connected: @YorkDurhamHomes

photo credit: farmontario.ca

At this price point, buyers are typically looking at:

1. Condos & Apartment Units

1–2 bedroom units in Cobourg near the waterfront

Low-maintenance living (ideal for first-time buyers or downsizers)

Great entry into the market with more space than condos

Strong rental/investment potential

3. Small Detached Homes

Often in Baltimore, Grafton, or Canton

May require cosmetic updates

Larger lots and quieter lifestyle

4. Fixer-Uppers & Investment Properties

Opportunity to build equity quickly

Ideal for investors or handy buyers

Looking for undervalued properties or fixer-uppers with strong upside? 👉 Browse opportunities at http://www.GeraldLawrence.Realtor or call 416-556-0238 to discuss your investment strategy. More insights: @YorkDurhamHomes

Your home deserves more than just a listing—it needs a strategy.👉 Let’s talk marketing, pricing, and results at http://www.GeraldLawrence.Realtoror 416-556-0238. See how I market homes: @YorkDurhamHomes

photo credit: narcity.ca

Why You Should Act NOW

Inventory has increased, giving buyers more choice and leverage

Prices have stabilized after previous peaks, creating entry opportunities

Infrastructure and development (like regional growth) continue to push long-term values upward

This is a strategic buying window—not a waiting market.

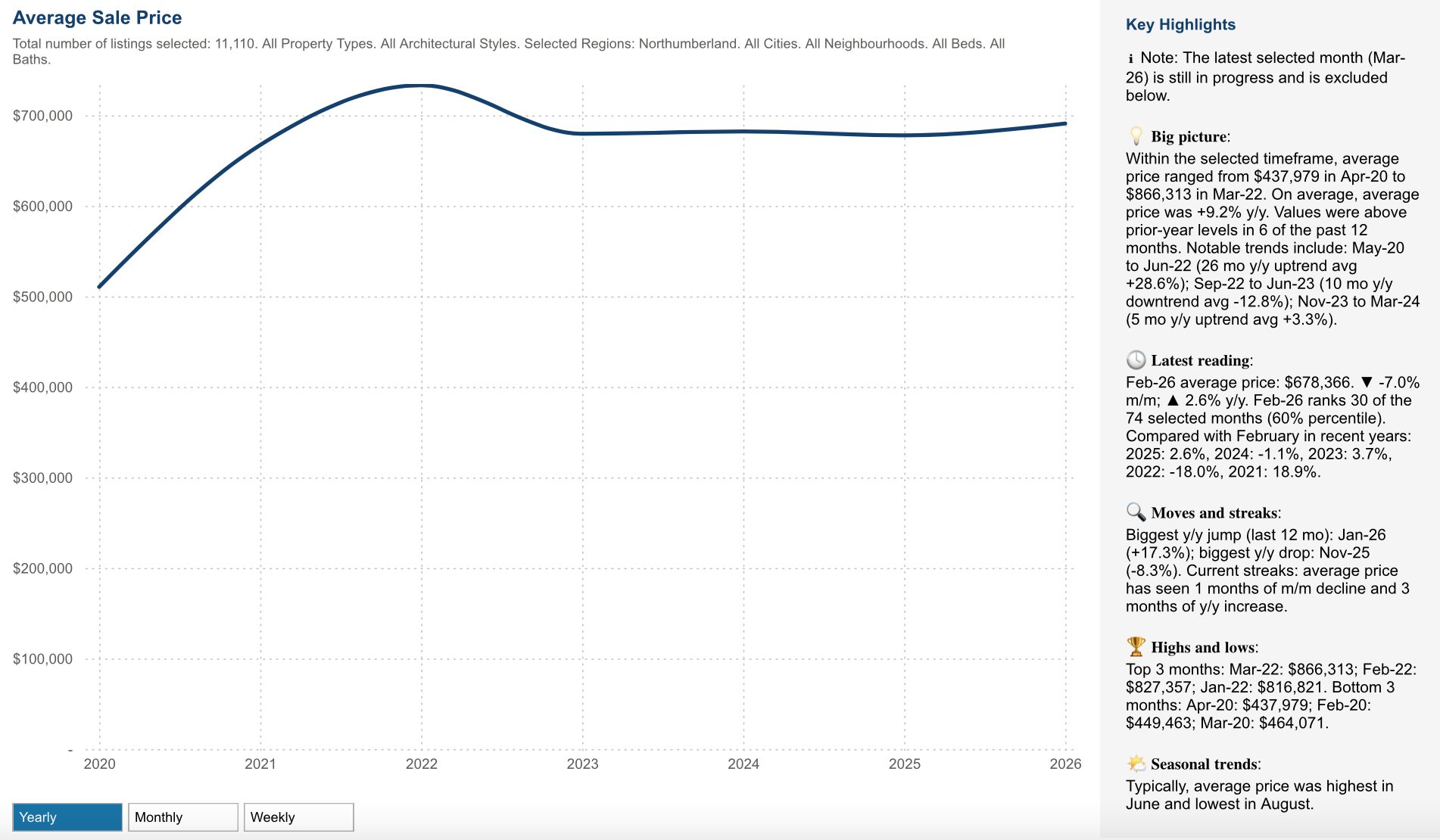

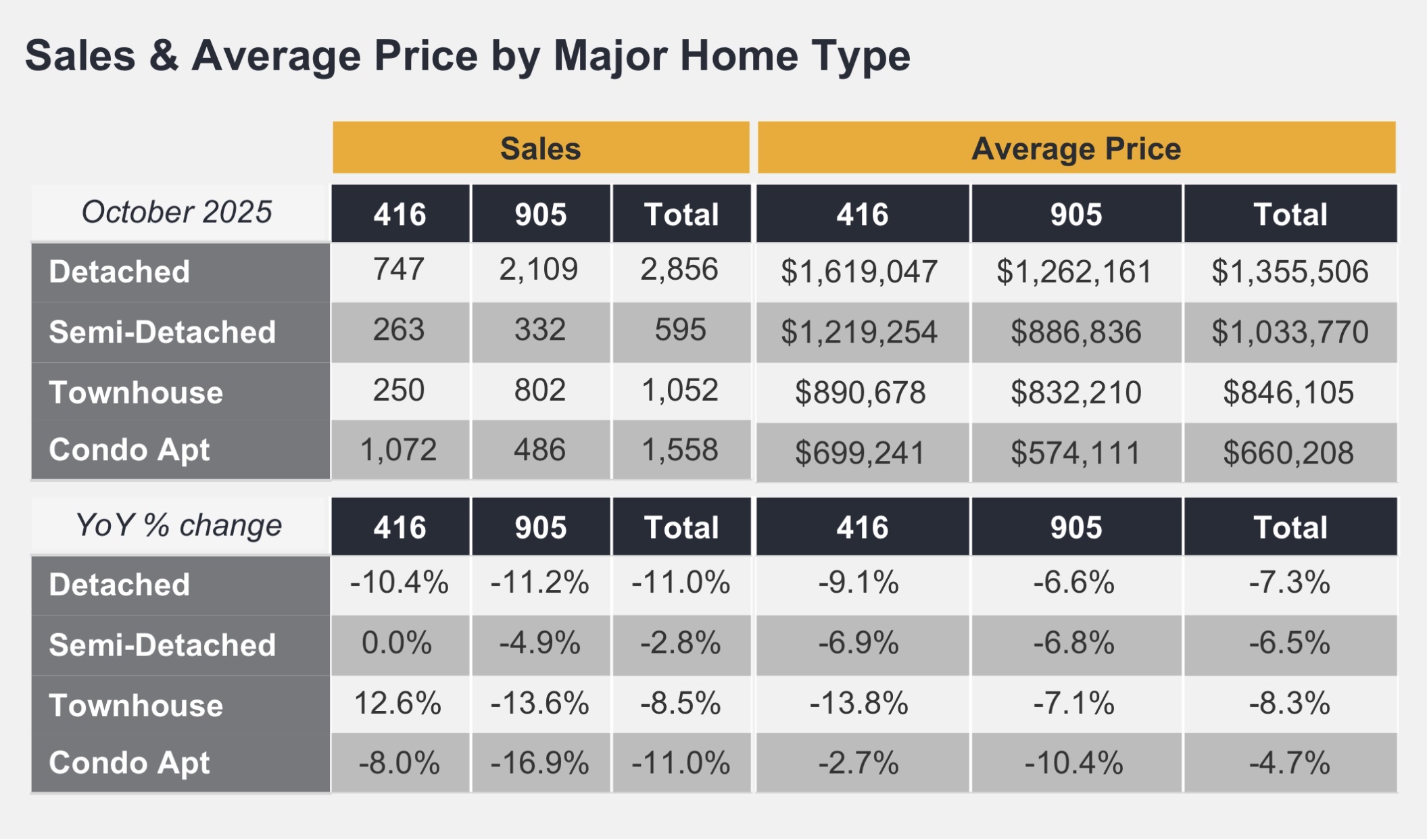

February 2026 Real Estate Market Update: A Season of Shift 🏡

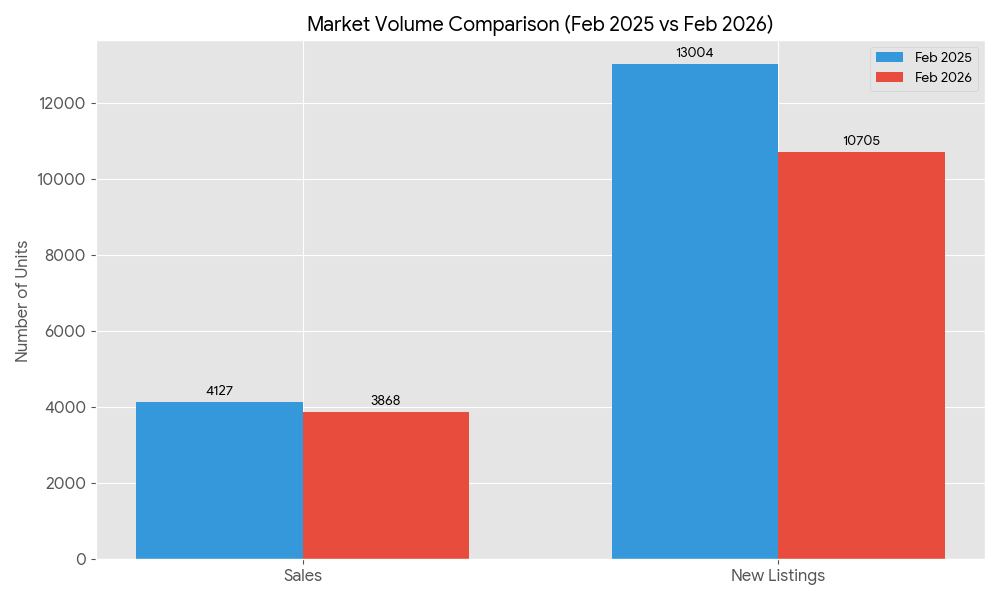

The Greater Toronto Area (GTA) resale housing market in February 2026 was characterized by tightening conditions, as a significant drop in new listings outpaced the decline in home sales. While overall sales volume decreased by 6.3% year-over-year, new listings saw a much sharper decline of 17.7%.

Wondering how the recent market shift has impacted your property’s bottom line? Get an instant update on your equity here: Free Home Evaluation 📈

Key Market Statistics

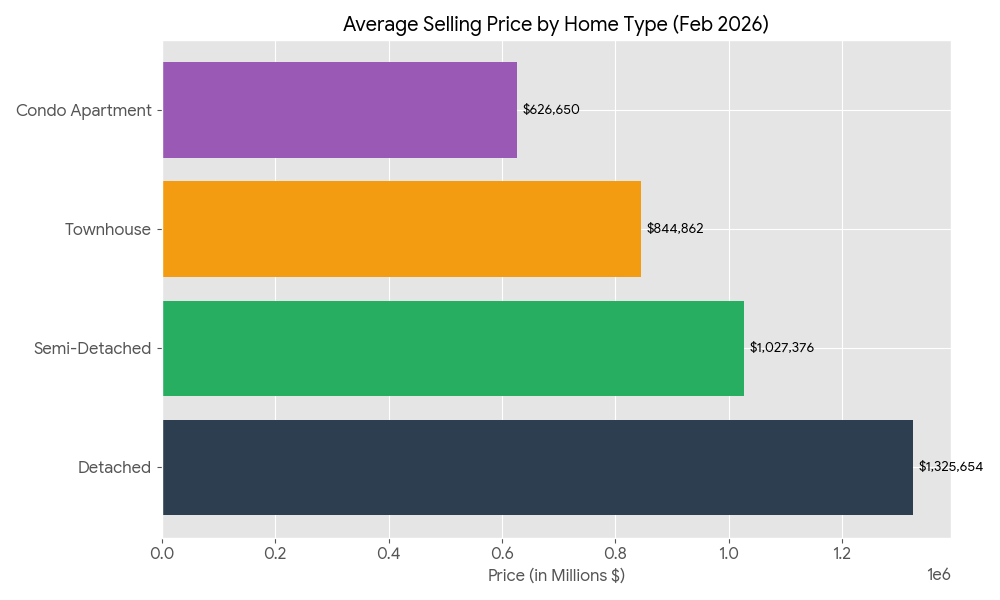

Average Selling Price: $1,008,968 (down 7.1% from February 2025).

