Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Market Update •

December 16, 2025

Niagara’s $6 Billion Secret: How Ford’s Massive Plan Will Triple Your Property Value (The GO Train Effect is Real)

Destination Niagara: Unlocking Ontario’s Tourism Titan and the Future of Niagara Real Estate

The Niagara Region—a geographical marvel and a foundational piece of Canada’s history—is currently experiencing a monumental, multi-billion-dollar transformation. Driven by the Ontario government’s ambitious Destination Niagara Strategy, the region is being repositioned as a premier, world-class, four-season global tourism destination. This is not merely a plan for tourism; it is a profound economic and infrastructural overhaul designed to turbocharge growth, double the region’s tourism economic impact to over $6 billion annually, and attract an unprecedented 25 million annual visitors.

This detailed analysis explores the far-reaching scope of the strategy, delves into the mechanics of the five core investment pillars, and critically examines the profound ripple effects these developments are already having on the local communities and, most significantly, the regional property values.

Ready to invest in the Niagara boom? Search Listings Now! Find out what your current Home is Worth with a free valuation, and Download Our Investor’s Guide for exclusive strategy insights. Explore New Neighbourhood Listings as they hit the market, Schedule a Private Tour Today, and Sign Up for Price Drop Alerts to never miss a deal. Want local expertise? Message Us to Connect You with An Agent instantly or Call Us Now to discuss your goals. Build Your Dream Home Wishlist with us, and finally, See What’s Available at http://www.MultipleListings.ca.

I. The Blueprint for Global Recognition: Five Core Pillars

The Destination Niagara Strategy is built upon five interconnected pillars of investment, each carefully designed to move the region past its reliance on short-term, seasonal tourism and into a year-round economic engine that rivals global entertainment hubs.

1. New Tourism Attractions: Engineering Must-See Destinations

The strategy commits to creating spectacular, world-class attractions that compel visitors to extend their stays from 1-2 days to 3-4 days. This push for longer visitation is crucial for maximizing economic impact.

-

The Crown Jewel: Toronto Power Generating Station: The cornerstone of the plan is the private-sector-led, $300 million-plus revitalization of the historic Toronto Power Generating Station. This architectural marvel, perched above the Falls, is being converted into a five-star boutique hotel, blending heritage preservation with luxury tourism. The complex will feature a craft brewery, a museum, an art gallery, and a theatre, instantly establishing a new benchmark for high-end hospitality in the region.

-

Iconic Landmarks and Family Fun: Niagara Parks is actively pursuing procurement for major new infrastructure. This includes a world-class, year-round observation wheel—a true destination landmark—and the redevelopment of the Ontario Power Generating Station into a unique guest experience. Furthermore, the government is seeking information for a brand-new signature theme park attraction and the Niagara River Line attraction, a fully accessible, suspended electric tram system that promises unparalleled views of the Falls as it connects key attractions.

-

Niagara Parks Momentum: Success stories like the $25 million Niagara Takes Flight flying theatre experience, which welcomed over 120,000 visitors and generated nearly $3.5 million in its initial months, prove the appetite for these high-quality, immersive attractions.

Ready to invest in the Niagara boom? Search Listings Now! Find out what your current Home is Worth with a free valuation, and Download Our Investor’s Guide for exclusive strategy insights. Explore New Neighbourhood Listings as they hit the market, Schedule a Private Tour Today, and Sign Up for Price Drop Alerts to never miss a deal. Want local expertise? Message Us to Connect You with An Agent instantly or Call Us Now to discuss your goals. Build Your Dream Home Wishlist with us, and finally, See What’s Available at http://www.MultipleListings.ca.

2. Expanding World-Class Gaming: Building an Entertainment Hub

Niagara’s existing casino operations already attract over five million visitors and generate over $500 million in annual revenue. The strategy seeks to significantly enhance this sector. By exploring options to potentially expand the market to multiple new, world-class casinos, the province aims to attract major new private investment in top-tier dining, entertainment venues, and additional luxury hotel capacity. This elevation of the gaming and entertainment offer is crucial to competing with other North American entertainment hubs.

3. Growing Wine and Culinary Tourism: The Agri-Tourism Advantage

The Niagara Region is globally recognized for its VQA wine industry, responsible for 86% of Ontario’s grape production. The plan emphasizes agri-tourism, extending support for grape growers, producers, and winery retail experiences.

This pillar is designed to draw visitors beyond the tourist core into the wider region—including St. Catharines, Niagara-on-the-Lake, and the rural municipalities—to experience the unique terroir through farm-to-table dining, breweries, distilleries, and farmers’ markets. This diversification creates a sustainable, year-round tourism appeal that is less weather-dependent and highly attractive to international markets.

4. Investing in Arts and Culture: Preserving Local Identity

To encourage longer, richer visits, the strategy includes significant investments in cultural institutions. The rebuilding of the Shaw Festival’s historic Royal George Theatre with a $35 million investment, alongside over $1 million in funding for other local festivals and events, ensures the preservation and celebration of the region’s rich heritage. By funding projects that tell the under-told stories of Niagara, including Black and Indigenous history, the government is ensuring the cultural offering is diverse, authentic, and reflective of the region’s past.

5. Transportation Development: Seamless Connectivity

None of the above can succeed without improved access. The strategy includes major commitments to infrastructure, leveraging the province’s multi-billion dollar capital plan to improve connectivity within the region and with the Greater Golden Horseshoe (GGH) and international markets.

-

Highway and Rail: Key projects include expanding the QEW in the Niagara corridor, twinning the Garden City Skyway, and continuing to increase GO Train service. The Niagara Region Transit Master Plan is already outlining stages for network optimization and Sunday service introduction by 2026-2027, with high-frequency networks in urban centres by 2031-2035.

-

Air Access: Issuing an RFP for development at the Niagara District Airport is a strategic move to unlock its potential to service millions of passengers and generate over $1 billion in economic output, creating a critical air gateway for international visitors.

Ready to invest in the Niagara boom? Search Listings Now! Find out what your current Home is Worth with a free valuation, and Download Our Investor’s Guide for exclusive strategy insights. Explore New Neighbourhood Listings as they hit the market, Schedule a Private Tour Today, and Sign Up for Price Drop Alerts to never miss a deal. Want local expertise? Message Us to Connect You with An Agent instantly or Call Us Now to discuss your goals. Build Your Dream Home Wishlist with us, and finally, See What’s Available at http://www.MultipleListings.ca.

II. The Property Value Perspective: Highs, Lows, and the Future of Housing

The sheer scale of the Destination Niagara Strategy guarantees a transformative effect on the region’s real estate market. This is a classic example of government and private investment acting as a catalyst for rapid value appreciation.

📈 The Positive Impact: Unprecedented Value Appreciation

The overall outlook for property values in the Niagara Region is decidedly positive, driven by fundamental economic factors:

-

Premium for Connectivity: The most significant booster outside of the tourist core is the increased GO Train service and highway upgrades. The elimination of the provincial portion of the HST for first-time home buyers on new homes up to $1 million (subject to federal legislation) makes a move to Niagara even more appealing. For many GGH workers, Niagara offers a transit-connected, highly desirable, and relatively affordable alternative to Toronto or Hamilton. This influx of commuter buyers dramatically increases demand for housing near transit hubs in St. Catharines, Grimsby, and Niagara Falls.

-

Luxury and Economic Diversification: The new five-star hotel, world-class attractions, and expanded dining/gaming venues will generate an array of high-wage, specialized jobs in luxury management, finance, and technology. This influx of “young wealth creators” and highly skilled professionals will boost demand for upscale housing, driving up average sale prices, especially in Niagara Falls and Niagara-on-the-Lake.

-

Investor Confidence and Rental Returns: The guaranteed increase to 25 million annual visitors creates a gold rush for investors. Properties suitable for short-term vacation rentals (VRUs) will see their income potential soar, making them exceptionally valuable assets. Meanwhile, long-term rentals will see high demand from the growing permanent workforce, ensuring low vacancy rates and strong rental yields. This dual-market pressure pushes up the price ceiling for all homes.

-

Infrastructure-Led Growth: Areas benefiting from the Niagara Region Transit Master Plan, such as new microtransit hubs and high-frequency routes in Fort Erie, Welland, and Grimsby, will see property values rise as accessibility and quality of life improve.

Ready to invest in the Niagara boom? Search Listings Now! Find out what your current Home is Worth with a free valuation, and Download Our Investor’s Guide for exclusive strategy insights. Explore New Neighbourhood Listings as they hit the market, Schedule a Private Tour Today, and Sign Up for Price Drop Alerts to never miss a deal. Want local expertise? Message Us to Connect You with An Agent instantly or Call Us Now to discuss your goals. Build Your Dream Home Wishlist with us, and finally, See What’s Available at http://www.MultipleListings.ca.

📉 The Critical Challenge: The Affordability Divide

While asset appreciation is a boon for existing homeowners, the strategy poses serious challenges to social equity and the availability of local labour.

-

Workforce Displacement: The very success of the $6 billion tourism economy depends on thousands of service industry workers—chefs, hotel staff, attraction operators, and cleaners. These workers typically rely on entry-level and mid-range housing. The dramatic increase in housing costs, driven by high-income commuters and VRU investors, creates a severe affordability crisis. Without proactive measures, essential workers will be priced out of the communities they serve, forcing them into long commutes and straining local infrastructure.

-

Residential Inventory Strain: The conversion of traditional long-term rentals and residential homes into profitable vacation rental units further depletes housing stock, exacerbating the problem. Municipalities like Niagara Falls are already grappling with how to regulate vacation rental units (VRUs) and single-room occupancy in existing motels to strike a balance. If the supply-demand imbalance is not addressed through targeted housing strategies, including the development of workforce housing and greater residential density, the housing crisis could ironically become the biggest threat to the region’s economic growth targets.