A quick-reference guide for your readers to see exactly where average prices landed in February 2026. It showcases the price hierarchy from Detached homes at $1,325,654 down to Condo Apartments at $626,650. This is an essential “anchor” visual for any market update.

Thinking of moving this spring? Step one is knowing your numbers. Start your journey with a FREE Professional Home Evaluation today! 🏠

Total Home Sales: 3,868 reported transactions.

New Listings: 10,705 properties entered the market.

This chart highlights the most significant trend of the month: the massive drop in new supply. While sales dipped by 6.3%, new listings plummeted by 17.7%. This visual clearly shows that while the market is “slower,” the lack of inventory is actually tightening market conditions.

With new listings down 17.7%, your home has less competition than it did last year. See what your home is worth in today’s tight market: Quick Home Values ✨

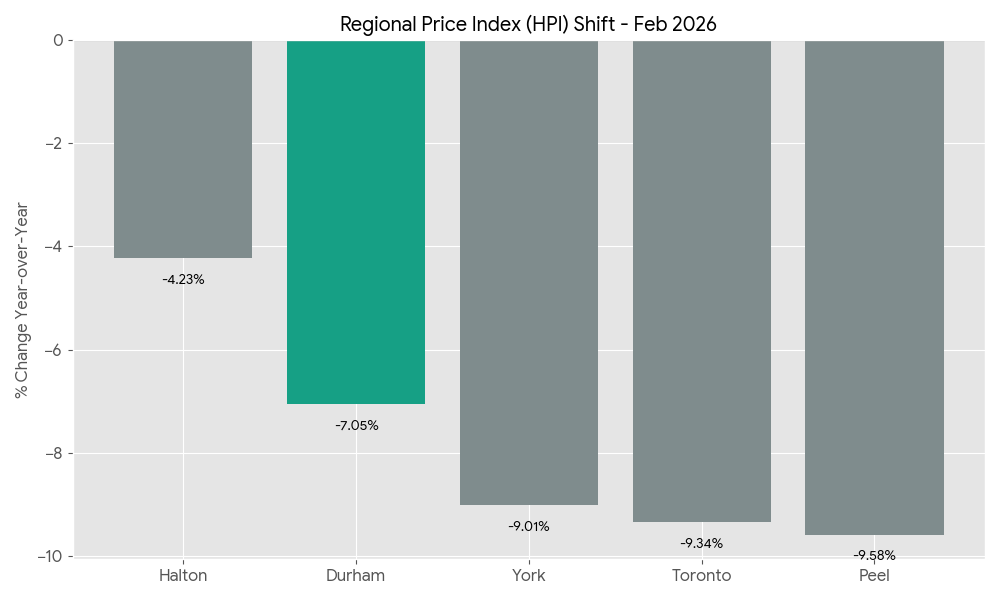

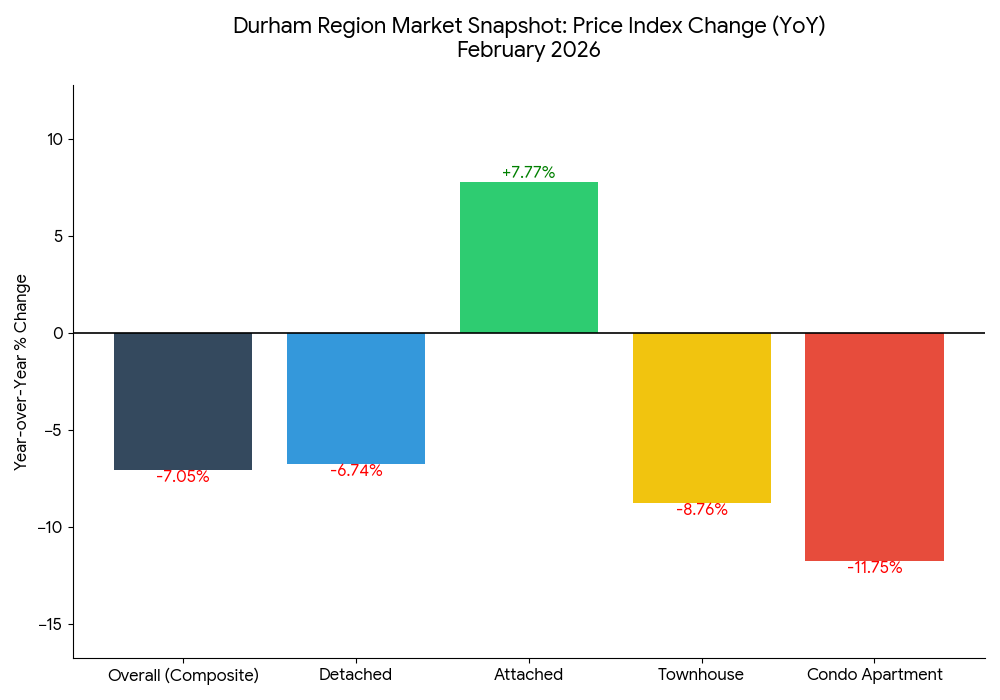

Price Index: The MLS® Home Price Index (HPI) Composite benchmark dropped by 7.9% year-over-year.

This chart focuses on the MLS® Home Price Index (HPI), which tracks the value of a “benchmark” home. I’ve highlighted the Durham Region specifically—with its 7.05% year-over-year dip , it is actually performing better (retaining more value) than the City of Toronto (-9.34%) or Peel Region (-9.58%).

The Durham market is moving fast—don’t rely on old data. Get a real-time valuation of your home based on February’s latest sold prices: Click Here 🔍

Regional & Property Performance

While the overall market is adjusting, Durham Region is showing some fascinating resilience in specific sectors. Here is the year-over-year price index change for February 2026:

Overall Market (Composite): Down 7.05%. with detached homes down 6.74% and apartments down 11.75%.

Detached Homes: Down 6.74%. Remained the most expensive segment with a GTA average of $1,325,654.

Single Family Attached: A surprising increase of 7.77%, showing strong demand for this specific segment.

Townhouses: Down 8.76%.

Condo Apartments: Saw the largest adjustment at -11.75%. Saw the largest volume of sales in the City of Toronto (733 sales) with a GTA-wide average price of $626,650.

TRREB analysts suggest that over 100,000 potential buyers are currently on the sidelines waiting for prices to stabilize and trade conditions to improve. If inventory levels remain low through the spring, increased competition is expected to drive a recovery in both sales and prices during the second half of 2026

With over 100,000 buyers currently waiting on the sidelines, now is the time to beat the rush. Secure your spot in the market today: Search Homes Now 🏃♂️

The latest figures from the Toronto Regional Real Estate Board (TRREB) are in for February 2026, and the data reveals a market that is undergoing a notable recalibration. While the pace of activity has softened compared to last year, the tightening of inventory is creating a unique dynamic for both buyers and sellers.

Is 2026 your year to sell? With experts predicting a surge in the second half of the year, find out your starting point now:Free Evaluation ⏳

The Big Picture: Sales and Pricing Trends

The headline story this month is a pull-back in overall volume. Home sales across the region totaled 3,868, representing a 6.3% decrease compared to the 4,127 sales recorded in February 2025.

This cooling trend is also reflected in property values. The average selling price for a home now sits at $1,008,968. This is a 7.1% dip from the February 2025 average of $1,086,586. For savvy buyers, this price adjustment may offer a strategic window of opportunity that wasn’t available during the peaks of the previous year.

Average prices have adjusted by 7.1% compared to last year. Find the best deals in your favorite neighborhood before they’re gone: View Current Listings📉

Breakdown by Property Type

Understanding the market means looking at the specific segments where you live and shop. Here is how the average prices and sales volume shook out this February:

Property Type

Average Selling Price

Total Sales Volume

Detached

$1,325,654

1,683 Sales

Semi-Detached

$1,027,376

336 Sales

Townhouse

$844,862

698 Sales

Condo Apartment

$626,650

1,088 Sales

Don’t let low inventory stop you! New listings are hitting the market every day. Browse the freshest Durham Region homes for sale right here:Start Your Search 🕵️♂️

The Inventory Crunch: New Listings on the Rise?

Perhaps the most significant statistic this month is the sharp decline in new inventory. There were only 10,705 new listings brought to market in February, a substantial 17.7% drop from the 13,004 listings seen in the same month last year.

This scarcity of new options is a critical factor for anyone planning a move. With fewer homes entering the market, competition for well-priced, high-quality listings remains steady.

Looking for a detached home or a sleek condo? Filter your search by property type and price to find your perfect match: Custom Home Search 🏢

The Sales-to-New-Listings Ratio (SNLR) is a key indicator used to determine if we are in a “Buyer’s,” “Seller’s,” or “Balanced” market.

February 2026: 36%

February 2025: 32%

Interestingly, even though total sales are down, the ratio has actually increased to 36%. This means that while fewer people are buying, even fewer people are selling, which effectively keeps the market from swinging too far into “Buyer’s Market” territory.

Your next chapter starts with a single click. Explore every active listing in the GTA and Durham Region on my easy-to-use portal: GeraldLawrence.Realtor/Search🥂

What This Means for You

For Sellers: Low inventory is your greatest ally. With 17.7% fewer homes to compete against, your property has a better chance of standing out, provided it is priced correctly for the current $1M+ average environment.

For Buyers: The 7.1% decrease in average price is a welcome relief. However, with fewer new listings hitting the wire, you’ll need to be decisive and have your financing in order to move quickly when the right home appears.

The real estate market inside scoop for the community you love. See homes that are for sale and have recently sold. Find out if home sales in your neighbourhood are trending up or down. See what homes around you are currently selling for.

The year 2025 began not with a bang of renewed activity, but with a quiet, persistent rustle of spreadsheet calculations echoing across the Greater Toronto Area (GTA). In a small, two-bedroom rental in Leslieville, Sarah and Mark—a couple in their early thirties—stared at a closing statement for a mid-sized townhouse in Durham Region that they had finally decided not to sign. Despite the Bank of Canada’s aggressive rate-cutting cycle, which saw the overnight rate retreat to 2.25% by late October, the fundamental math of the Toronto dream had changed. For Sarah and Mark, the relatable scenario was one of “cautious hesitation,” a sentiment shared by thousands of prospective buyers who found that even as borrowing costs eased, the cumulative weight of years of inflation on groceries and essentials had permanently altered their debt-service ratios. This was the year of the Great Rebalancing—a period where the emotional urgency of the pandemic era was replaced by a disciplined, strategy-first approach to property.

For sellers, the narrative was equally transformative. Consider the Hendersons in Uxbridge, who had watched their neighbors sell for record highs in 2022. Listing their detached home in early 2025, they were forced to confront a market where “active listings” had surged to levels not seen since 2009. Instead of a weekend bidding war, they faced an average of 31 to 34 days on the market and buyers who insisted on home inspections and financing conditions. This report serves as a definitive professional autopsy of the 2025 market, designed to provide institutional-grade clarity for buyers seeking entry, sellers navigating a reset, and renters finding their first real taste of leverage in a decade. By synthesizing thousands of data points from the Toronto Regional Real Estate Board (TRREB), the Massachusetts Institute of Technology (MIT), and federal housing agencies, this analysis establishes the 2025 market as a foundational pivot toward a more predictable, yet structurally different, 2026.

The Macroeconomic Crucible: Navigating Trade Headwinds and Fiscal Shifts

The performance of the GTA housing market in 2025 was fundamentally underpinned by a broader Canadian economy grappling with what the Bank of Canada described as a period of “subdued growth”. The national landscape was marred by trade uncertainty, particularly regarding widespread U.S. tariffs on steel, aluminum, and automotive sectors—industries that form the backbone of Southern Ontario’s industrial base. Real GDP for Canada contracted by 1.6% in the second quarter of 2025, a shock primarily attributed to declining exports and a pullback in business investment. This cooling at the federal level trickled down to the provincial economy, where Ontario’s real GDP growth was projected to decelerate to a modest 0.8% for the year.

For the real estate professional, these figures were more than just abstract statistics; they were the primary drivers of consumer confidence. The Toronto Census Metropolitan Area (CMA) faced a persistent labor market lag, with an annual unemployment rate standing at approximately 9.4% by the fourth quarter—a figure significantly higher than the national average of $6.9\%$. This disparity created a “confidence gap” where, despite falling mortgage rates, many households were reluctant to commit to long-term financial obligations while the industrial and manufacturing sectors faced structural headwinds.

Monetary Policy and the Affordability Paradox

The Bank of Canada’s monetary response was the primary catalyst for market stabilization. By October 29, 2025, the benchmark rate had been cut to 2.25%, a cumulative drop of 2.75% from the 5.0% peak seen in early 2024. This led to a significant easing in the mortgage landscape, with five-year insured fixed rates dipping as low as $3.69% and variable rates hitting 3.45%. However, the anticipated “flood of buyers” failed to materialize in the first half of the year. The reason, as analyzed by TRREB and Ipsos, was that while interest rates were falling, home prices had not yet corrected enough to offset the increased cost of living.