Ready to invest in the Niagara boom? Search Listings Now! Find out what your current Home is Worth with a free valuation, and Download Our Investor’s Guide for exclusive strategy insights. Explore New Neighbourhood Listings as they hit the market, Schedule a Private Tour Today, and Sign Up for Price Drop Alerts to never miss a deal. Want local expertise? Message Us to Connect You with An Agent instantly or Call Us Now to discuss your goals. Build Your Dream Home Wishlist with us, and finally, See What’s Available at http://www.MultipleListings.ca.

III. A Sustainable Future: Balancing Prosperity and Preservation

The long-term success of Destination Niagara hinges on the province and regional partners managing the trade-offs between economic expansion and community integrity.

-

Environmental Stewardship: The history of tourism at Niagara Falls, dating back to the 1800s, has always been a battle between preservation and commercialism. Modern influences, including hydroelectric diversion and remedial work, have long been necessary to preserve the Falls. The current strategy commits to balancing growth with preservation, promising to integrate green spaces and eco-friendly initiatives. However, with massive developments like the new theme park and a suspended tram, stringent environmental impact studies and adherence to the Niagara Official Plan are essential to ensure the natural heritage—from the Niagara Glen Nature Reserve to the Escarpment—remains pristine.

-

Cultural and Social Resilience: The influx of new visitors and the shift towards a high-end, globalized entertainment economy must not come at the expense of local character. Investments in arts and culture are key, but there must be continued commitment to “Creative Niagara”—a recognition that the region’s unique mix of historic towns (Niagara-on-the-Lake), industrial centres (St. Catharines), and rural landscapes must be protected and celebrated. The goal is to ensure that Niagara remains both a great place to visit and a great place to live.

The Destination Niagara Strategy is a powerful, long-term investment in Ontario’s economic future. By leveraging its iconic natural asset and pairing it with smart infrastructure, luxury attractions, and a diversified cultural offering, the province is poised to make Niagara a year-round tourism powerhouse. For homeowners, it means strong appreciation; for prospective buyers and investors, it signals an unmissable long-term opportunity, provided the region successfully navigates the complex challenge of housing affordability.

Ready to invest in the Niagara boom? Search Listings Now! Find out what your current Home is Worth with a free valuation, and Download Our Investor’s Guide for exclusive strategy insights. Explore New Neighbourhood Listings as they hit the market, Schedule a Private Tour Today, and Sign Up for Price Drop Alerts to never miss a deal. Want local expertise? Message Us to Connect You with An Agent instantly or Call Us Now to discuss your goals. Build Your Dream Home Wishlist with us, and finally, See What’s Available at http://www.MultipleListings.ca.

🏘️ In-Depth Look: Housing Strategies and Zoning Battles in the Niagara Region

Will the region’s prosperity destroy its affordability?

The economic boom and property value appreciation are a double-edged sword, and local municipalities are keenly aware of the brewing crisis.

The research confirms that the Niagara Region and its key cities, such as Niagara Falls and St. Catharines, are actively responding to the housing pressures through comprehensive planning, affordable housing investments, and regulatory changes. Their actions fall into two main categories: increasing the affordable and attainable housing supply and regulating short-term rentals (VRUs) to protect long-term housing stock.

1. Attainable and Affordable Housing Initiatives

The Niagara Region, recognizing that its housing costs are rising faster than incomes (the median rent for a 1-bed unit jumped 19.2% from 2021), has deployed a multi-faceted approach to address the housing spectrum, from homelessness to medium-income household needs.

Niagara Region-Wide Strategies: The Long-Term Roadmap

-

Consolidated Housing Master Plan (2025 Update): This is the Region’s 25-year roadmap to address the severe need for housing, particularly for low- and moderate-income households. The plan aims to double the current number of community housing units by 2050, committing to building 2,983 new units.

-

Funding Commitment: The Region is proposing to fund 25% of the expected costs (approximately $546 million) and is actively pursuing co-investment from federal and provincial governments, including leveraging programs like the Canada-Ontario Affordable Housing Fund (AHF) and the Ontario Priorities Housing Initiative (OPHI).

-

Focus on Existing Assets: A key part of the plan is redeveloping existing Niagara Regional Housing properties to add density on current sites, streamlining delivery, and reducing land acquisition costs.

-

-

Attainable Housing Strategy: This strategy specifically targets households with incomes (80-120% of the average) who struggle to afford market-rate housing but do not qualify for rent-geared-to-income (RGI) support. The goals include:

-

Increasing the supply of rental housing through strategic incentives for purpose-built rentals.

-

Optimizing the use of existing housing stock and promoting innovative models like modular construction.

-

-

Targeted Affordable Housing: Federal and provincial funding, through programs like OPHI, has been funnelled into projects in Niagara Falls and across the Region to create permanent supportive housing and temporary bridge housing for vulnerable populations.

Ready to invest in the Niagara boom? Search Listings Now! Find out what your current Home is Worth with a free valuation, and Download Our Investor’s Guide for exclusive strategy insights. Explore New Neighbourhood Listings as they hit the market, Schedule a Private Tour Today, and Sign Up for Price Drop Alerts to never miss a deal. Want local expertise? Message Us to Connect You with An Agent instantly or Call Us Now to discuss your goals. Build Your Dream Home Wishlist with us, and finally, See What’s Available at http://www.MultipleListings.ca.

St. Catharines: Intensification and Zoning Reforms

St. Catharines is leveraging its status as a key urban growth area and transit hub to drive density. The city’s current planning reviews and by-law amendments are focused on increasing the housing supply through policy changes:

-

Zoning By-Law Housekeeping Amendment (April 2024): This significant amendment promotes intensification in established neighbourhoods:

-

Accessory Dwelling Units (ADUs): It explicitly permits two additional residential units (ADUs) within detached, semi-detached, or townhouse dwellings, including updated standards for detached ADUs (laneway suites).

-

Missing Middle Housing: It permits duplex, triplex, and fourplex dwellings within the former Low Density – Suburban Neighbourhood (R1) Zone. This move directly responds to the provincial mandate to allow the “missing middle” housing forms and will be crucial for creating more affordable entry points for new buyers and renters.

-

-

The Garden City Plan (Official Plan Update): St. Catharines is consolidating its official plan to accommodate a 2051 growth horizon, planning for 18,000 new housing units and 35,000 new residents. The focus is on aligning land use, transportation, and infrastructure to direct growth toward the downtown urban growth area and major transit hubs (like the new GO Station), supporting a compact, efficient built form.

2. The VRU Crackdown: Protecting Residential Housing Stock

The financial incentive to convert residential homes into lucrative short-term rentals (VRUs) is a direct consequence of the Destination Niagara Strategy’s success. Both Niagara Falls and St. Catharines have implemented strict regulatory frameworks to curb this trend and protect long-term housing availability.

| Municipality | Regulation Strategy | Key Rules and Fines |

| Niagara Falls | Restrictive Zoning & High Fines | VRUs (Non-owner-occupied) are only permitted in specific commercial/tourist zones (TC, GC, CB). They are illegal in most residential areas. |

| Fines: Up to $50,000 for a first offence and up to $100,000 for subsequent offences for operating without a license or in an unpermitted zone. | ||

| Licensing: Mandatory VRU license ($500 initial, $250 annual renewal), $2/night Municipal Accommodation Tax (MAT). | ||

| St. Catharines | Principal Residence Rule | STRs are generally only permitted when the property remains the host’s primary residence and the operation is an occasional, secondary use (home-based business). |

| Tax: Collects a 2% Municipal Accommodation Tax (MAT) on short-term stays. | ||

| Enforcement: Currently strengthening its by-law enforcement capabilities to regulate public space use and non-compliant operations. |

The intent is clear: to legally fence off residential neighbourhoods from the powerful commercial pressures of the $6 billion tourism market. This regulation is crucial for investors—a non-owner-occupied property purchased in a Niagara Falls residential zone cannot be legally operated as a VRU without facing severe fines, forcing these homes back into the long-term rental or owner-occupied housing pool.

Ready to invest in the Niagara boom? Search Listings Now! Find out what your current Home is Worth with a free valuation, and Download Our Investor’s Guide for exclusive strategy insights. Explore New Neighbourhood Listings as they hit the market, Schedule a Private Tour Today, and Sign Up for Price Drop Alerts to never miss a deal. Want local expertise? Message Us to Connect You with An Agent instantly or Call Us Now to discuss your goals. Build Your Dream Home Wishlist with us, and finally, See What’s Available at http://www.MultipleListings.ca.

🎯 Conclusion on Housing and Property Values

The Destination Niagara Strategy is fundamentally an economic growth policy that drives up property values across the board. The local planning and housing initiatives act as a mitigation strategy to manage the social consequences of that growth.

-

Property Value Prediction: Areas benefiting from the Destination Niagara investments and GO Train connectivity (Niagara Falls tourism zones, St. Catharines downtown) will see the highest appreciation.

-

Mitigation Success: The success of the zoning changes in St. Catharines (allowing duplexes/fourplexes) and the VRU crackdown in Niagara Falls will be the key to maintaining a functional workforce. If these policies successfully create a greater supply of “missing middle” housing and prevent mass residential displacement, the region can retain the workers necessary to sustain its tourism boom.

The next few years will be a race between the speed of the tourism/economic development and the pace of the housing supply and affordability solutions.

Ready to invest in the Niagara boom? Search Listings Now! Find out what your current Home is Worth with a free valuation, and Download Our Investor’s Guide for exclusive strategy insights. Explore New Neighbourhood Listings as they hit the market, Schedule a Private Tour Today, and Sign Up for Price Drop Alerts to never miss a deal. Want local expertise? Message Us to Connect You with An Agent instantly or Call Us Now to discuss your goals. Build Your Dream Home Wishlist with us, and finally, See What’s Available at http://www.MultipleListings.ca.

The real estate market inside scoop for the community you love. See homes that are for sale and have recently sold. Find out if home sales in your neighbourhood are trending up or down. See what homes around you are currently selling for.

Market Update •

November 30, 2025

Thank You For The Booked Showing – 19 Forestgreen Drive!

Thanks for Booking A Showing for 19 Forestgreen Dr by Gerald Lawrence, REALTOR®

Industry Update •

November 26, 2025

“Pay to Say”: The Controversial New Rule Blocking Tenants From Court (Unless They Pay Up)

Bill 60 Deep Dive: The Ultimate Guide for Ontario Landlords, Tenants, Buyers, and Sellers

Bill 60, formally known as the Fighting Delays, Building Faster Act, 2025, has officially shaken up the landscape of rental housing in Ontario. Whether you are a seasoned investor, a first-time renter, or someone looking to buy or sell a tenanted property, these changes are not just “fine print”—they fundamentally alter your rights, timelines, and financial obligations.

This comprehensive guide breaks down every critical aspect of the new legislation, offering detailed analysis, practical scenarios, and checklists to keep you compliant and protected.

What is Bill 60?

At its core, Bill 60 was introduced by the Ontario government with the stated aim of “reducing red tape” and clearing the massive backlog at the Landlord and Tenant Board (LTB). For years, both landlords and tenants have suffered from wait times that can stretch to 8-12 months for a simple hearing.

While the goal of speed is universally appreciated, the methods used in Bill 60 have sparked intense debate. The legislation aggressively shortens timelines for evictions and limits certain tenant defenses, tilting the procedural balance significantly.

The 4 Key Changes You Must Know

1. The “Cash for Keys” Trade-Off (N12 Compensation)

-

Old Rule: If a landlord wanted to move into their unit (or move a family member in), they had to give 60 days’ notice and pay the tenant 1 month’s rent as compensation.

-

New Bill 60 Rule: Landlords can now avoid paying the 1-month compensation if they provide a longer notice period of 120 days (4 months) instead of the standard 60 days.

-

Note: This specifically applies to Section 48 (Landlord’s Own Use).

-

Strategy: This creates a “Time vs. Money” decision for landlords. If you are cash-poor but have time, you can save money. If you need the unit fast, you pay the compensation for the 60-day exit.

-

2. “Pay to Say” (Rent Arrears Hearings)

-

Old Rule: If a landlord filed for eviction due to unpaid rent (L1 application), the tenant could show up at the hearing and raise “new issues” like maintenance problems or harassment to explain why they withheld rent.

-

New Bill 60 Rule: Tenants can no longer raise these issues at an arrears hearing unless they:

-

Provide advance written notice.

-

Pay 50% of the alleged rent arrears into the Board or to the landlord before the hearing can proceed with those arguments.

-

Impact: This effectively bars tenants who are withholding rent due to severe disrepair (and have spent the money on repairs or other needs) from using that defense without a significant upfront payment.

-

3. The 7-Day Eviction Clock (N4 Notice)

-

Old Rule: If a tenant missed rent, the landlord gave an N4 notice. The landlord had to wait 14 days after the notice was served before they could file an application with the LTB.

-

New Bill 60 Rule: The waiting period has been slashed to 7 days.

-

Impact: This cuts a week off the eviction timeline. If rent is due on the 1st and unpaid, an N4 can be issued on the 2nd, and the LTB filing can happen as early as the 9th or 10th.

-

4. Slashed Appeal Windows

-

Old Rule: Parties had 30 days to appeal an LTB decision to the Divisional Court or request a review.

-

New Bill 60 Rule: The appeal window is reduced to 15 days.

-

Impact: You must have your legal counsel and paperwork ready immediately after a decision is rendered.

-

Pros and Cons Analysis

For Landlords

For Tenants

Real-World Scenarios

Scenario A: The “Patient” Landlord

Situation: Sarah owns a condo downtown. Her daughter is graduating university in 5 months and needs the unit.

Action: Sarah serves an N12 notice now, opting for the 120-day termination date.

Result: Sarah does not have to pay her tenant the standard $2,800 compensation. The tenant gets 4 months to find a place, and Sarah saves nearly $3,000.

Scenario B: The “Emergency” Repair Defense

Situation: Mark, a tenant, stops paying rent because his roof is leaking and destroying his furniture. He owes $4,000 in back rent.

Bill 60 Impact: The landlord files for eviction. Mark wants to show photos of the roof at the hearing. The adjudicator asks, “Have you paid $2,000 (50%) of the arrears?” Mark has not.

Result: Mark is blocked from raising the maintenance issue as a defense against the eviction. The eviction for non-payment is likely granted, and Mark must pursue a separate (and later) application for the roof.

Critical Advice for Buyers and Sellers of Tenanted Properties

This is the most complex area of the new bill. The distinction between Landlord’s Own Use (Section 48) and Purchaser’s Own Use (Section 49) is vital.

For Sellers

-

The “Compensation Trap”: If you are selling a tenanted property, do not assume you can waive the compensation for the buyer. The legislation specifically amends Section 48 (Landlord’s Own Use). It is legally risky to assume this applies to Section 49 (Purchaser’s Own Use).

-

Recommendation: If your buyer wants vacant possession, stick to the standard 60-day N12 and pay the compensation. Using the 120-day rule to save a few thousand dollars could spook a buyer who doesn’t want to wait 4 months to close.

-

Marketing: If you have a long closing (e.g., 5-6 months), you might be able to use the 120-day notice before listing or early in the process to clear the unit cost-effectively, but consult a paralegal first.

For Buyers

-

Closing Dates: If you are buying a tenanted property for your own use, demand a standard 60-day N12. Do not let the seller try to save money with the 120-day notice unless you are perfectly happy waiting 4+ months to move in.

-

Vacant Possession Clauses: Ensure your Agreement of Purchase and Sale (APS) has a strict clause requiring the Seller to provide vacant possession. With the new appeal window shortened to 15 days, you will know sooner if a tenant is fighting the eviction, allowing you to walk away or renegotiate faster.

Actionable To-Do Lists

For Landlords

-

[ ] Update Your Forms: Ensure you are using the newest versions of N4 and N12 forms that reflect Bill 60 changes. Old forms may be considered defective.

-

[ ] Audit Your Arrears: If a tenant is late, issue the N4 on day 2. Mark your calendar for Day 8 to file the L1 application (down from Day 15).

-

[ ] Budget for Legal: If you plan to use the 120-day notice, verify with a legal professional that your specific scenario qualifies for the compensation waiver.

For Tenants

-

[ ] Don’t Withhold Rent: Under Bill 60, withholding rent is riskier than ever. Pay your rent, and file a separate T6 (Maintenance) application immediately if repairs are needed.

-

[ ] Act Fast on N4s: If you receive a 7-day notice, contact a rent bank or legal clinic immediately. You have half the time you used to have.

-

[ ] Check the Notice: If a landlord gives you 120 days notice and doesn’t pay compensation, make sure they are actually moving in. If they re-rent it or sell it, you can file a T5 (Bad Faith) application for significant damages.

Conclusion

Bill 60 is a double-edged sword. It offers speed and cost-saving potential for landlords but demands rigorous adherence to new, tighter schedules. For tenants, it strips away financial leverage and safety nets, making “paying rent on time” the only safe harbor. Whether you agree with the politics or not, understanding these rules is the only way to survive in Ontario’s new rental reality.

Bill 60 protest video This video provides visual context on the public reaction and protests regarding Bill 60, highlighting the intensity of the debate surrounding these changes.

🚨 Critical Action: Are Your New Notices Legal?

Bill 60 has eliminated your margin for error. The new 7-day N4 timelines and the complex N12 compensation waivers mean a single mistake on paperwork can lead to your LTB application being dismissed—forcing you to start over, or worse, facing substantial bad-faith fines.

Don’t rely on outdated templates or guesswork. Ensure your documentation is 100% compliant with the new Fighting Delays, Building Faster Act before you file.

Protect Your Investment: Book a Bill 60 Compliance Audit

Click below to schedule a rapid, 15-minute audit with a licensed paralegal specializing in Ontario landlord-tenant law.

We will confirm if:

-

Your 7-day N4 is properly timed and served.

-

Your 120-day N12 compensation waiver is legally applicable to your scenario (Section 48 vs. Section 49).

-

Your selling strategy complies with the new purchaser use rules.

Protect your legal right to the unit and save thousands in potential compensation and fines.

Market Update •

November 20, 2025

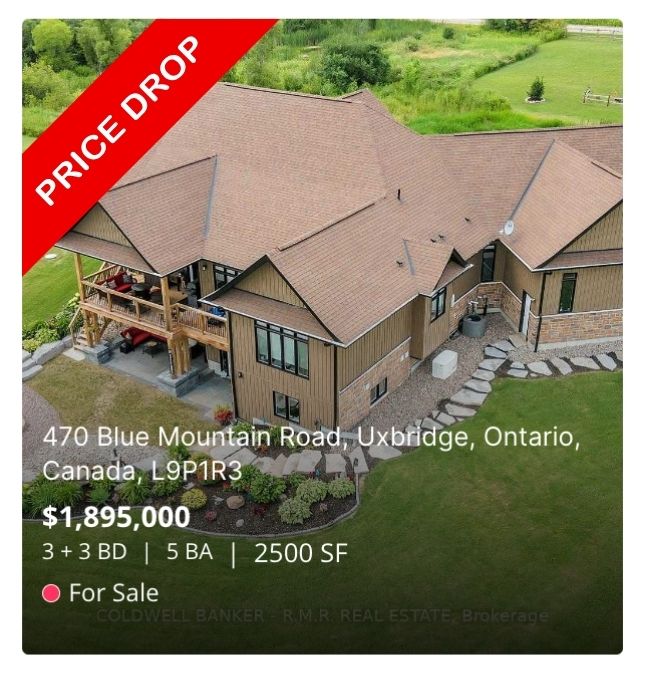

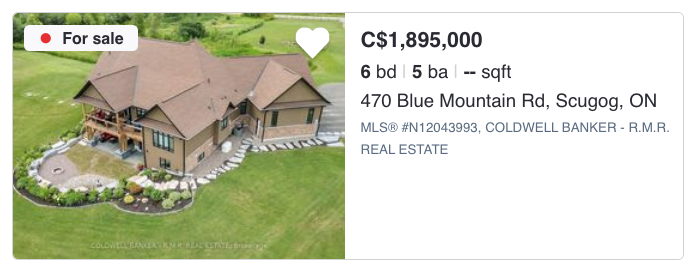

Thank You For The Booked Showing – 470 Blue Mountain Rd!