Economic Indicator

2025 Full Year (Estimated)

2024 Full Year (Actual)

Impact Direction

Canada Real GDP Growth

0.75%

1.1%

Negative/Slowing

Ontario Real GDP Growth

0.8%

1.4%

Negative/Slowing

Toronto Unemployment Rate

9.4%

8.2%

Negative/Rising

BoC Overnight Rate (Year-End)

2.25%

5.0%

Positive/Falling

CPI Inflation (Ontario Avg)

1.9%

2.4%

Positive/Stabilizing

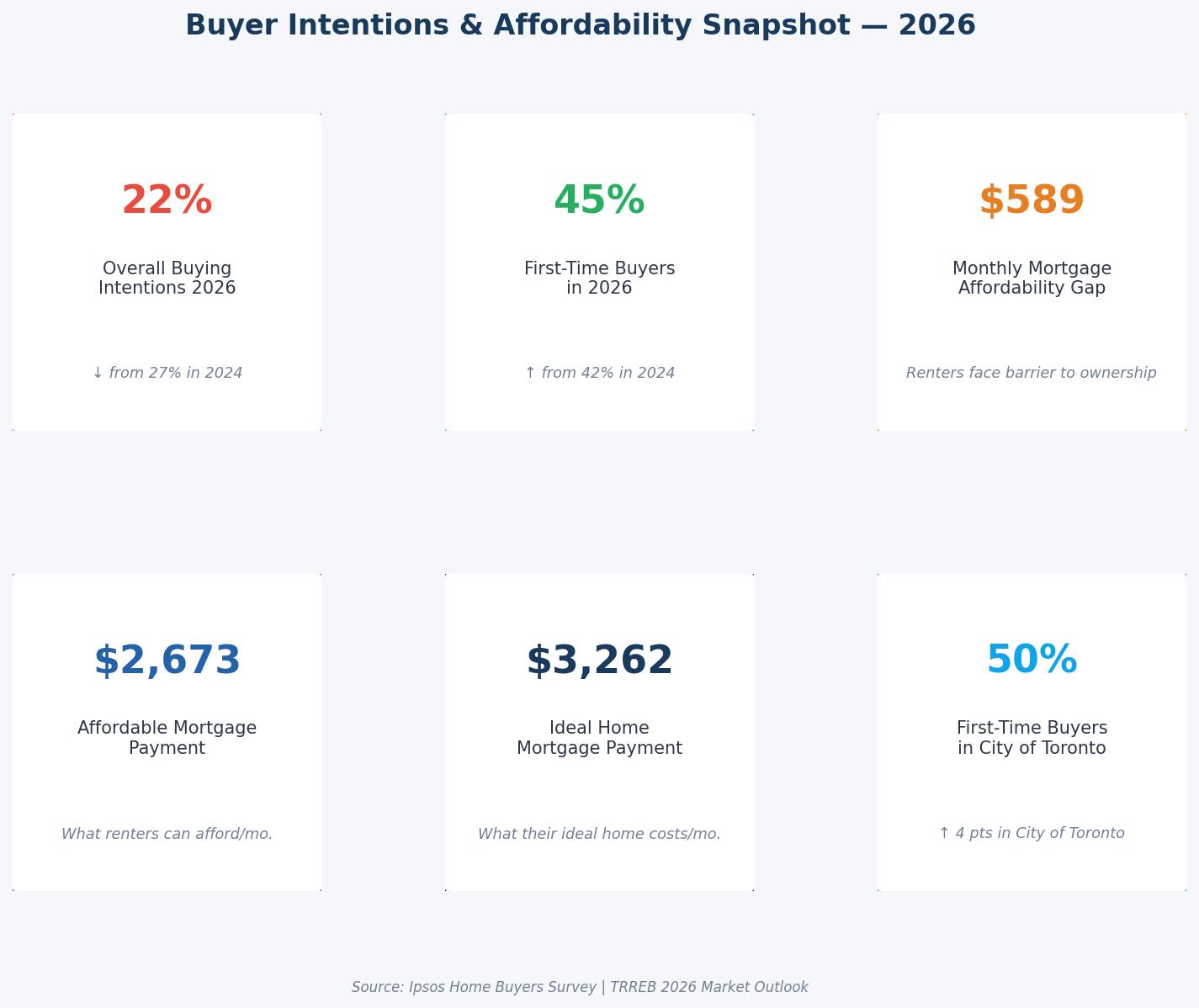

The analysis suggests that 2025 was the year the “Pressure Point”—the intersection of housing supply, migration, and the missing middle—became the central focus of policymakers. While inflation moderated to near the 2% target, the cumulative effect of the previous years’ price surges left household budgets permanently elevated. Groceries remained 25%-30% more expensive than in 2019, and GTA rents had climbed 40% over the same period, creating a “trap” for renters who wished to save for a down payment but were consumed by monthly carrying costs.

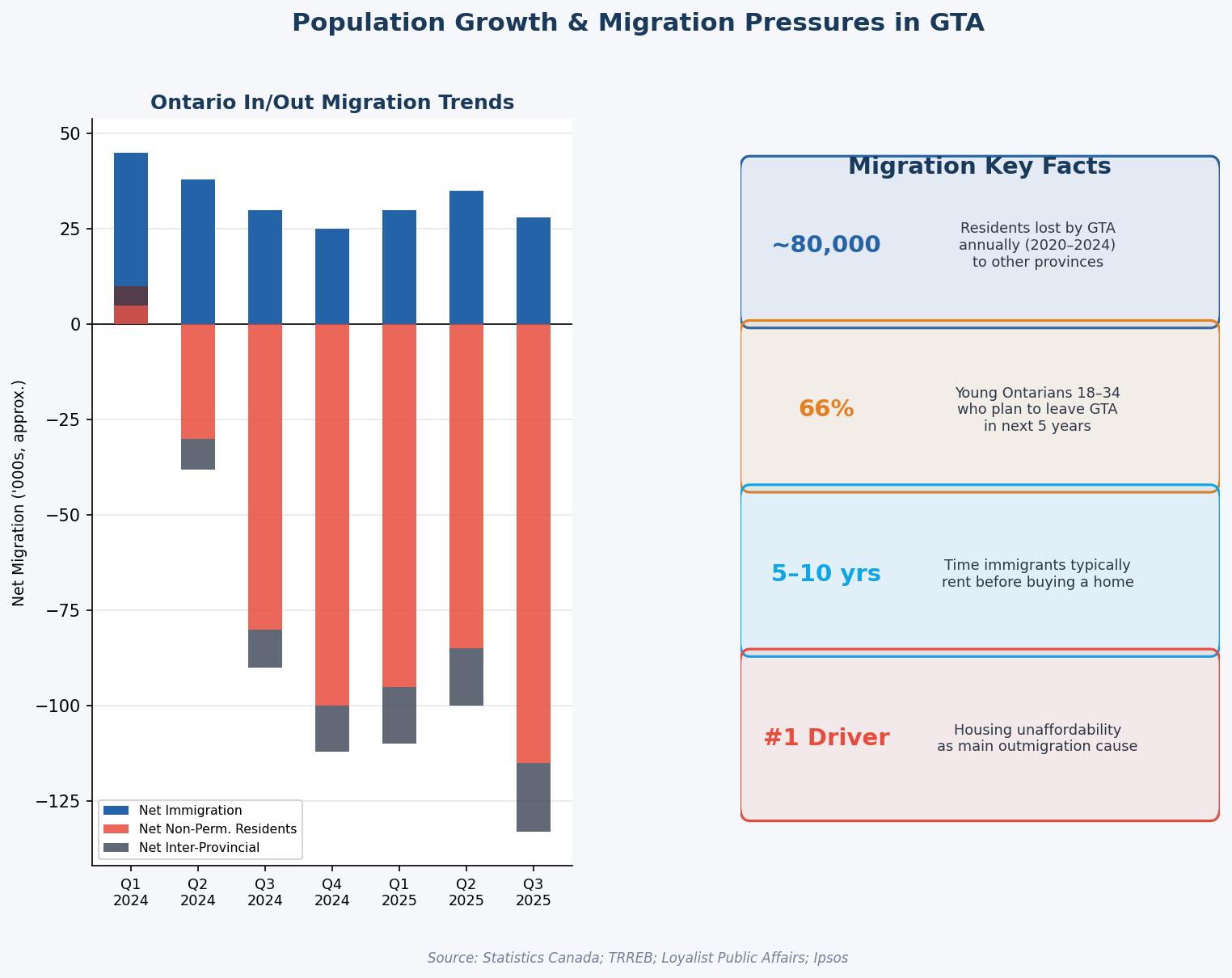

The Migration Phenomenon: The Erosion of the Urban Premium

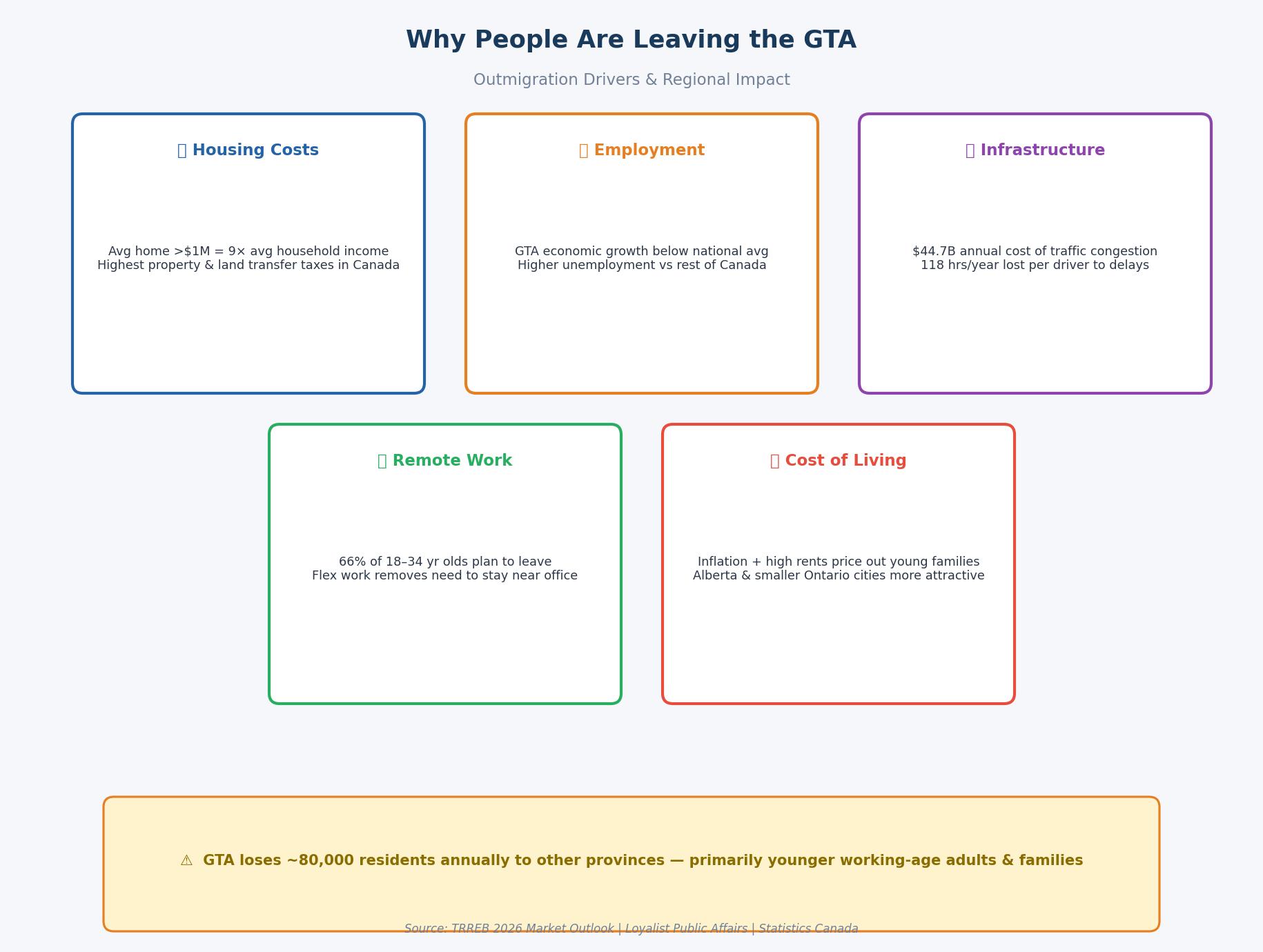

A defining characteristic of 2025 was the acceleration of outmigration from the GTA. Excluding international immigration, the region lost an average of 80,000 residents annually to other parts of Ontario and the rest of Canada. This movement was not merely a lifestyle choice but a fiscal necessity. The “urban premium”—the idea that living in Toronto was worth the exorbitant cost for the sake of proximity to jobs—began to dissolve under the weight of remote work and infrastructure failure.

The Cost of Congestion and Infrastructure Stagnation

For the average professional, the GTA’s infrastructure became a primary driver of relocation. Toronto’s traffic congestion was ranked among the worst in North America, with drivers losing approximately 118 hours each year to delays. This was not just a frustration; it was an economic drain, costing the region roughly $44.7 billion annually in combined social and economic losses. Ipsos polling indicated that 53% of residents had considered leaving the GTA specifically because of gridlock.

The normalization of remote and hybrid work provided the “escape hatch” residents needed. By late 2024, 28.8% of the Toronto labor force worked in a hybrid or fully remote capacity. This enabled a mass exodus of young families and professionals to more affordable communities where they could access larger living spaces without sacrificing their Toronto-based salaries.

The Alberta and Small-Town Ontario Allure

The financial incentive to relocate was most apparent when comparing the carrying costs of homeownership across Canadian jurisdictions. A household moving from Toronto to Calgary or a mid-sized Ontario city like Uxbridge or London found immediate relief in lower property taxes and the absence of a municipal land transfer tax.

Ownership Cost Factor

City of Toronto

City of Calgary

City of Mississauga

Avg. Home Price (Sept 2025)

$1,089,918

$615,005

$969,501

Res. Property Tax Rate

0.7541%

0.6180%

1.0338%

Estimated Annual Tax

$8,219

$3,990

$9,950

Land Transfer Tax (LTT)

Double (Prov + Mun)

No LTT (Title Fee Only)

Single (Prov Only)

The evidence indicates that a Toronto homeowner pays roughly double the annual property tax of a comparable Calgary homeowner, while a Mississauga homeowner pays nearly three times more. This recurring financial burden, when layered onto elevated mortgage and utility costs, became a primary catalyst for outmigration among the 66% of young Ontarians (aged 18-34) who expressed a desire to leave the region.

Residential Segments: A Tale of Two Markets

The 2025 residential market was a study in contrasts, characterized by a resilient but normalizing freehold sector and an oversupplied, investor-strained condominium segment.

Freehold Resilience: The Detached and Semi-Detached Reset

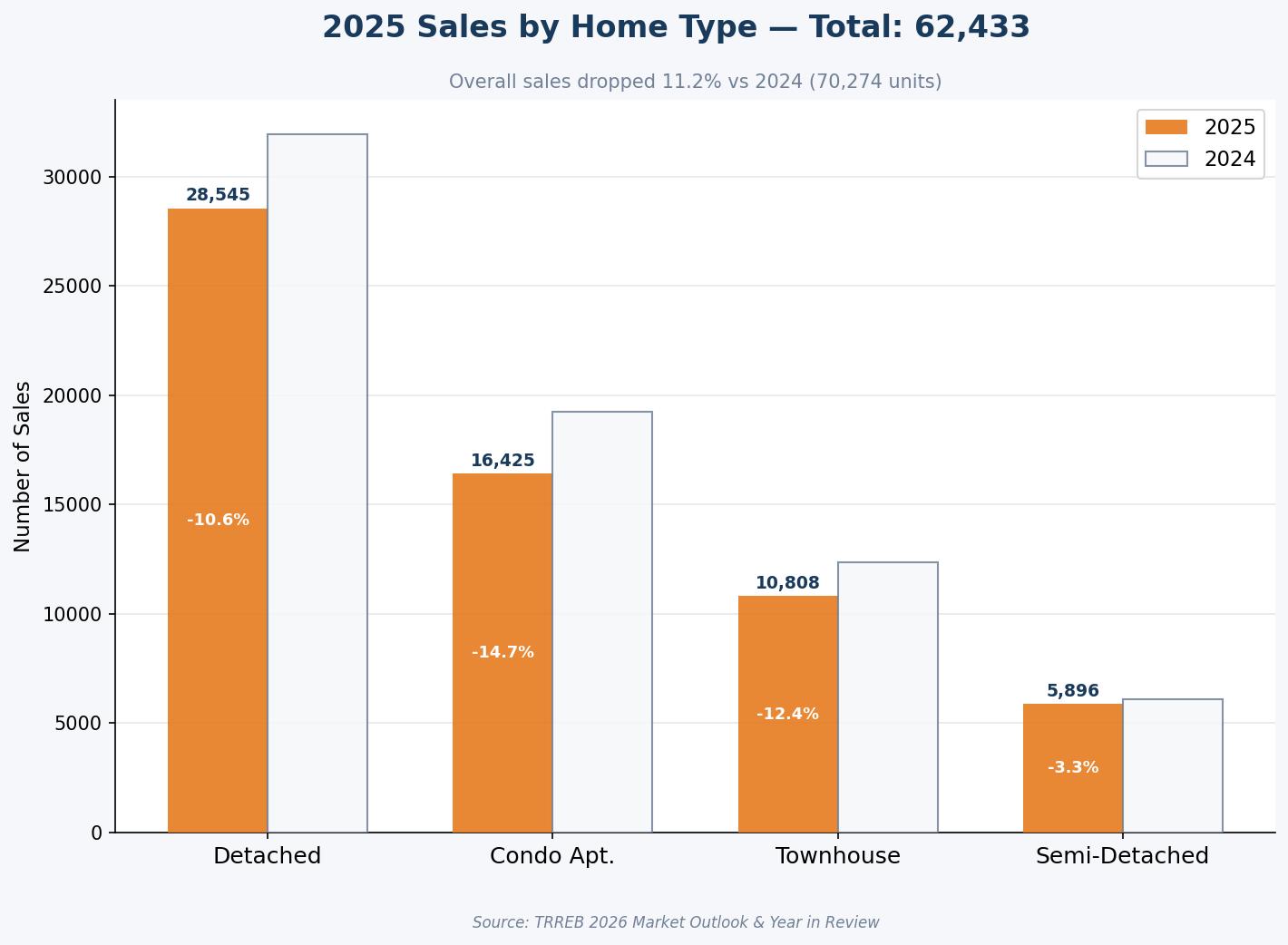

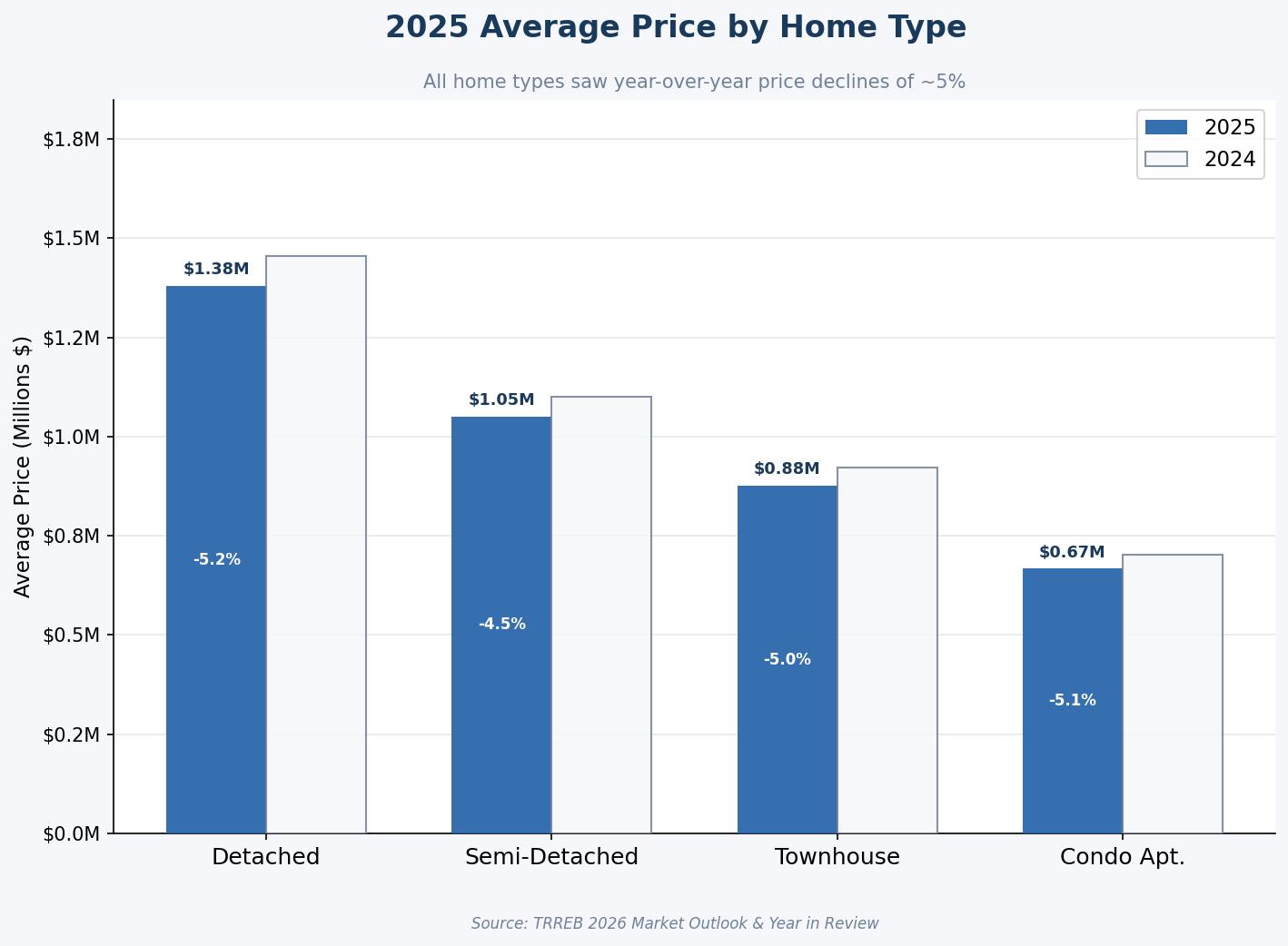

Detached homes remained the most coveted asset class in 2025, but they were not immune to the broader market rebalancing. The average price for a detached home in the GTA fell by 5.2% to approximately $1,379,666. This correction was seen by industry professionals as a “reset” rather than a “crash.” Sellers who recognized the shift toward balanced conditions and priced their homes accurately continued to find success, while those anchored to 2022 expectations saw their properties sit for months.

Semi-detached homes and townhouses proved slightly more resilient, with semi-detached prices declining by a more modest 4.5% to $1,050,605. The growth in new listings for these segments—up 17.3% for semi-detached and 9.3% for townhouses—provided move-up buyers with a level of choice that had been absent for the better part of a decade.

The Condominium Crisis: Inventory at a Crossroads

The condominium apartment segment faced the most significant challenges in 2025. Sales volume for condos dropped by $14.7\%$ year-over-year, while the average selling price fell by 5.1% to $667,235. The sector was impacted by a “perfect storm” of factors:

High Listing Inventory: Active listings in the condo segment reached historic highs, giving buyers unprecedented negotiating power.

Investor Pullback: As average rents trended lower and short-term rental regulations tightened, many investors found their units to be cash-flow negative, leading them to list properties rather than continue to hold.

The First-Time Buyer Gap: Despite being the most affordable housing type, Ipsos polling found a persistent gap of approximately $600 between what typical renter households could afford for a monthly mortgage and the actual cost of a condo unit.

Housing Type

2025 Avg. Price

2024 Avg. Price

Price Change (%)

Sales Change (%)

Detached

$1,379,666

$1,456,039

-5.2%

-10.6%

Semi-Detached

$1,050,605

$1,099,883

-4.5%

-3.3%

Townhouse

$876,354

$922,207

-5.0%

-12.4%

Condo Apartment

$667,235

$702,943

-5.1%

-14.7%

The data suggests that the condo market in 2025 became a “buyer’s playground,” where offer conditions and price negotiations replaced the bidding wars of the past. For buyers like Sarah and Mark, this segment finally offered a point of entry, provided they were willing to navigate the complexities of high maintenance fees and building-specific financials.

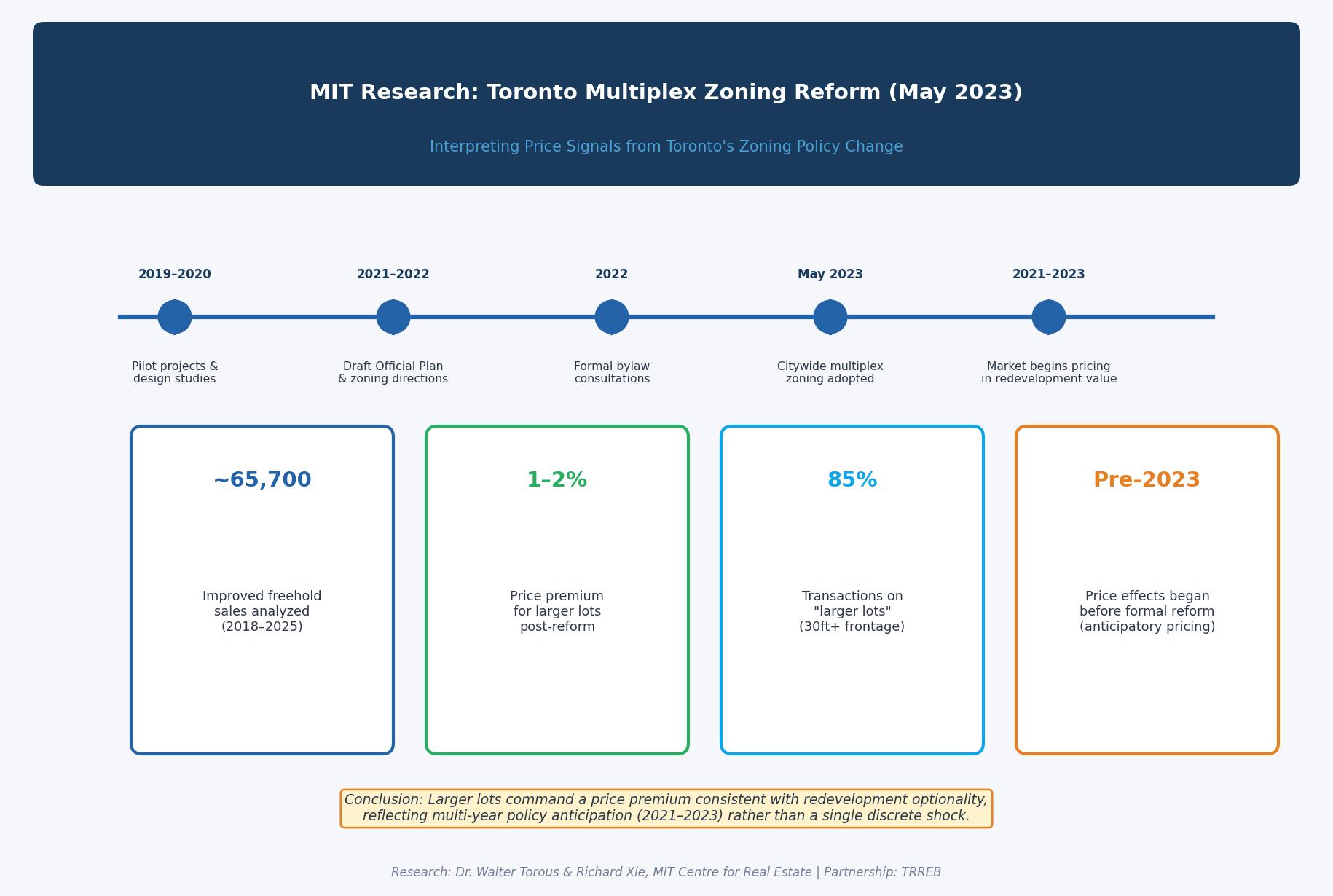

Policy and Planning: The Multiplex Zoning Experiment

One of the most profound shifts in the Toronto planning landscape occurred in May 2023, when the city adopted a citywide zoning reform allowing two- to four-unit residential buildings (“multiplexes”) as-of-right. In 2025, researchers from MIT’s Centre for Real Estate published an exploratory assessment of how this policy was being reflected in land values.