Thanks for Booking A Showing for 470 Blue Mountain Rd by @YorkDurhamHomes

Property Update •

November 20, 2025

Thank You For The Booked Showing – 12885 Hwy 12!

Thanks for Booking A Showing for 12885 Hwy 12! Gerald Lawrence -REALTOR®

Market Update •

November 8, 2025

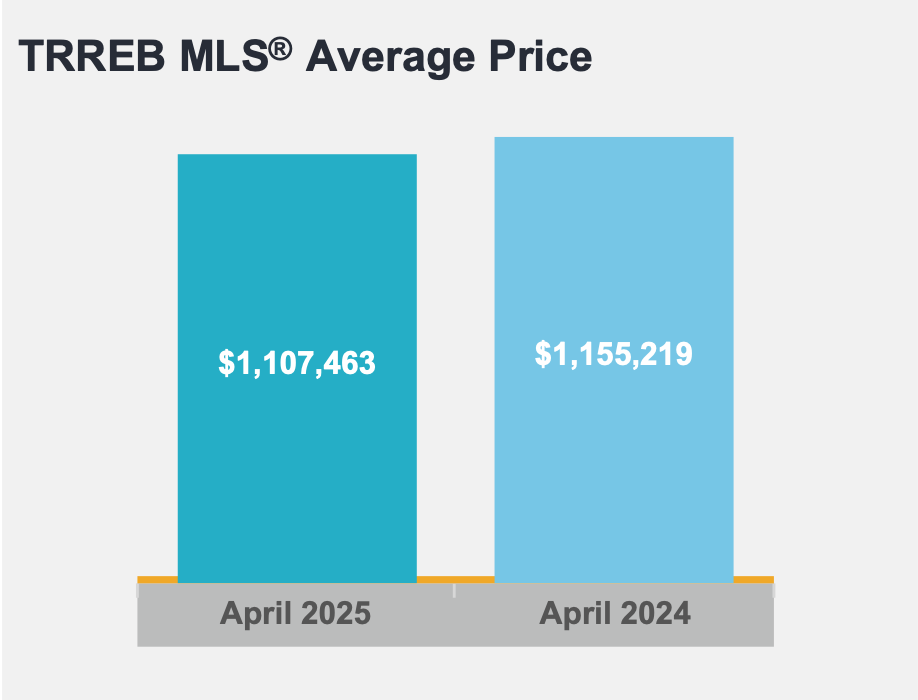

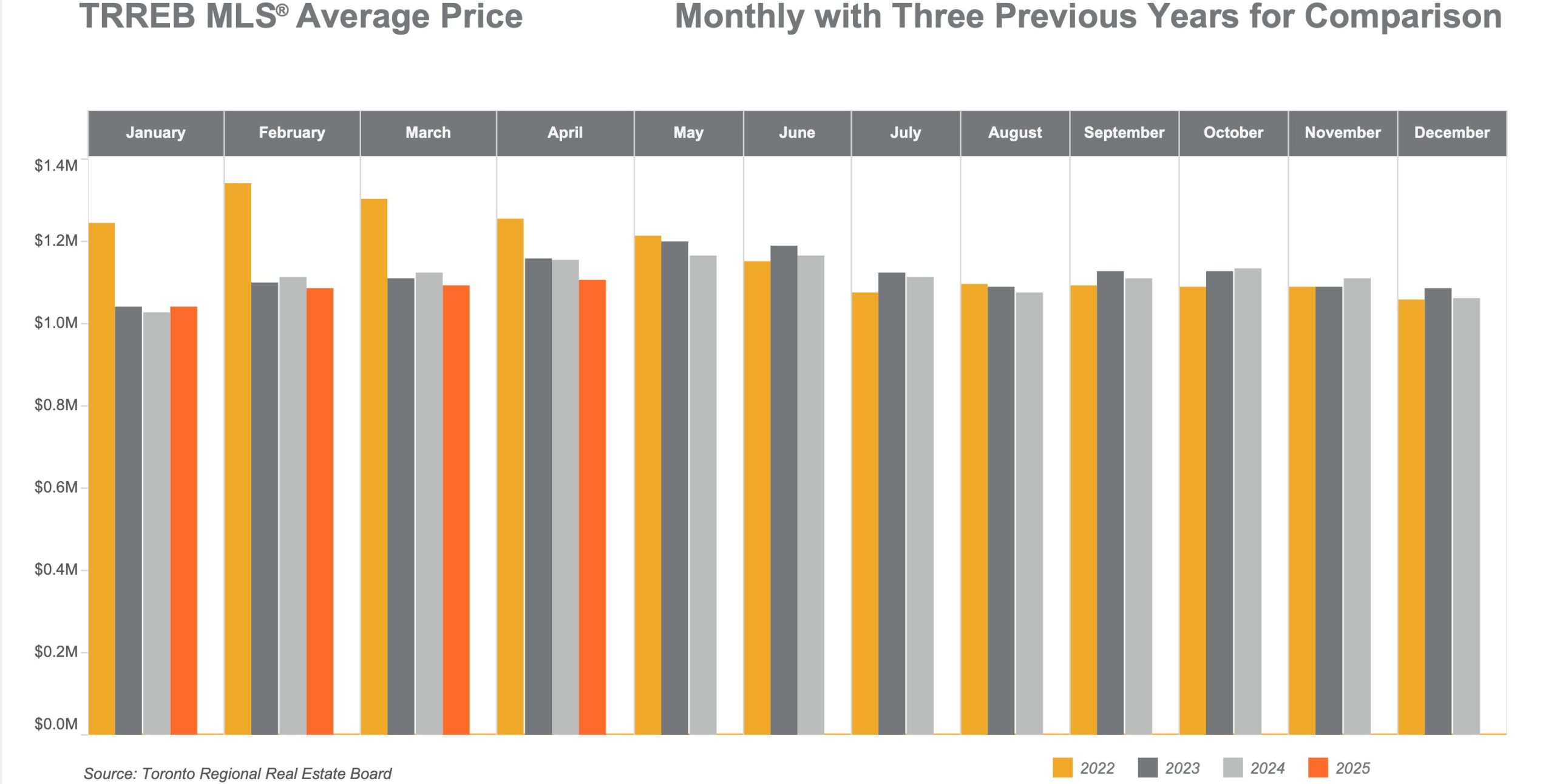

STOP WAITING: GTA Home Prices CRASHED 7.2%! 📉 The October/November Secret Buyers Need to Know Now

The October 2025 Durham Region real estate report reveals a balanced housing market characterized by lower home sales, increased inventory, and easing prices. The average sale price in Durham slipped by about 4-5% year-over-year to roughly $850,000, while homes sold for just under their list price and spent more time on the market. Inventory levels climbed to multi-year highs, giving buyers more options and shifting negotiations in their favor, yet some segments remain competitive—especially lower-priced properties. Sellers are adjusting expectations as market balance improves, and buyers benefit from greater choice and negotiating room, all amid ongoing economic uncertainty, declining mortgage rates, and steady but cautious transactional activity.

Screenshot

Durham Region Real Estate Market October 2025: Key Insights

October 2025 saw shifting dynamics in the Durham Region housing market. Home sales experienced a decline year-over-year, while new listings edged up, signaling a more favorable climate for buyers than in recent years. Lower mortgage rates and downward adjustments in selling prices improved affordability, though broader economic uncertainties are holding some buyers back.

Year-Over-Year Performance

-

Sales Volume: Home sales were down 9.5% in October 2025 compared to October 2024, echoing a region-wide cooling trend.

-

Listings: New listings increased by 2.7% year-over-year; active listings supply remains healthy, bolstering buyer options.

-

Average Price: The region’s average selling price fell by 7.2% compared to October 2024, showing a significant year-over-year price correction.