MIT Research Findings on Land Value

The analysis, which utilized approximately 65,700 improved freehold sales within Toronto between 2018 and 2025, sought to determine if the “optionality” of building a multiplex was being priced into the market.

Larger Lots: The study defined “larger lots” as those with a frontage of at least 30 feet or an area of at least 3,000 square feet. These lots represent roughly 85% of the transactions in Toronto’s low-rise neighborhoods. Price Signal: The baseline model estimated a modest 1%-2% relative price increase for larger lots following the reform.

The Anticipation Effect: A critical insight from the MIT research was that the price gap between larger and smaller lots began widening as early as 2021-2022. This suggests that the market had already “priced in” the multiplex reform through years of public signals, pilot projects, and policy discussions before the formal bylaw was ever enacted.

The evidence indicates that while zoning reform is a necessary step toward addressing the “missing middle,” the market’s response is gradual and influenced by broader economic factors like construction costs and interest rates. For the homeowner, this means that while their lot might have gained some “redevelopment value,” the ability to realize that value depends on site-specific buildability and current financing conditions.

Fiscal Policy: Tax Relief and the Cost of Development

In a year defined by affordability concerns, governments at all levels were forced to take action. The 2025 Federal Budget and the Ontario Fall Economic Statement introduced several measures designed to lower the barrier to entry for first-time buyers.

The GST/HST Rebate Revolution

Effective May 27, 2025, the federal government introduced a 100% rebate of the 5% federal GST on newly built homes priced up to $1 million for first-time buyers. This initiative was designed to encourage new home construction and provide significant upfront relief—up to $50,000—to buyers. The Ontario government mirrored this at the provincial level, announcing the removal of the provincial 8% HST portion for first-time buyers of new homes effective January 1, 2026. Together, these rebates represent a massive reduction in closing costs for the “missing middle” segment, where new homes often hover between $800,000 and $1.2 million.

The Burden of Development Charges

Despite these tax cuts, the cost of bringing new supply to market in the GTA remained punishingly high. Development charges—fees collected from developers to fund municipal infrastructure—saw significant increases.

Low-Rise Homes: Average charges in the GTA hit $123,649 per unit in 2025, an increase of $42,000 since 2022.

High-Rise Homes: Average charges hit $68,608 per unit, up $32,000 since 2022.

The analysis suggests a stark disparity between the GTA and competing regions like Calgary, where off-site levies averaged just $22,600 per unit. This cost-of-growth imbalance is a primary reason why new home sales slowed in 2025, as developers struggled to maintain project viability while buyers faced reduced purchasing power.

The Rental Market: A Shift in the Balance of Power

For several years, the GTA rental market had been defined by ultra-tight conditions and soaring rents. In 2025, that dynamic began to shift as supply growth met a cooling of demand.

The Vacancy Surge and the “Filtering Effect”

According to CMHC and TRREB reports, the national purpose-built rental vacancy rate rose to 3.1% in 2025, up from 2.2% in 2024. In the GTA, the rental inventory remained historically high due to a wave of condominium completions and the entry of new purpose-built rental units. This surge in supply created a “filtering effect.” As high-end, newly completed units hit the market, landlords were forced to offer incentives like one or two months of free rent to attract tenants. This, in turn, allowed tenants to move from older, less-efficient buildings into higher-quality units without the “rent shock” that had characterized previous moves.

Rental Prices and Negotiating Power

Average rents in the GTA trended lower on a year-over-year basis for the first time in the post-pandemic era. In the second quarter of 2025, average one-bedroom rents were down 5.1% to $2,326, while two-bedroom rents dropped 3.5% to $3,066. The inventory of units listed for rent grew by 16% year-over-year, significantly outpacing the growth in rental transactions. For the renter, this meant that the power dynamic had shifted from the landlord to the tenant. The evidence indicates that even in the secondary rental market (condo rentals), vacancies rose, and owners became more flexible on terms to avoid units sitting empty.

Rental Segment (GTA)

Q2 2025 Avg Rent

Q2 2024 Avg Rent

YoY Change

Bachelor

$1,873

$1,972

-5.0%

1-Bedroom

$2,326

$2,452

-5.1%

2-Bedroom

$3,066

$3,178

-3.5%

3-Bedroom

$3,924

$3,972

-1.2%

The analysis highlights that while permanent residents through immigration helped keep transaction volumes above 2024 levels, the dip in temporary residents—students and temporary workers—removed a significant layer of competition from the bottom of the market.

Regional Deep Dives: The Durham and Uxbridge Micro-Markets

While the broader GTA market felt the weight of 2025’s economic headwinds, certain pockets showed remarkable resilience and localized dynamism. The Durham Region, in particular, became a focus for families seeking the “missing middle” housing that was increasingly scarce in Toronto.

Durham Region: The Competitiveness Leader

In late 2025, Durham Region led the GTA in buyer competitiveness, boasting the lowest average days on market and a sale-price-to-list-price ratio that remained consistently near parity. Despite a 4.8% decrease in average sale prices year-over-year, detached homes in Durham remained stable, averaging just over $945,000 in October. The region’s attractiveness was driven by a combination of affordability and economic momentum. Durham achieved a record $1.23 billion in non-residential building permits in 2023, signaling a robust economic ecosystem that supports long-term property appreciation.

Uxbridge: A Case Study in Market Reset

Uxbridge Township, known for its rural charm and high-value detached homes, provided a clear snapshot of the “normalization” trend.

Year-End Prices: The average sale price in Uxbridge reached $1,190,682 in December 2025, a marginal 0.32% increase from December 2024.

The “Buyer’s Window”: In January 2026, the average price dipped to $996,667, marking the first time in years that the regional average fell below the $1 million threshold.

Inventory Shifts: Active listings in Uxbridge reached 77 in December, a 40% increase year-over-year, while the average days on market climbed to 64 days.

The data from Uxbridge suggests that while the “lifestyle-driven move” remains a priority for many, buyers are now moving at their own pace, performing due diligence, and negotiating terms that reflect the new interest rate reality.

Infrastructure: The Connectivity Catalyst

A critical “third-order” insight for property values in Durham and Uxbridge is the massive investment in transit connectivity.

Durham-Scarborough BRT: Ground was broken in 2025 on the 36-kilometer dedicated bus rapid transit lane, which is projected to reduce travel delays by 85% along the Kingston Road corridor.

Uxbridge Transit Hub: The upgrade of the local hub, integrating smart ticketing and real-time tracking, is scheduled to reduce travel times to Toronto by 20%, significantly enhancing the “commuter value” of homes in the township.

The professional perspective indicates that homes within walking distance of these hubs are positioned for superior long-term appreciation as the region continues to grow toward a projected population of 1.3 million by 2051.

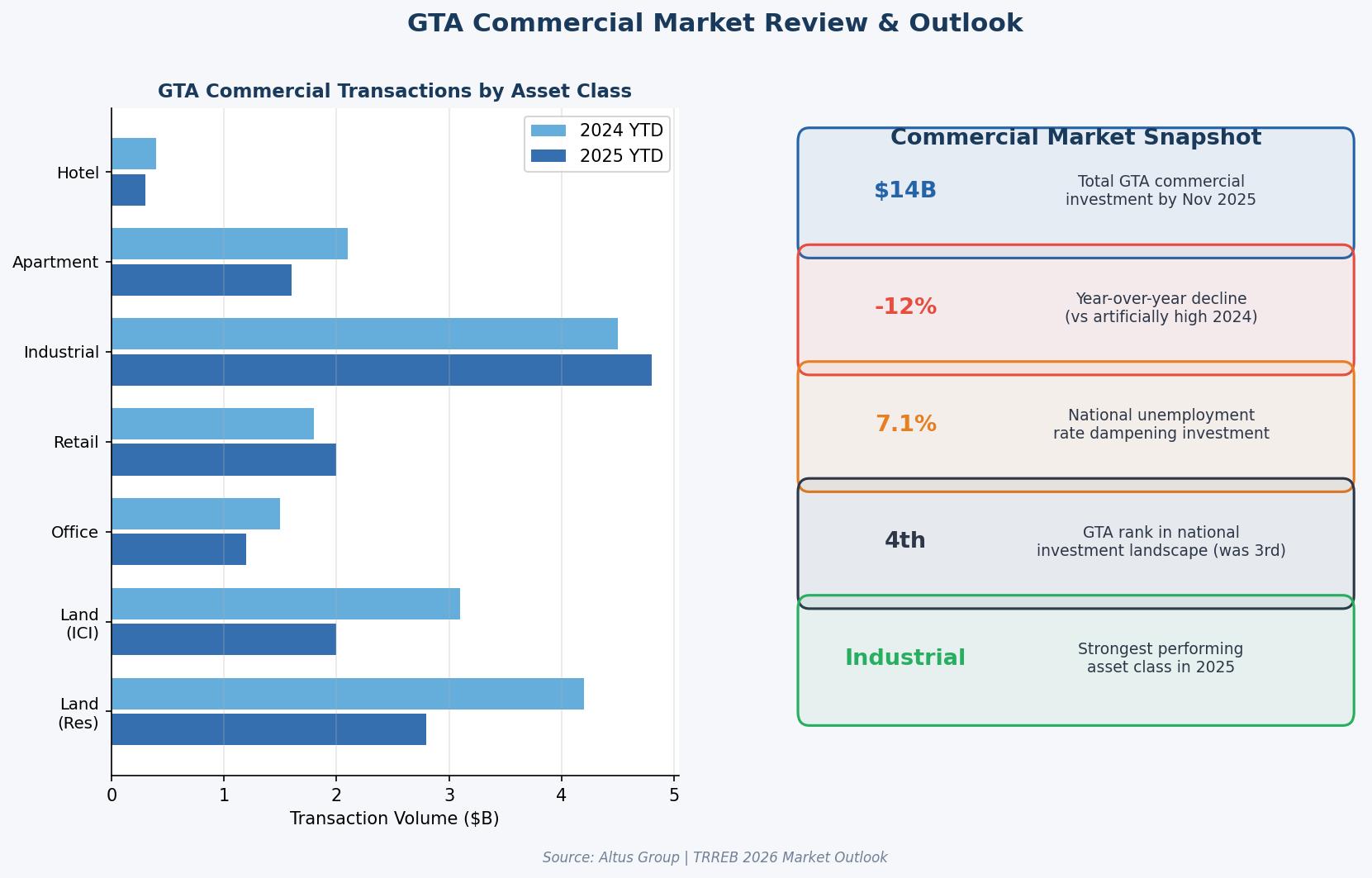

Commercial Real Estate: A Disciplined Holding Pattern

The GTA commercial real estate market in 2025 was a story of “mixed fortunes,” as optimism about improving debt markets clashed with persistent economic uncertainty. Total investment volume reached $2.9 billion in the third quarter, a 6% increase from the previous quarter but still 6% below 2024 levels.

Industrial Dominance

Industrial assets remained the undisputed leader of the commercial landscape, accounting for 51% of all transactions. Investment volume in this sector jumped 22% quarter-over-quarter, driven by a scarcity of high-quality assets. A standout transaction was a $152.5 million self-storage portfolio, which underscored the continued demand for logistical and storage solutions in an urbanizing GTA.

Office and Multi-Residential Challenges

Office investment remained the laggard, down 28% year-over-year. While improved leasing activity offered some hope, the sector continued to struggle with valuation uncertainty. Multi-residential investment also saw a sharp 62% decline from the previous year, although demand for value-add assets remained strong as financing conditions improved. The commercial sector in 2025 was defined by a “disciplined approach,” where investors were extremely selective, focusing on necessity-based assets like grocery-anchored strip malls, which saw a 49% resurgence in deal volume.

Conclusion: Synthesizing the 2025 Experience for the 2026 Horizon

The full year of 2025 represented the most significant structural rebalancing of the GTA real estate market since the 2008 financial crisis. For the first time in a decade, the “fear of missing out” was replaced by “the freedom of choice.” The analysis demonstrates that the 2025 market was not one of collapse, but of “normalization”—a reset that was necessary to create a sustainable foundation for future growth.