-

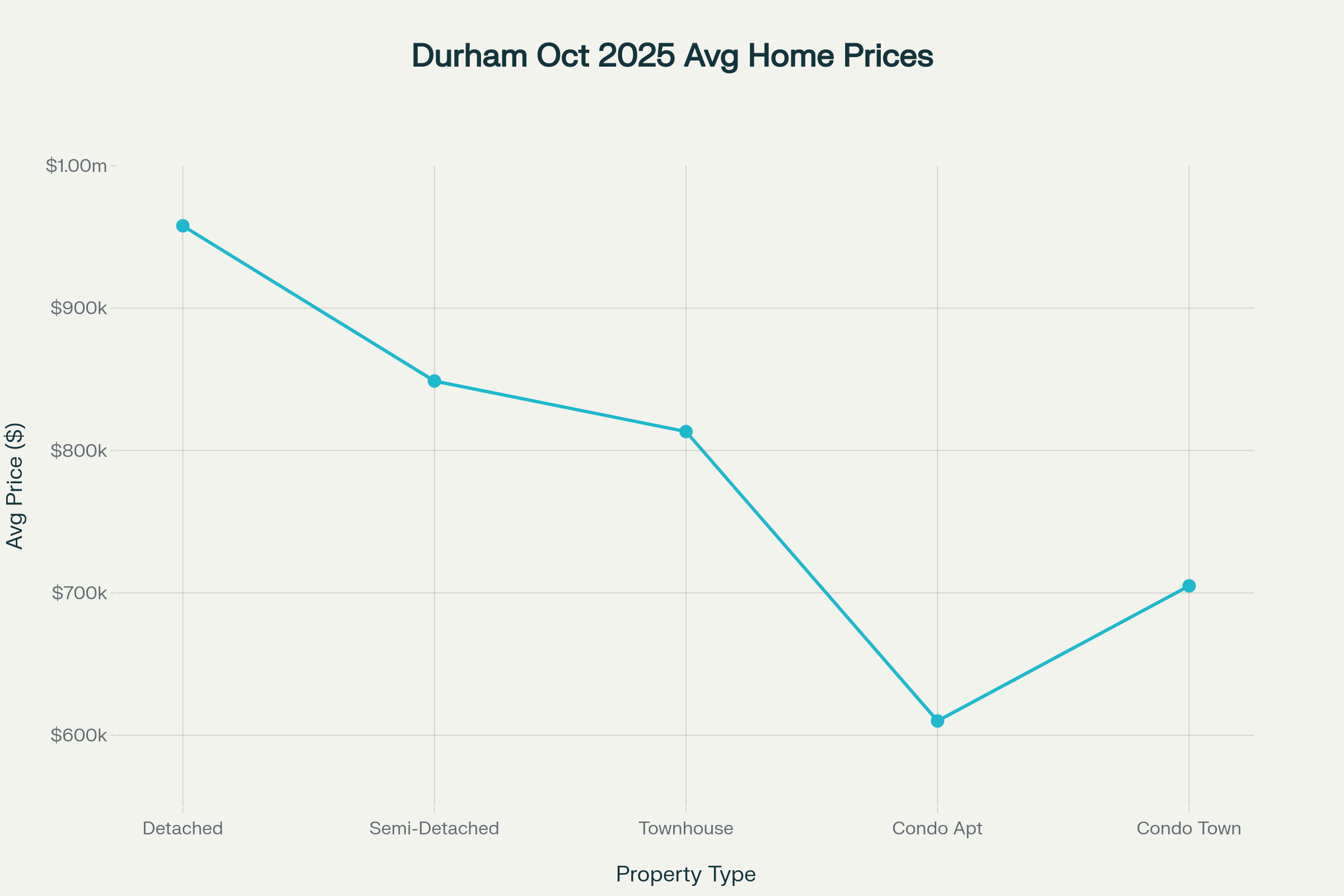

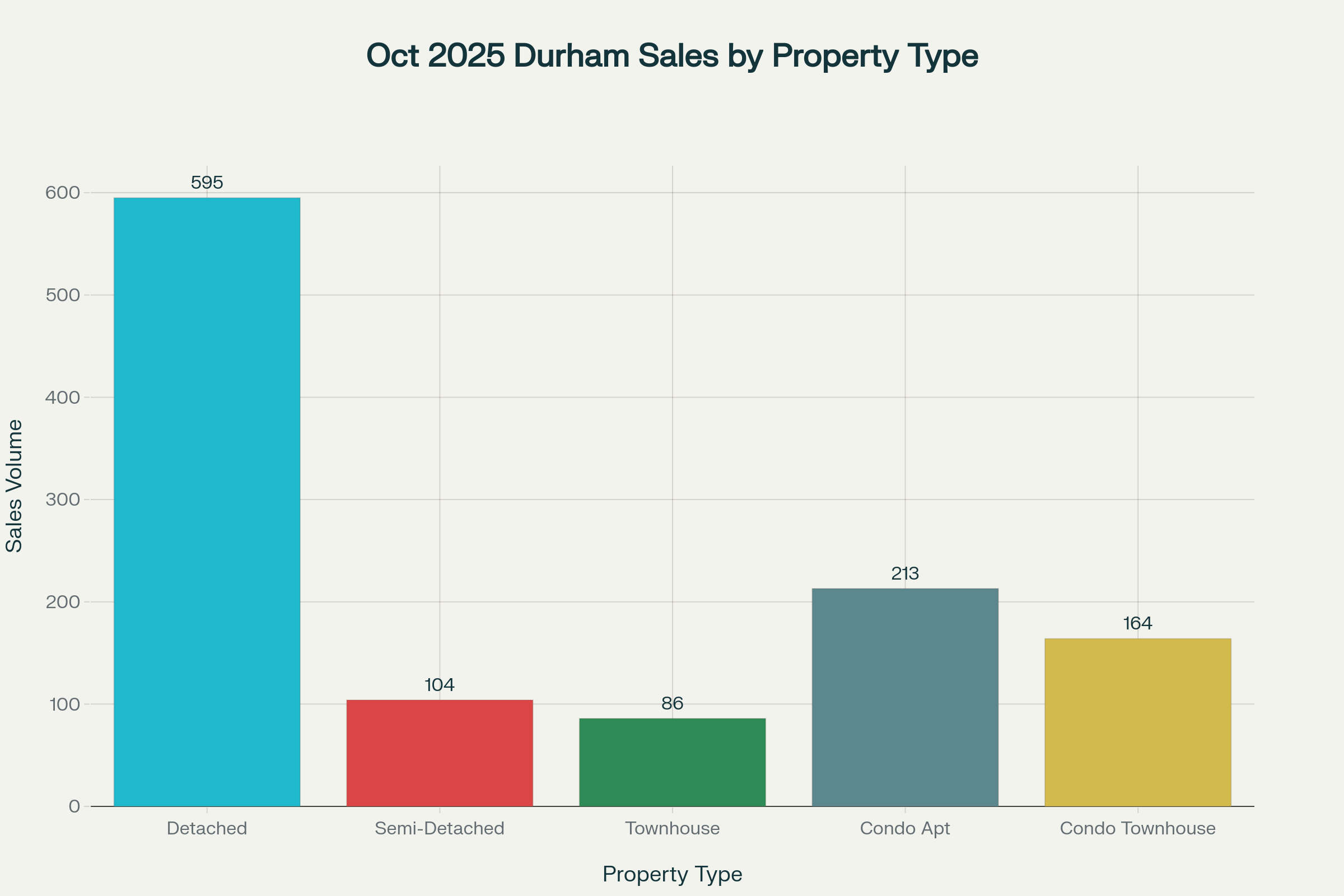

Benchmarks: In Durham, detached homes averaged $957,800, while townhouses and condos posted average prices of $813,300 and $610,000, respectively.

Market Segmentation: Home Types and Price Ranges

Detached and Semi-Detached Trends

-

Detached Homes: Average price was $957,800, with 595 transactions. Volumes were down and prices adjusted by about 10% year-over-year, reflecting overall softer market conditions.

-

Semi-Detached: These properties averaged $848,800 with 104 sales. Year-over-year price drop was about 8%, underscoring increasing price sensitivity among buyers.

Townhouses and Condominiums

-

Townhouses: The average sale price for townhomes stood at $813,300, slightly higher supply and moderate demand led to more negotiation on sales prices.

-

Condo Apartments: Durham’s average price for a condo apartment in October 2025 was $610,000, down almost 7% year-over-year. The volume for condo apartment sales was 213, demonstrating stable but selective buyer intent in this segment.

-

Condo Townhouses: These reached an average price of $704,900, signaling relative stability in entry-level housing.

Sales Volume and Price Range Data

| Home Type | Sales Volume | Avg. Price | YoY % Change |

|---|---|---|---|

| Detached | 595 | $957,800 | -10% |

| Semi-Detached | 104 | $848,800 | -8% |

| Att/Row Townhouse | 86 | $813,300 | -7% |

| Condo Apt | 213 | $610,000 | -7% |

| Condo Townhouse | 164 | $704,900 | -7% |

Inventory, Listings, and Buyer/Seller Dynamics

Inventory and Listings

-

Months of Inventory: Durham Region held around 4–5 months of inventory, up slightly year-over-year. This metric indicates a slowly growing buyer’s market, with more choice and less upward price pressure.

-

SNLR (Sales-to-New-Listings Ratio): Durham’s ratio hovered in the low 30s, indicative of balanced market conditions. Buyers now have more negotiating power, which translates into lower sale-to-list price ratios.

Buyer and Seller Strategies

-

Affordability: Lower interest rates and price drops have improved affordability for qualified buyers, especially those with job security and stable financing.

-

Listing Strategy: Sellers need to price realistically and stage homes attractively, as days-on-market are up, and average property days on market (PDOM) often exceeds 30 days.

-

Investor Impact: Investors have returned to monitoring the market closely for signs of price bottoms, but most are remaining selective, focused on properties that will cash-flow under higher interest costs.

Durham Region: Community-Specific Highlights

-

Ajax: 48 detached homes sold at an average of $957,800, while 15 condos averaged $610,000. Average listing days on market ranged from 20 to 30 days.

-

Oshawa: 144 detached transactions with an average price of $704,900; the town remains a magnet for entry-level buyers due to relatively affordable prices across all property categories.

-

Pickering and Whitby: Both cities maintained robust new listing activity and had average sale prices in the high $900,000s for detached, with strong diversity in available inventory from condos to large single-family homes.

Economic Factors and Forward-Looking Statements

-

Interest Rates: The Bank of Canada’s overnight rate in October was 4.7%, with most mortgage products reflecting favorable buyer terms. Weaker monthly sales contributed to weaker price gains, but falling borrowing costs create longer-term optimism.

-

Unemployment: Toronto’s seasonally adjusted unemployment rate dropped to 2.3%, supporting buyer confidence but not eliminating broader economic anxieties.

-

Policy Watch: Calls continue for governments to cut buyer costs, end exclusionary zoning, and prioritize new construction, especially as the population grows and housing diversity becomes critical.

What to Expect in Durham Region Real Estate

The Durham Region real estate market in October 2025 provided a classic example of the transition to a buyer-favored environment. While price corrections and increased supply benefitted buyers, overall sales volumes declined as some remained sidelined due to uncertainty. If macroeconomic confidence rebounds, expect pent-up demand to gradually return, particularly if borrowing costs remain low and local job markets stay robust. For now, Durham’s property market offers opportunity for buyers and a clear message to sellers: adapt strategies to this more competitive climate.

The Greater Toronto Real Estate Market Update

The Greater Toronto Area (GTA) real estate market in October 2025 has created a rare and powerful window of opportunity for homebuyers. The latest stats from GTA REALTORS® confirm a clear shift to a buyer’s market, marked by increased inventory, lower prices, and more affordable mortgage payments.

If you’ve been waiting on the sidelines, this is your sign to move forward with confidence.

📉 Buyer Advantage: Prices & Payments Are Down

October’s data presents an undeniable financial benefit for buyers with long-term certainty in their employment and income.

- Average Selling Price Down: The average selling price in the GTA dropped to $1,054,372, a significant 7.2% decrease compared to October 2024.

- Lower Monthly Payments: As TRREB’s Chief Information Officer noted, the monthly mortgage payment for an average-priced home is trending lower. This is due to the combined effect of negotiated price reductions and generally lower borrowing costs, making homeownership more accessible.

- Price Benchmark Eased: The MLS® Home Price Index (HPI) Composite benchmark was down by five per cent year-over-year. This indicates a broader, sustained cooling in home values.

Key Takeaway: You can now enter the GTA housing market at a more affordable price point and secure a lower monthly payment than buyers faced just one year ago.

🏡 More Choice: Inventory Is Up

Buyers now have time to breathe, compare, and make a decision without the pressure-cooker bidding wars of the past.

- Listings Increase: New listings totaled 16,069 in October, a 2.7% increase year-over-year. While sales were down, the increase in listings means a more diverse selection of properties for you to choose from.

- Conditions Favour Buyers: With sales down by 9.5% year-over-year against a rise in new listings, the competition is significantly reduced. This is the definition of market conditions that favour homebuyers, giving you the negotiating leverage you’ve been waiting for.

🚀 Seize the Negotiation Window!

The current market dynamic won’t last forever. As TRREB experts suggest, once economic uncertainty fades and business confidence returns, demand is likely to increase and tighten the market again.

The time to act is now, while inventory is high, prices are favourable, and your negotiation power is at its peak.

Don’t wait for the next wave of buyers to jump in. Secure your future home and lock in your price before the market starts to turn.

🔥 Buyers: Stop Waiting! Schedule Your Exclusive Strategy Call TODAY.

Ready to capitalize on lower prices and higher negotiating power? Let’s discuss a tailored buying strategy to find your dream home at the best possible value.

Click Here to Schedule a Free, No-Obligation Buyer Consultation Now!

Are you a homeowner thinking of selling? Even in a buyer’s market, a properly priced and professionally marketed home will still attract the right buyer.

✅ Sellers: Get a Free, Expert Home Valuation.

Don’t let market headlines scare you. Discover what your home is truly worth in today’s competitive environment.

Find Out Your Home’s Current Value – Get Your FREE Market Report!

GTA Real Estate Market, October 2025 Stats, Buyer’s Market GTA, Lower Mortgage Payments, Toronto Home Prices Down, GTA Housing Market Forecast, Buy a Home in Toronto, Negotiation Power Real Estate, Affordable GTA Homes

Market Update •

November 3, 2025

🤯 A Weekend of Overload: Clocks, Cleats, and ‘Staches in the GTA

What a whirlwind! If you live in the Greater Toronto Area, this past weekend wasn’t just another spin around the calendar—it was a sensory overload of major events, from time-bending clock changes to nail-biting sports drama and the annual start of a hairy health initiative. It truly felt like everything was happening all at once.

Let’s break down the trifecta that made the last couple of days a massive moment in the city.

⏰ The Great Fall Back: An Extra Hour of Chaos

It began late Saturday night/early Sunday morning with the semi-annual ritual that is Daylight Saving Time (DST) ending. The clocks “fell back” an hour, giving us all the theoretical gift of a glorious extra hour of sleep.

But let’s be honest, it was a little more chaotic than peaceful. Did you set your clock back an hour before bed? Did your phone do it automatically? Did you wake up an hour early, momentarily panic, and then realize you had a bonus hour to… well, probably check Twitter for Blue Jays updates? The GTA’s collective internal clock just got a hard reset, and it’s a groggy adjustment for everyone.

💔 The Heartbreak on the Diamond: Blue Jays’ World Series Thriller

Speaking of Blue Jays updates, the end of DST coincided with one of the most agonizing and electric finishes to a baseball season in recent memory! The last two Blue Jays World Series games were nothing short of a spectacular, emotional rollercoaster.

Game 6 and the decisive Game 7 had us all glued to our screens, shouting at the television, and riding every pitch. The games were a nail-biting, edge-of-your-seat marathon, culminating in a truly heartbreaking loss in extra innings in Game 7. From incredible plays to clutch home runs that had the Rogers Centre crowd absolutely roaring, the team left absolutely everything on the field. It was a tough end, but what an unforgettable run! Thank you, Blue Jays, for a season that kept the entire country on the edge of its collective dugout.

The Show Must Go On: What’s Next for Toronto Sports?

With the baseball season officially over, the Toronto sports focus immediately pivots. This past weekend’s drama was actually preceded and followed by major action on the ice and the court! The Toronto Maple Leafs (NHL) and the Toronto Raptors (NBA) are already well into their seasons, providing the next major events to rally around. After a few rescheduled games to accommodate the Jays, the Leafs and Raptors now take centre stage in their respective title chases. Expect the excitement to shift from the Rogers Centre to the Scotiabank Arena for the foreseeable future!

🧔 Grow for a Great Cause: Movember is HERE!

As the calendar officially flipped, November arrived, and with it, the start of Movember. For those new to the movement, Movember is a global initiative dedicated to raising funds and awareness for men’s health, particularly prostate cancer, testicular cancer, and men’s mental health and suicide prevention.

The visible sign of support? Men growing out their moustaches for the entire month! This weekend was the crucial “Shave Down,” where countless men across the GTA went clean-shaven, ready to start growing their ‘staches for the cause. It’s an excellent conversation starter and a highly visible tribute to the fight against men’s health issues. Keep an eye out for the fledgling Mos around town!

How to Get Involved with Movember Fundraising

Want to do more than just grow a killer ‘stache? There are many ways to support Movember in the GTA:

- Grow a Mo: The classic way! Register on the Movember website, shave down, and get your friends and family to donate to your “Mo Space” fundraising page.

- Move for Movember: Not a grower? Commit to running or walking 60km over the month. That’s 60 kilometres for the 60 men we lose to suicide globally, every single hour.

- Host a Mo-ment: Organize a fun event, like a trivia night, a bake sale, or a friendly sports tournament (maybe a post-Blue Jays softball game!) and charge an entry fee as a donation.

- Mo Your Own Way: Take on any unique challenge! Give up coffee for the month and donate the savings, or try a personal fitness challenge.

The money raised goes to fund groundbreaking men’s health projects, so every action makes a difference!

A Weekend to Remember

So, this past weekend was a lot. We collectively gained an hour, lost a championship, and started an entire month-long facial hair journey, all within a 48-hour window. It was a weekend that proved the city doesn’t slow down, even when the clocks do. Now, as we adjust to the earlier sunsets, mourn the season, and embrace the fuzz, let’s carry that incredible energy into the next phase of the Toronto sports calendar and the vital mission of Movember.

What was the most memorable part of your whirlwind weekend? Let me know in the comments!

Mortgage Update •

October 31, 2025

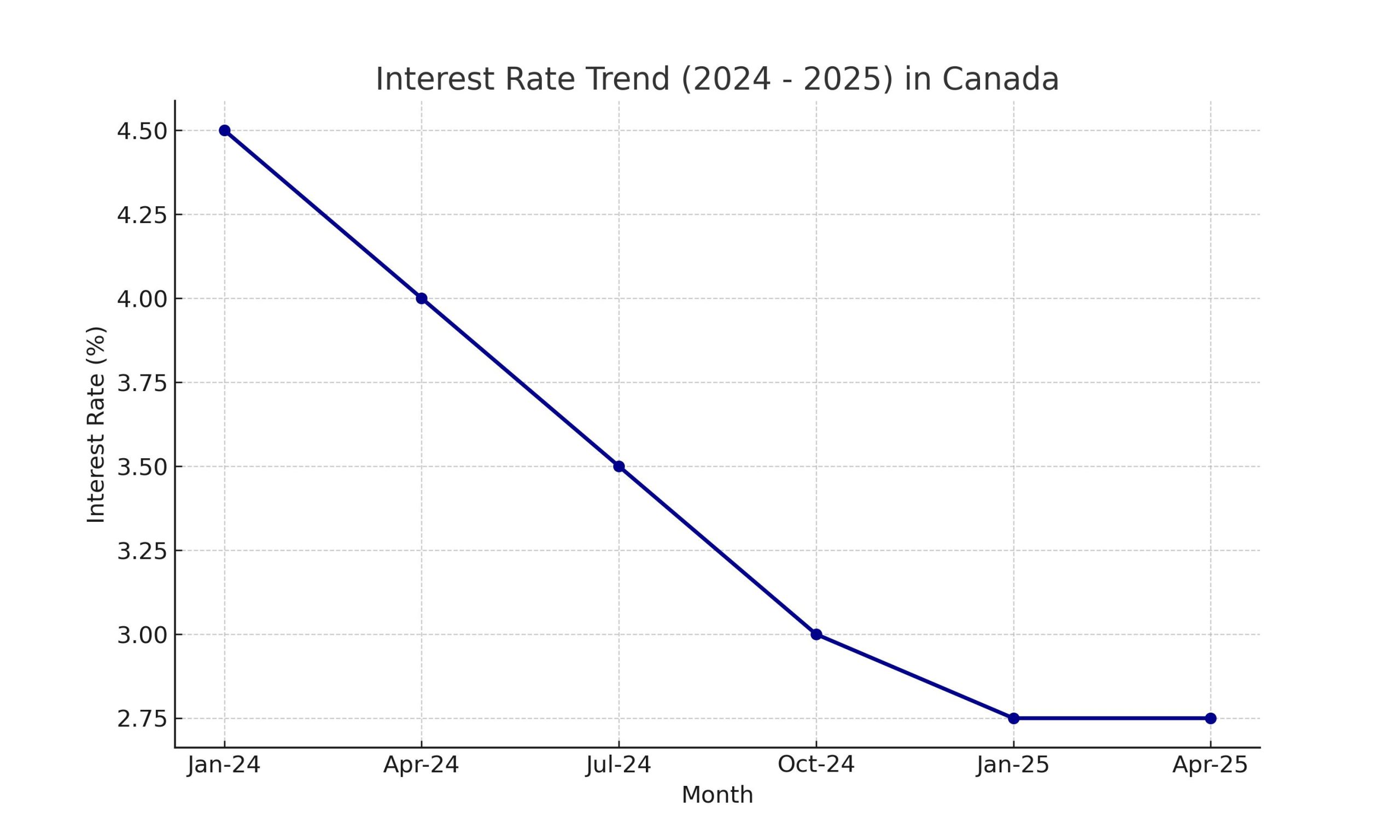

What the Bank of Canada’s Recent Rate Cut to 2.25% Means for Real Estate in Ontario 🏡

As a REALTOR® working in the Toronto area, this week’s interest-rate decision by the Bank of Canada (BoC) is very meaningful for you—whether you are on the buy side or the sell side of a real-estate transaction. Below is a breakdown of the decision, its real-estate implications, and how you and your clients can respond.