For Buyers, 2025 provided the strategic entry window they had been waiting for. More choice, less competition, and improved affordability through both lower mortgage rates and federal tax rebates created a rare moment of leverage. For Sellers, the year was a lesson in realism. Success required a departure from the emotional pricing of the past and a focus on presentation, strategy, and market-accurate valuations. For Renters, the year marked the end of the ultra-tight market. A wave of new supply and a cooling of demand granted them negotiating power and the ability to move into higher-quality housing with incentives.

As we look toward 2026, the evidence suggests that the “Pressure Point” identified by TRREB will remain a central theme. The region’s ability to retain talent and house its growing population depends on continued coordination across all levels of government to streamline development, reduce fees, and incentivize the “missing middle”. For the real estate professional, 2025 was the year we moved from speed to strategy, a shift that will define the winners of the next decade.

Professional Real Estate FAQ: 2025 Year in Review

Is the GTA real estate market currently in a buyer’s or seller’s market?

In 2025, the GTA market shifted into a “balanced” state, with significant pockets of “buyer’s market” conditions, particularly in the condominium and entry-level freehold segments. Inventory reached levels not seen since 2009, granting buyers unprecedented power to include conditions and negotiate prices below list.

How much did home prices actually drop in 2025?

Across the entire GTA, the average selling price for all home types in 2025 was approximately $1,067,968, a decrease of 4.7% from 2024. Detached homes saw the steepest correction at 5.2%, while the condo segment fell by 5.1% due to high inventory levels.

What is the new GST rebate for first-time buyers of new homes?

Introduced in the 2025 Federal Budget, the rebate eliminates the 5% GST for first-time buyers on newly built homes priced up to $1 million. A partial rebate is available for homes up to $1.5 million, providing up to $50,000 in total upfront savings for qualifying purchasers.

Why are so many people leaving the Greater Toronto Area (GTA)?

Outmigration is primarily driven by housing unaffordability, high property taxes, and extreme traffic congestion. Many young professionals and families are using remote work flexibility to relocate to more affordable regions like Alberta or Southwestern Ontario, where the cost of living and property taxes are significantly lower.

Are rents going down in Toronto and the GTA?

Yes, average rents trended lower in 2025 for the first time in several years. Average one-bedroom rents in the GTA fell by 5.1% to $2,326, as a surge in new condominium and purpose-built rental supply gave tenants more choice and negotiating power.

What impact did the multiplex zoning reform have on home values?

MIT research found that Toronto’s 2023 multiplex zoning reform led to a modest 1%-2% relative price increase for “larger lots” (30ft+ frontage). However, much of this value was “priced in” by the market during the policy discussion phase between 2021 and 2022.

How do development charges affect the price of new homes in Ontario?

Development charges in the GTA are among the highest in Canada, averaging $123,649 for a new low-rise home in 2025. These fees have increased by $42,000 since 2022, adding significant upward pressure on the final sale price of new housing supply.

Is now a good time to invest in the Toronto condo market?

The 2025 condo market offered unique opportunities for “value plays,” as high inventory and lower rents pressured some investors to sell. Strategic buyers are finding opportunities in well-located units where supply levels currently allow for deeper negotiations on price and terms.

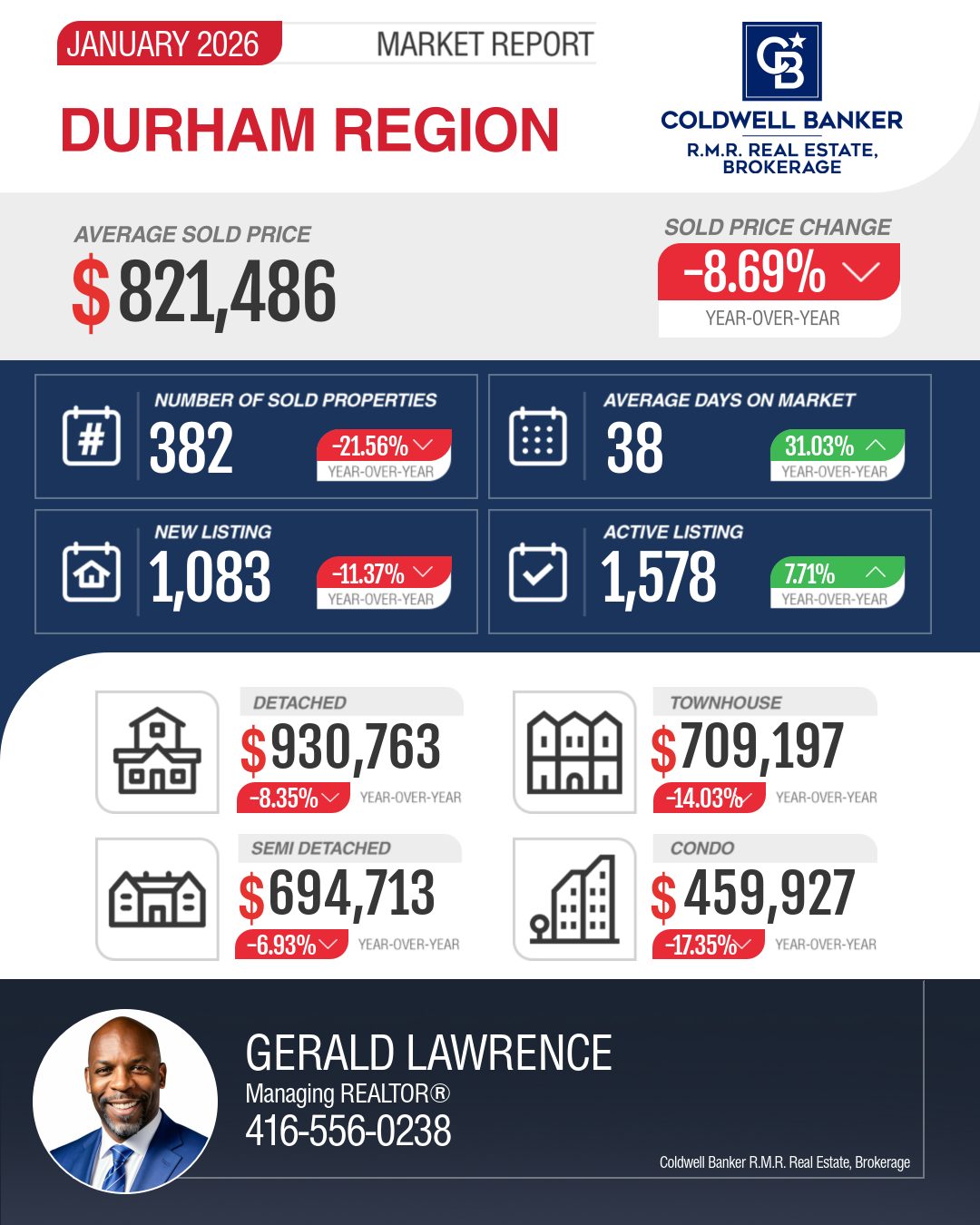

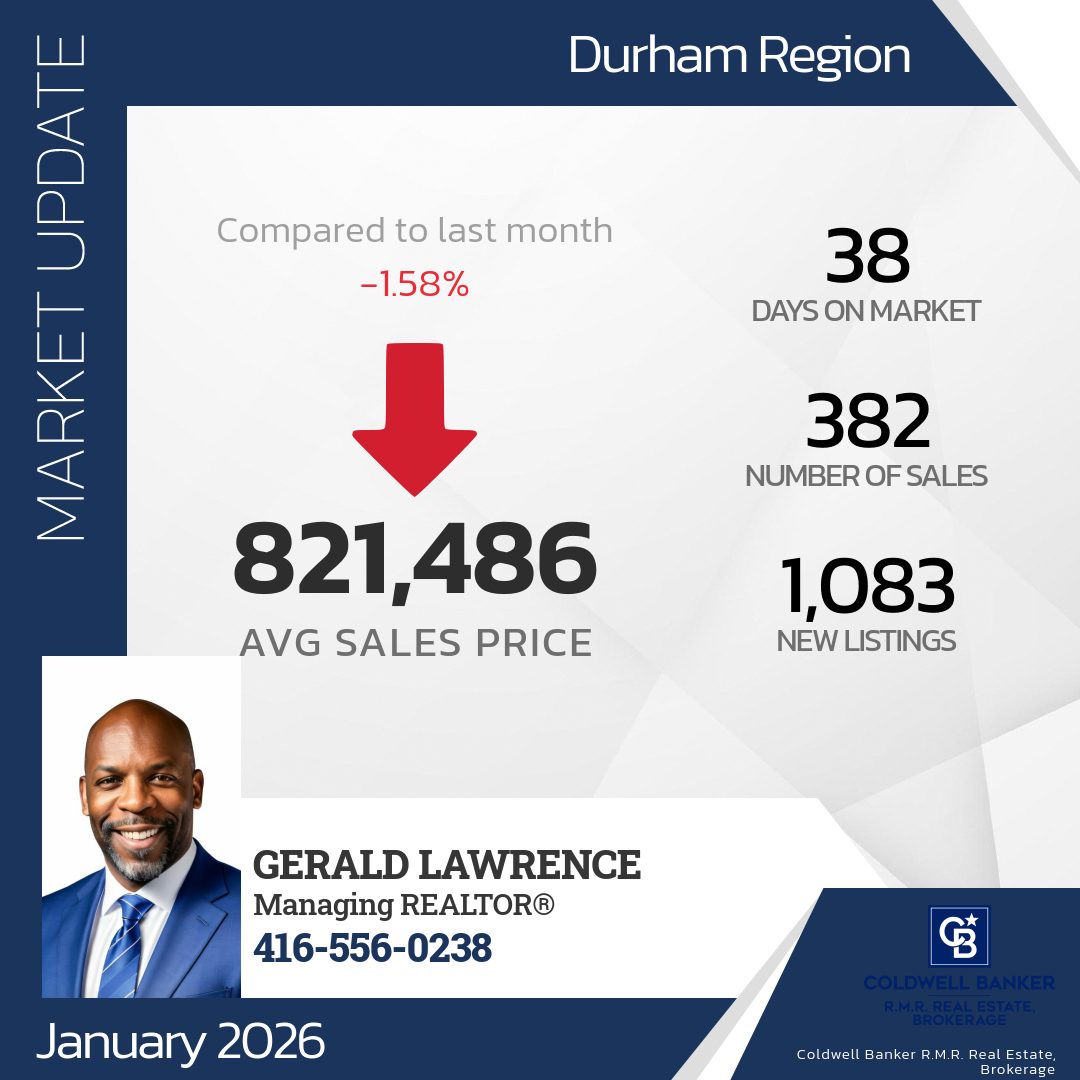

Durham Region Real Estate Market Update: January 2026 Analysis

The January 2026 real estate data for the Durham Region is in, and it paints a picture of a market in transition. Whether you’re looking to buy your first home or sell your current property, understanding these shifts is crucial for making informed decisions.

Here’s a breakdown of the key stats and what they mean for you:

The Big Picture: Prices and Volume

Average Price: The average home price in Durham for January 2026 was $822,185. This represents a slight dip of 1.9% from December 2025 and a more significant 9.2% decrease compared to January 2025.

Median Price: The median price followed a similar trend, sitting at $776,000, down 1.5% month-over-month and 7.6% year-over-year.

Inventory Surge: We saw a massive jump in new listings, with 1,150 new properties hitting the market—a 107.6% increase from December. However, overall transaction volume remained lower than last year, with 408 sales (down 17.9% YoY).

Days on Market: Homes are staying on the market longer. The average time to sell is now 41 days, up nearly 34% from the same time last year.

What This Means for Buyers

If you’ve been waiting on the sidelines, the January data offers some encouraging news. The market is shifting in a way that gives buyers more breathing room and leverage.

More Choice: The explosion in new listings (up over 100% from last month) means you finally have more inventory to browse. You aren’t forced to compete for the same two or three houses.

Negotiating Power: With nearly 79% of homes selling below the list price and an average Sale Price to List Price (SP/LP) ratio of 97.9%, the “bidding war” era has cooled significantly. Sellers are increasingly open to offers below the asking price.

Time is on Your Side: With homes sitting for an average of 41 days, you have more time to conduct due diligence, schedule second viewings, and ensure the home is the right fit without the pressure of an immediate deadline.

Buyer Strategy: Focus on properties that have been on the market for 30+ days. These sellers may be more motivated to negotiate on price or terms.

What This Means for Sellers

Selling in the current market requires a shift in strategy compared to the highs of early 2025. While prices have softened, the market remains active for well-positioned properties.

Realistic Pricing is Critical: The average list price ($953,844) is significantly higher than the average sale price ($822,185). Overpricing your home in this market can lead to it sitting stagnant, as evidenced by the increase in Days on Market and the 432 terminations seen this month.

Presentation Matters: With more competition (listings) and fewer active buyers (lower volume), your home needs to stand out. Professional staging, high-quality photography, and minor repairs are no longer optional—they are essential to attract serious offers.

Expect Negotiations: Only 17.2% of homes sold above the list price this month. Be prepared for offers that include conditions and come in slightly below your asking price.

Seller Strategy: Price your home according to current sold data, not active listings. A “sweet spot” price will generate interest early, which is vital when buyer attention is spread thin across many new listings.

The Bottom Line

The Durham Region is currently a “Balanced to Buyer-Leaning” market. While prices have corrected from last year’s peaks, the increase in inventory and the slower pace of sales create a more stable environment for everyone involved.

Ready to Make Your Move?

For Buyers: Don’t miss out on the best selection of inventory we’ve seen in months! [Contact me today] for a curated list of homes in your favorite Durham neighborhood and let’s get you a deal below the asking price.

For Sellers: In a competitive market, your strategy is everything. [Click here for a Free Home Evaluation] to see what your property is worth in today’s shifting market and learn how our marketing plan can get your home sold while others sit on the market.

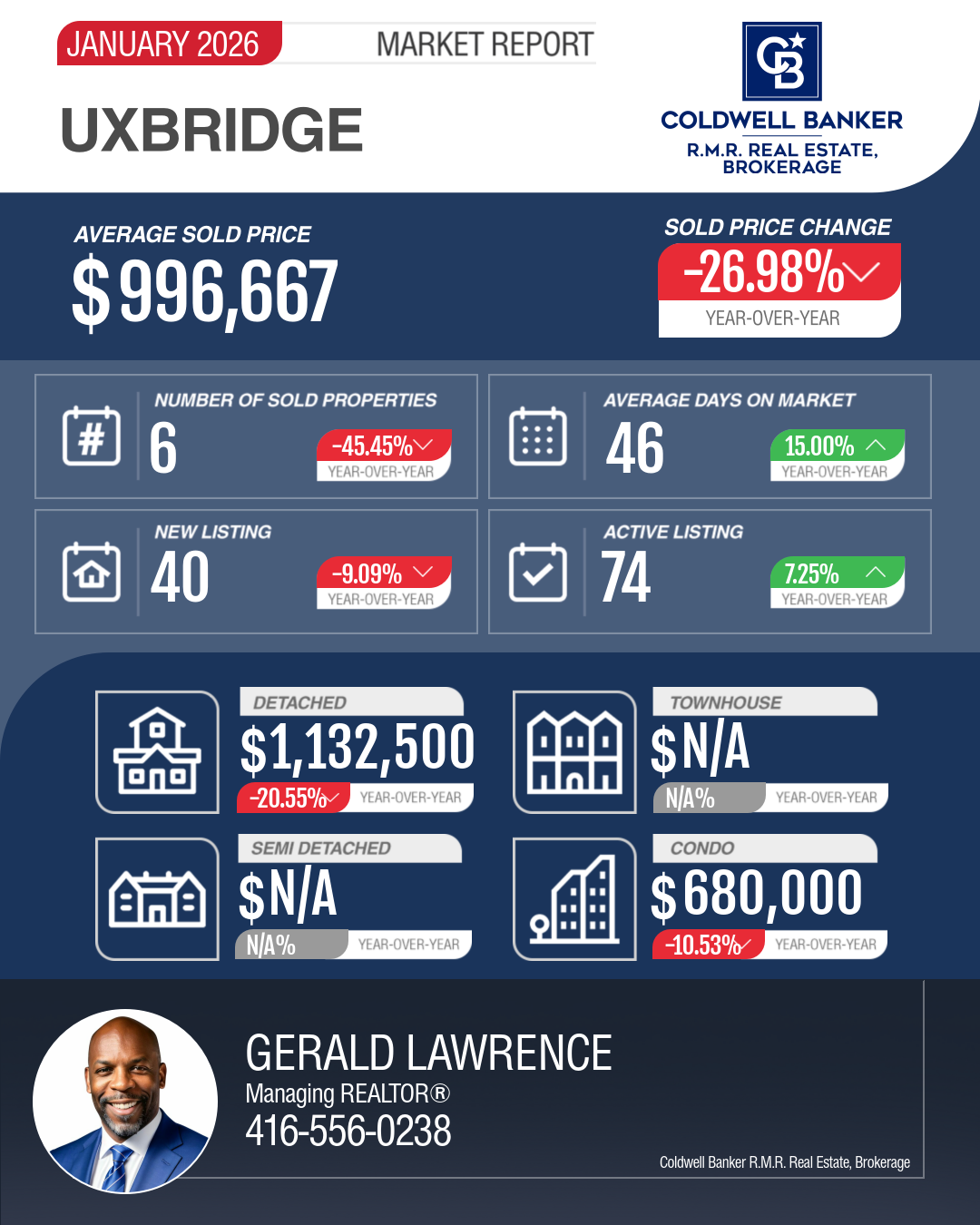

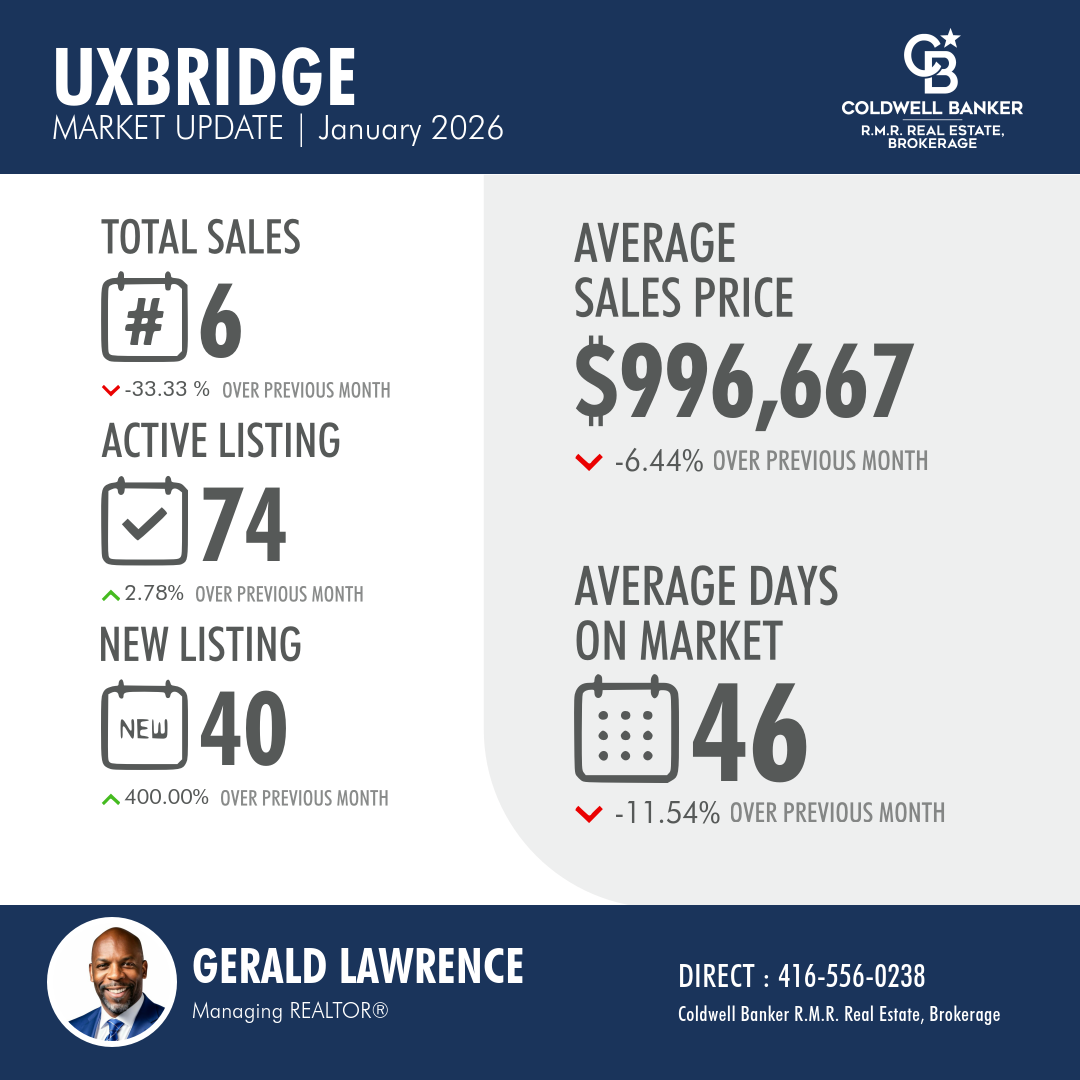

The Uxbridge housing market started 2026 in a cooling phase, characterized by significant year-over-year price corrections and a month-over-month decline. While the long-term trend (2020–2026) shows substantial growth, the current “Latest Reading” suggests a buyer-favorable shift as prices dip below the million-dollar threshold for the first time in several months.

1. Price Performance & Trends

Average Sale Price (Jan 2026):$996,667

Monthly Change: ▼ 1.9% (from Dec 2025)

Yearly Change: ▼ 27.0% (from Jan 2025)

Historical Context: January 2026 ranks 61st out of the last 73 months (bottom 17th percentile). Compared to the pandemic-era peak in February 2022 ($1,565,267), prices have retracted by approximately 36%.

Current Streaks: The market is currently experiencing a sustained cooling period, with 4 consecutive months of month-over-month price declines and 3 consecutive months of year-over-year declines.

2. Comparative Analysis (January YoY)

The current January average is significantly lower than the same month in previous years, highlighting a notable market reset:

vs. 2025: -27.0%

vs. 2024: -13.0%

vs. 2023: -20.5%

vs. 2022: -26.5%

vs. 2021: -24.7%

3. Market Highs and Lows

The Peak: The highest average price recorded in the dataset was $1,565,267 (Feb 2022), followed closely by November 2021 ($1,547,371).

The Floor: The lowest prices in recent years occurred in early 2020, with the bottom hit in March 2020 at $725,916.

Significant Moves: The most aggressive growth in the last 12 months occurred in September 2025, which saw a +32.4% year-over-year jump, a spike that has since been corrected.

4. Seasonal Insights

Data indicates a strong seasonal pattern in Uxbridge:

Highest Prices: Typically peak in May, coinciding with the spring market.

Lowest Prices: Historically found in December, following the late autumn slowdown.

5. Outlook for Buyers and Sellers

For Buyers:

The market currently presents a rare opportunity. With prices down 27% year-over-year and the average price sitting just under $1M, buyers have significantly more leverage than they did during the peak years of 2021–2022. The 4-month downward trend suggests a lack of urgency in the market, allowing for more thorough due diligence and negotiation.

Stop Waiting for the Bottom—You’re Looking at It. With Uxbridge prices dipping below $1,000,000 for the first time in years and year-over-year values down 27%, the “buyer’s market” window is wide open. Don’t wait for the spring rush to bring back the competition. Secure your dream home today while you still have the upper hand in negotiations. View Current Listings Under $1M

Buy the Dip, Not the Hype. Today’s Uxbridge market offers something we haven’t seen since 2020: Choice. With 4 consecutive months of price cooling, you can finally move at your own pace, perform your due diligence, and negotiate terms that work for you. Ready to find a high-value home in a premium community? [Download My Uxbridge Buyer’s Guide]

For Sellers:

The market is in a “down” cycle compared to the highs of late 2025. Sellers should be aware that Jan 2026 represents a low point in recent years (17th percentile). Pricing strategy is critical; properties priced based on 2022 or even early 2025 expectations will likely sit on the market. Strategic listing in the upcoming May peak may be advisable to capture the historical seasonal high.

Don’t Get Lost in the Spring Crowd. While the market is currently quiet, serious buyers are active and looking for quality inventory. By listing now, you capture “The Early Bird” demand before the market becomes saturated in May. Let’s position your home to stand out as the premier choice in Uxbridge. [Get My Professional Valuation]

Is Your Home Ready for the May Peak? History shows that Uxbridge prices consistently hit their highest levels in May. Success in this market requires more than a lawn sign—it requires a data-driven pricing strategy and flawless presentation. Start your 90-day “Success Plan” today to ensure you’re ready to capture top dollar when the market heats up. [Book a Strategy Consultation]

Living, Investing, and Thriving in Durham Region: A Complete Guide to What’s Happening Now

Durham Region continues to stand out as one of Ontario’s most desirable places to live, work, and invest. Located just east of Toronto, Durham offers a rare combination of affordability, community-focused living, economic growth, and access to nature—making it highly attractive to homebuyers, sellers, investors, and families alike.

As a REALTOR® serving Durham Region, staying informed on local events, infrastructure projects, lifestyle trends, and real estate market dynamics is essential. This comprehensive guide explores what’s happening across Durham right now, why it matters, and how it impacts real estate decisions—whether you’re buying your first home, upsizing, downsizing, or investing.

Why Durham Region Continues to Attract Buyers

Durham Region includes Ajax, Pickering, Whitby, Oshawa, Clarington, Scugog, Brock, and Uxbridge—each offering a distinct lifestyle while benefiting from regional growth and connectivity.

Key Reasons Buyers Are Choosing Durham:

Relative affordability compared to Toronto and York Region

GO Transit expansion and improved highway access

Growing employment hubs and post-secondary institutions

Waterfront communities and expansive green spaces

Strong sense of community and family-friendly neighbourhoods

For many buyers priced out of Toronto, Durham provides more space, better value, and long-term appreciation potential.

👉 Learn more about the region directly from Durham Region’s official website: https://www.durham.ca

Major Events and Community Happenings Across Durham Region

Community events play a major role in shaping neighbourhood appeal and quality of life—both important factors for homeowners and buyers.

The Durham housing market has evolved into a balanced, opportunity-driven environment.

Current Market Highlights:

Continued demand for detached and freehold townhomes

Strong interest in bungalows and downsizing options

Increased investor activity in legal duplexes and secondary suites

Buyers prioritizing move-in-ready homes and energy efficiency

Strategic pricing, professional marketing, and strong negotiation skills are more important than ever for sellers. Buyers, meanwhile, benefit from local expertise to identify value and avoid overpaying.