1. What did the Bank of Canada decide?

-

On October 29, 2025 the Bank of Canada cut its target overnight rate by 25 basis points, bringing it to 2.25%.

-

The Bank Rate now stands at 2.50% and the deposit rate at 2.20%.

-

The BoC signalled that, if inflation and activity evolve broadly in line with its October projections, “the current policy rate is at about the right level …” and further cuts are not guaranteed.

-

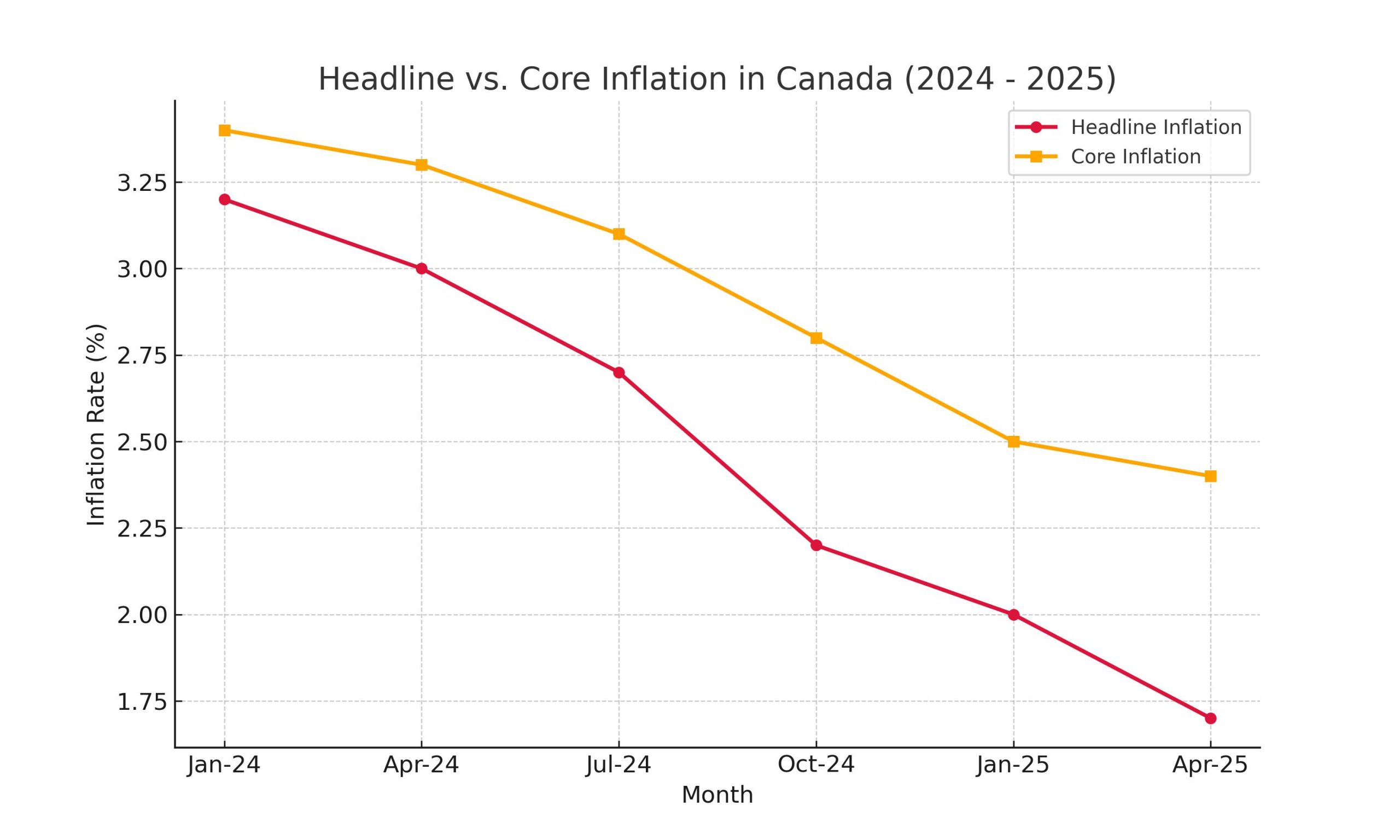

The underlying economic backdrop: modest growth, trade-headwinds (particularly U.S. tariffs) and inflation near, but slightly above, 2% (with core inflation a little higher) are influencing the decision.

In short: borrowing costs for banks should ease slightly (or at least stabilise) and the BoC is signalling caution about further rate moves—so this is a window of opportunity.

2. Why this is especially relevant for the real-estate market

For Buyers:

-

Lower policy rates => banks may offer slightly better mortgage terms (or at least less upward pressure) which can boost affordability.

-

If variable-rate or adjustable mortgage products respond quickly to BoC moves, you may see a dip in payments or an improved debt‐service ratio.

-

With this rate cut signalling a potential floor, buyers may be more confident stepping into the market now rather than waiting.

Call to action for buyers: If you’ve been on the fence, let’s review your financing options now—this could be a timely moment to lock in favourable terms before any shifting sentiment or rate increases.

For Sellers:

-

A marginally better affordability environment can broaden the buyer pool—especially first-time buyers or investors who were hassled by elevated rates.

-

Motivation to list now: If rates remain near current levels and affordability improves, competition can heat up. Listing later could mean facing more competition or less favourable financing for buyers.

Call to action for sellers: Let’s evaluate your home’s market value now, prepare your property for listing, and capitalise on potentially improved buyer demand while this window is open.

3. What’s going on in the Ottawa decision and economy

-

The BoC emphasised that “ongoing weakness in the economy and inflation expected to remain close to the 2 % target” drove the decision.

-

On the flip side, the trade‐shock (tariffs) has elevated costs for certain sectors and added uncertainty, meaning the Bank remains cautious.

-

According to projections, growth remains modest and risks remain elevated — meaning the BoC has to balance supporting the economy and keeping inflation contained.

-

Mortgage rates don’t immediately mirror the policy rate, but the policy rate serves as a key anchor for banks’ cost of funds and thus influences what lenders offer.

📌 Real-estate note: While a 25 basis-point cut may not immediately translate into a dramatic drop in mortgage rates, the expectation of easier policy and stable rates matters for buyer psychology and listing strategies.

4. How this affects the Toronto / Ontario market specifically

-

In the greater Toronto region, affordability has been a key issue—higher interest rates squeezed budgets and slowed some sales activity. An easing environment can help.

-

Sellers who might have been cautious may now find there are more qualified buyers coming off the sidelines.

-

For investors: lower financing costs can improve cash-flow projections and return calculations, making small-scale investment properties more attractive again.

-

For first-time buyers: this may be a timely reminder to revisit budgeting and purchase-readiness.

-

As your REALTOR®, I can help interpret how this interest-rate backdrop translates into your specific neighbourhood, home-type, and budget scenario.

5. Strategic next-steps for you

Buyers:

-

Get pre-qualified now—we’ll work with your lender to survey the impact of the rate cut on your mortgage options.

-

Review fixed vs variable rate strategies in light of this decision and your risk-tolerance.

-

Expand your search with confidence: if the payment burden eases, you might access homes you thought were out of reach.

-

Let’s craft an offer strategy that capitalises on this moment of improved affordability.

Sellers:

-

Let’s conduct a market evaluation now: assess your home’s competitive positioning in the upcoming window of opportunity.

-

Prepare your home—staging, minor repairs, presentation—to ensure you’re ready to list when buyer interest rises.

-

Timing matters: listing now may catch buyers before they shift focus to other markets or before inventory builds.

-

Let’s discuss pricing strategy that reflects the slightly improved financing environment for buyers.

6. Visualising the Impact

🍁 What This Fall Market Means for Buyers in the GTA

The Bank of Canada’s latest rate cut to 2.25 % is more than just a headline — it’s a tangible opportunity for GTA buyers. With borrowing costs easing and lenders adjusting their fixed and variable mortgage products, your buying power has effectively increased. Whether you’re a first-time buyer trying to break into the market or a move-up buyer seeking more space, this fall could be the ideal time to act.

The GTA housing market remains diverse — from Toronto’s condo corridors to family homes in Durham, York, and Peel regions — and we’re already seeing signs of renewed buyer interest since the rate announcement. That means inventory may start tightening again as more buyers re-enter the market, especially for well-priced homes in desirable neighbourhoods.

Now is the time to take advantage of improved affordability and a slightly less competitive environment before momentum builds again.

Let’s sit down for a confidential buyer consultation to review your goals, pre-approval options, and neighbourhood strategies. As your REALTOR®, I’ll help you secure the right property at the right price — while the market is still in your favour.

📞 Call, text, or email me today to schedule your private consultation and discover what your next move could look like in this evolving market.

🍂 What This Fall Market Means for Sellers in the GTA

For sellers, the fall 2025 market brings renewed optimism — and a valuable window of opportunity. Lower interest rates are stimulating demand and improving buyer confidence, which can translate into more showings, stronger offers, and shorter days on market. Many prospective buyers who had paused earlier this year due to higher borrowing costs are now stepping back in.

This means your property could attract a larger and more motivated pool of buyers, particularly if it’s priced right and presented effectively. From professional staging to tailored marketing plans, positioning your home now — while the market is adjusting to this new rate environment — can help you stand out before winter listings begin to taper off.