If you’re thinking about buying or selling, understanding micro-market conditions by neighbourhood is critical.

Lifestyle, Recreation, and Green Space

One of Durham’s strongest selling points is its access to nature.

Outdoor Highlights:

Lake Ontario waterfront trails and beaches

Heber Down Conservation Area

Lynde Shores Conservation Area

Durham Forest trail system

Durham’s balance of urban convenience and outdoor living continues to attract professionals, retirees, and families looking for a healthier lifestyle.

Real estate is hyper-local. Pricing, demand, and buyer behaviour can change street by street. As a REALTOR® actively working in Durham Region, I provide:

Neighbourhood-specific market insights

Accurate pricing strategies backed by data

Professional marketing and exposure

Skilled negotiation to protect your interests

Guidance through inspections, financing, and closing

Whether you’re buying your first home, selling a family property, or building an investment portfolio, local expertise translates into real results.

Strong Call to Action: Let’s Talk About Your Goals

If you’re considering buying, selling, or investing in Durham Region, now is the time to get informed and plan strategically.

✅ Request a free home value assessment ✅ Receive custom property alerts ✅ Discuss market timing and strategy ✅ Explore neighbourhoods that fit your lifestyle and budget

Durham Region is not just growing—it’s evolving. With strong infrastructure investment, vibrant communities, and diverse housing options, it remains one of the smartest real estate markets in the GTA.

Staying informed is the first step. Having the right REALTOR® is the second.

Destination Niagara: Unlocking Ontario’s Tourism Titan and the Future of Niagara Real Estate

The Niagara Region—a geographical marvel and a foundational piece of Canada’s history—is currently experiencing a monumental, multi-billion-dollar transformation. Driven by the Ontario government’s ambitious Destination Niagara Strategy, the region is being repositioned as a premier, world-class, four-season global tourism destination. This is not merely a plan for tourism; it is a profound economic and infrastructural overhaul designed to turbocharge growth, double the region’s tourism economic impact to over $6 billion annually, and attract an unprecedented 25 million annual visitors.

This detailed analysis explores the far-reaching scope of the strategy, delves into the mechanics of the five core investment pillars, and critically examines the profound ripple effects these developments are already having on the local communities and, most significantly, the regional property values.

I. The Blueprint for Global Recognition: Five Core Pillars

The Destination Niagara Strategy is built upon five interconnected pillars of investment, each carefully designed to move the region past its reliance on short-term, seasonal tourism and into a year-round economic engine that rivals global entertainment hubs.

1. New Tourism Attractions: Engineering Must-See Destinations

The strategy commits to creating spectacular, world-class attractions that compel visitors to extend their stays from 1-2 days to 3-4 days. This push for longer visitation is crucial for maximizing economic impact.

The Crown Jewel: Toronto Power Generating Station: The cornerstone of the plan is the private-sector-led, $300 million-plus revitalization of the historic Toronto Power Generating Station. This architectural marvel, perched above the Falls, is being converted into a five-star boutique hotel, blending heritage preservation with luxury tourism. The complex will feature a craft brewery, a museum, an art gallery, and a theatre, instantly establishing a new benchmark for high-end hospitality in the region.

Iconic Landmarks and Family Fun: Niagara Parks is actively pursuing procurement for major new infrastructure. This includes a world-class, year-round observation wheel—a true destination landmark—and the redevelopment of the Ontario Power Generating Station into a unique guest experience. Furthermore, the government is seeking information for a brand-new signature theme park attraction and the Niagara River Line attraction, a fully accessible, suspended electric tram system that promises unparalleled views of the Falls as it connects key attractions.

Niagara Parks Momentum: Success stories like the $25 million Niagara Takes Flight flying theatre experience, which welcomed over 120,000 visitors and generated nearly $3.5 million in its initial months, prove the appetite for these high-quality, immersive attractions.

2. Expanding World-Class Gaming: Building an Entertainment Hub

Niagara’s existing casino operations already attract over five million visitors and generate over $500 million in annual revenue. The strategy seeks to significantly enhance this sector. By exploring options to potentially expand the market to multiple new, world-class casinos, the province aims to attract major new private investment in top-tier dining, entertainment venues, and additional luxury hotel capacity. This elevation of the gaming and entertainment offer is crucial to competing with other North American entertainment hubs.

3. Growing Wine and Culinary Tourism: The Agri-Tourism Advantage

The Niagara Region is globally recognized for its VQA wine industry, responsible for 86% of Ontario’s grape production. The plan emphasizes agri-tourism, extending support for grape growers, producers, and winery retail experiences.

This pillar is designed to draw visitors beyond the tourist core into the wider region—including St. Catharines, Niagara-on-the-Lake, and the rural municipalities—to experience the unique terroir through farm-to-table dining, breweries, distilleries, and farmers’ markets. This diversification creates a sustainable, year-round tourism appeal that is less weather-dependent and highly attractive to international markets.

4. Investing in Arts and Culture: Preserving Local Identity

To encourage longer, richer visits, the strategy includes significant investments in cultural institutions. The rebuilding of the Shaw Festival’s historic Royal George Theatre with a $35 million investment, alongside over $1 million in funding for other local festivals and events, ensures the preservation and celebration of the region’s rich heritage. By funding projects that tell the under-told stories of Niagara, including Black and Indigenous history, the government is ensuring the cultural offering is diverse, authentic, and reflective of the region’s past.

None of the above can succeed without improved access. The strategy includes major commitments to infrastructure, leveraging the province’s multi-billion dollar capital plan to improve connectivity within the region and with the Greater Golden Horseshoe (GGH) and international markets.

Highway and Rail: Key projects include expanding the QEW in the Niagara corridor, twinning the Garden City Skyway, and continuing to increase GO Train service. The Niagara Region Transit Master Plan is already outlining stages for network optimization and Sunday service introduction by 2026-2027, with high-frequency networks in urban centres by 2031-2035.

Air Access: Issuing an RFP for development at the Niagara District Airport is a strategic move to unlock its potential to service millions of passengers and generate over $1 billion in economic output, creating a critical air gateway for international visitors.

II. The Property Value Perspective: Highs, Lows, and the Future of Housing

The sheer scale of the Destination Niagara Strategy guarantees a transformative effect on the region’s real estate market. This is a classic example of government and private investment acting as a catalyst for rapid value appreciation.

📈 The Positive Impact: Unprecedented Value Appreciation

The overall outlook for property values in the Niagara Region is decidedly positive, driven by fundamental economic factors:

Premium for Connectivity: The most significant booster outside of the tourist core is the increased GO Train service and highway upgrades. The elimination of the provincial portion of the HST for first-time home buyers on new homes up to $1 million (subject to federal legislation) makes a move to Niagara even more appealing. For many GGH workers, Niagara offers a transit-connected, highly desirable, and relatively affordable alternative to Toronto or Hamilton. This influx of commuter buyers dramatically increases demand for housing near transit hubs in St. Catharines, Grimsby, and Niagara Falls.

Luxury and Economic Diversification: The new five-star hotel, world-class attractions, and expanded dining/gaming venues will generate an array of high-wage, specialized jobs in luxury management, finance, and technology. This influx of “young wealth creators” and highly skilled professionals will boost demand for upscale housing, driving up average sale prices, especially in Niagara Falls and Niagara-on-the-Lake.

Investor Confidence and Rental Returns: The guaranteed increase to 25 million annual visitors creates a gold rush for investors. Properties suitable for short-term vacation rentals (VRUs) will see their income potential soar, making them exceptionally valuable assets. Meanwhile, long-term rentals will see high demand from the growing permanent workforce, ensuring low vacancy rates and strong rental yields. This dual-market pressure pushes up the price ceiling for all homes.

Infrastructure-Led Growth: Areas benefiting from the Niagara Region Transit Master Plan, such as new microtransit hubs and high-frequency routes in Fort Erie, Welland, and Grimsby, will see property values rise as accessibility and quality of life improve.

📉 The Critical Challenge: The Affordability Divide

While asset appreciation is a boon for existing homeowners, the strategy poses serious challenges to social equity and the availability of local labour.

Workforce Displacement: The very success of the $6 billion tourism economy depends on thousands of service industry workers—chefs, hotel staff, attraction operators, and cleaners. These workers typically rely on entry-level and mid-range housing. The dramatic increase in housing costs, driven by high-income commuters and VRU investors, creates a severe affordability crisis. Without proactive measures, essential workers will be priced out of the communities they serve, forcing them into long commutes and straining local infrastructure.

Residential Inventory Strain: The conversion of traditional long-term rentals and residential homes into profitable vacation rental units further depletes housing stock, exacerbating the problem. Municipalities like Niagara Falls are already grappling with how to regulate vacation rental units (VRUs) and single-room occupancy in existing motels to strike a balance. If the supply-demand imbalance is not addressed through targeted housing strategies, including the development of workforce housing and greater residential density, the housing crisis could ironically become the biggest threat to the region’s economic growth targets.

III. A Sustainable Future: Balancing Prosperity and Preservation

The long-term success of Destination Niagara hinges on the province and regional partners managing the trade-offs between economic expansion and community integrity.

Environmental Stewardship: The history of tourism at Niagara Falls, dating back to the 1800s, has always been a battle between preservation and commercialism. Modern influences, including hydroelectric diversion and remedial work, have long been necessary to preserve the Falls. The current strategy commits to balancing growth with preservation, promising to integrate green spaces and eco-friendly initiatives. However, with massive developments like the new theme park and a suspended tram, stringent environmental impact studies and adherence to the Niagara Official Plan are essential to ensure the natural heritage—from the Niagara Glen Nature Reserve to the Escarpment—remains pristine.

Cultural and Social Resilience: The influx of new visitors and the shift towards a high-end, globalized entertainment economy must not come at the expense of local character. Investments in arts and culture are key, but there must be continued commitment to “Creative Niagara”—a recognition that the region’s unique mix of historic towns (Niagara-on-the-Lake), industrial centres (St. Catharines), and rural landscapes must be protected and celebrated. The goal is to ensure that Niagara remains both a great place to visit and a great place to live.

The Destination Niagara Strategy is a powerful, long-term investment in Ontario’s economic future. By leveraging its iconic natural asset and pairing it with smart infrastructure, luxury attractions, and a diversified cultural offering, the province is poised to make Niagara a year-round tourism powerhouse. For homeowners, it means strong appreciation; for prospective buyers and investors, it signals an unmissable long-term opportunity, provided the region successfully navigates the complex challenge of housing affordability.

🏘️ In-Depth Look: Housing Strategies and Zoning Battles in the Niagara Region

Will the region’s prosperity destroy its affordability?

The economic boom and property value appreciation are a double-edged sword, and local municipalities are keenly aware of the brewing crisis.

The research confirms that the Niagara Region and its key cities, such as Niagara Falls and St. Catharines, are actively responding to the housing pressures through comprehensive planning, affordable housing investments, and regulatory changes. Their actions fall into two main categories: increasing the affordable and attainable housing supply and regulating short-term rentals (VRUs) to protect long-term housing stock.

1. Attainable and Affordable Housing Initiatives

The Niagara Region, recognizing that its housing costs are rising faster than incomes (the median rent for a 1-bed unit jumped 19.2% from 2021), has deployed a multi-faceted approach to address the housing spectrum, from homelessness to medium-income household needs.

Niagara Region-Wide Strategies: The Long-Term Roadmap

Consolidated Housing Master Plan (2025 Update): This is the Region’s 25-year roadmap to address the severe need for housing, particularly for low- and moderate-income households. The plan aims to double the current number of community housing units by 2050, committing to building 2,983 new units.

Funding Commitment: The Region is proposing to fund 25% of the expected costs (approximately $546 million) and is actively pursuing co-investment from federal and provincial governments, including leveraging programs like the Canada-Ontario Affordable Housing Fund (AHF) and the Ontario Priorities Housing Initiative (OPHI).

Focus on Existing Assets: A key part of the plan is redeveloping existing Niagara Regional Housing properties to add density on current sites, streamlining delivery, and reducing land acquisition costs.

Attainable Housing Strategy: This strategy specifically targets households with incomes (80-120% of the average) who struggle to afford market-rate housing but do not qualify for rent-geared-to-income (RGI) support. The goals include:

Increasing the supply of rental housing through strategic incentives for purpose-built rentals.

Optimizing the use of existing housing stock and promoting innovative models like modular construction.

Targeted Affordable Housing: Federal and provincial funding, through programs like OPHI, has been funnelled into projects in Niagara Falls and across the Region to create permanent supportive housing and temporary bridge housing for vulnerable populations.

St. Catharines: Intensification and Zoning Reforms

St. Catharines is leveraging its status as a key urban growth area and transit hub to drive density. The city’s current planning reviews and by-law amendments are focused on increasing the housing supply through policy changes:

Zoning By-Law Housekeeping Amendment (April 2024): This significant amendment promotes intensification in established neighbourhoods:

Accessory Dwelling Units (ADUs): It explicitly permits two additional residential units (ADUs) within detached, semi-detached, or townhouse dwellings, including updated standards for detached ADUs (laneway suites).

Missing Middle Housing: It permits duplex, triplex, and fourplex dwellings within the former Low Density – Suburban Neighbourhood (R1) Zone. This move directly responds to the provincial mandate to allow the “missing middle” housing forms and will be crucial for creating more affordable entry points for new buyers and renters.