Don’t wait until everyone else catches on to the changing momentum. Let’s review your home’s market value, current competition, and strategies to maximise your return this season.

Book your confidential seller consultation today, and let’s prepare your property to make the strongest impact in this more favourable market environment.

💼 Reach out directly for a no-obligation, one-on-one conversation — your timing, pricing, and preparation decisions today can make all the difference in your sale results tomorrow.

Navigating This Market with a Professional Advantage

Markets don’t wait — and opportunities like this come in cycles. Whether you’re buying your first home, upgrading, or selling an investment property, strategic timing and expert guidance matter.

As a trusted REALTOR® in the GTA, I provide market insight, negotiation expertise, and data-driven strategies to help you move confidently in today’s evolving landscape.

📲 Let’s talk confidentially about your next move.

I offer private consultations for both buyers and sellers to help you make smart, well-timed decisions in this shifting market.

Let’s turn this moment — and this rate cut — into your next real estate success.

7. Final Thoughts & Your Next Move

This week’s rate cut by the Bank of Canada is an important signal to both buyers and sellers: the environment for real-estate transactions is shifting favourably. Buyers have an opportunity to act with somewhat improved affordability, and sellers have a chance to access a broader buyer pool.

👉 If you are considering entering the market — contact me today. I’ll provide a tailored consultation:

-

For buyers: we’ll map out the best financing strategy and target homes at your new budget.

-

For sellers: we’ll prepare your home for listing, capitalise on current conditions, and hit the market at an optimal time.

Let’s leverage this interest-rate moment together. Markets move quickly when policy pivots. I’m here to ensure you’re ready.

The real estate market inside scoop for the community you love. See homes that are for sale and have recently sold. Find out if home sales in your neighbourhood are trending up or down. See what homes around you are currently selling for.

Market Update •

September 17, 2025

Interest Rates Drop Again — Is Now the Time to Buy or Sell in the Greater Toronto Area?

Bank of Canada Rate Cut + GTA Market Snapshot

Bank of Canada Rate Cut + GTA Market Snapshot

Bank of Canada Rate Cut + GTA Market Snapshot

Bank of Canada Rate Cut + GTA Market SnapshotOn September 17, 2025, the Bank of Canada made its latest policy move:

-

The overnight rate was cut to 2.50%, down from 2.75%.

-

This came after several “holds” and in the context of weaker economic data: job losses, rising unemployment, softening demand, cooling inflation.

This change has immediate and potential implications, especially in a market like the GTA, which has been under pressure from affordability issues, declining prices, and high inventories. Let’s dig into what’s happening locally and how both buyers and sellers might respond.

GTA Real Estate Market: Key Metrics & Trends

Here are some of the more recent GTA housing market numbers (August 2025) that matter, especially in light of the rate cut:

| Metric | Value / Trend | Implication |

|---|---|---|

| Average home sale price (GTA, all types) | ~$1,022,143 — down ~4.9% year-over-year. | Prices have softened; potential opportunity for buyers, less upside for sellers unless property is strongly differentiated. |

| Detached homes | ~$1,312,240 — among the biggest drops (~7.2% YoY) in GTA. | Detached remains a premium segment; risk of more correction especially in outer suburbs or less in-demand locations. |

| Condominums | ~$642,195 — down ~4.8% YoY. | Condos remain under pressure, though lower entry cost may draw first-timers or investors. |

| Townhouses / Semi-Detached | Townhouses: ~$946,395; Semi-detached: ~$980,102; both down YoY. | Mid-priced homes have some correction, but not as steep in all sub-markets. |

| Sales vs. Listings (Supply) | Active listings high (~27,495 in August), up substantially vs previous years; new listings up; supply has outpaced demand. | Buyers have more options; more negotiating power; sellers will have to compete. |

| Sales Trend | Sales are increasing year-over-year modestly; buyer activity returning. | Suggests that affordability improvements are starting to matter. |

What the Rate Cut Means for GTA Buyers

With the Bank of Canada cutting to 2.50%, here are possible effects on buyers within the GTA, and strategies to take advantage.

| Benefit | How to Act |

|---|---|

| Lower borrowing costs | If you’re using a variable rate mortgage (or renewing soon), you may see immediate relief. Even small monthly savings can free up budget. |

| Improved affordability | Price drops + lower interest = a more favorable payment schedule. Particularly helpful for first-time buyers or those moving up. |

| More negotiation power | Greater choice among listings; less competition (fewer bidding wars in many segments); sellers may need to make concessions. |

| Opportunity to lock in | If fixed mortgage rates begin to follow (depends on bond yields), getting pre-approved and locking in could help avoid future costs. |

Risks / cautions for buyers:

-

Fixed mortgage rates may lag the policy rate change; not all lenders pass cuts immediately, and bond market conditions matter.

-

Economic uncertainty in the GTA/ON (jobs, trade, immigration) may dampen confidence; some buyers may still hesitate.

-

Even with lower rates, total cost (down payment, maintenance, taxes, etc.) remains high.

Recommended buyer strategies:

-

Get pre-approved now. Know exactly what you can afford.

-

Watch property types: mid-segments (townhouses/semi’s) may see better value than peak detached-home pricing.

-

Negotiate well: longer days on market, higher inventory = greater leverage. Ask for closing cost help, flexible possession, repairs.

-

Consider fixed vs variable carefully: variable may benefit sooner, but fixed gives stability if rates reverse.

-

Think long term: Even if market dips more, buying in GTA tends to build value over years—if you have the ability to hold.

What the Rate Cut Means for GTA Sellers

This rate cut may help stabilize some downward trends, but sellers need to adapt to current realities. Here’s how:

| Potential Opportunities | Things You’ll Need to Do Differently |

|---|---|

| More buyer interest | Buyers discouraged by high rates may return. Homes that are well priced and well presented will see attention. |

| Faster sales for strong listings | Properties that stand out (location, condition, value) may sell faster, even in a buyer’s market. |

| Benefit from easing affordability | Lower monthly payments for buyers expand the pool somewhat. Sellers need to recognize where buyers’ budgets are now. |

Challenges / risks for sellers:

-

Prices are down, particularly in detached and condos. Expect lower offers.

-

Longer time on market; more competition from other sellers.

-

Buyers will expect more — inspections, incentives, maybe closing terms.

Seller strategies:

-

Price realistically from the start — avoid overpricing. If you start too high, you’ll lose momentum.

-

Invest in presentation and staging — a well-maintained, move-in-ready home will stand out among many.

-

Flexible terms & incentives — consider assisting with closing costs, offering flexible closing dates, or providing minor upgrades/allowances.

-

Market smartly — highlight affordability relative to past peaks; show what monthly payments could look like post-rate cut.

-

Watch inventory & timing — there is evidence that inventory, after peaking, is starting to pull back. Becoming one of the early listings in a tightening market helps.

GTA Market Outlook & What Comes Next

Putting it all together:

-

The rate cut to 2.50% is generally favorable for the GTA, given ongoing price softening and high supply. It helps pull some buyers off the sidelines.

-

But this is not a magic fix: structural affordability remains a challenge — prices are still high relative to incomes, and many buyers remain cautious.

-

The balance of power still leans toward buyers in many neighbourhoods, though some sub-areas (especially in high demand) may see more balanced conditions as listings fall.

-

If economic data worsens (unemployment, trade, inflation), more rate cuts are possible. Conversely, if inflation spikes or supply gets tight, rates could stay stable or even rise again.

Call to Action

If you’re in the GTA and thinking about moving, now’s not the time to stay passive. Whether buying or selling, you need a plan. Here’s what to do:

-

Buyers: Reach out to mortgage brokers, get price-sensitive search set up, lock in pre-approval. Don’t just browse—calculate what your monthly payments will look like and act when you find value.

-

Sellers: Talk to one of our team member realtors who know your neighbourhood deeply. Price smart, spruce up your listing, and use the interest cut to show buyers what their payments might be under current conditions.

Want help zeroing in on your neighbourhood? I can pull together a custom GTA-neighbourhood report (price trends, comparable sales, days on market) so you can see whether your area is trending with the broader market, or diverging. Do you want me to put one together for your specific area?

Market Update •

July 6, 2025

Post #12278

📊 GTA Housing Market Update: June 2025

Your Complete Guide to Greater Toronto Area Real Estate Trends

🎯 Market Snapshot: What You Need to Know

The Greater Toronto Area housing market is showing fascinating dynamics in June 2025. Whether you're a potential buyer looking for the perfect opportunity or a seller considering your next move, understanding these trends is crucial for making informed decisions. Let's dive deep into the numbers that are shaping our market today.

Current Market Condition: BALANCED WITH BUYER OPPORTUNITIES

6,243

Total Home Sales

↓ 2.4% vs June 2024$1,101,691

Average Selling Price

↓ 5.4% vs June 202419,839

New Listings

↑ 7.7% vs June 202431%

Sales-to-Listings Ratio

↓ 4% vs June 2024🏠 SELLERS: Is Your Home Priced Right in Today's Market?

Get a FREE Comparative Market Analysis (CMA) tailored to your property's unique features and location. Know your home's true value in today's shifting market conditions.

GET YOUR FREE CMA NOW💰 Property Type Breakdown: Where the Value Lies

Understanding the price variations across different property types is essential for both buyers and sellers. Here's how each category performed in June 2025:

| Property Type | Average Price | Units Sold | Market Share |

|---|---|---|---|

| Detached Homes | $1,392,033 | 3,011 | 48.2% |

| Semi-Detached | $1,089,751 | 601 | 9.6% |

| Townhouse | $871,652 | 1,048 | 16.8% |

| Condominium | $696,424 | 1,510 | 24.2% |

📊 Sales Volume by Property Type

💡 Market Insight

Detached homes continue to dominate the market, representing nearly half of all sales. However, condominiums are showing strong activity, making up over 24% of transactions. This suggests a diverse market with opportunities across all price points.

📈 Market Trends: What the Numbers Really Mean

🏷️ Price Trends

The average selling price of $1,101,691 represents a 5.4% decrease from June 2024's $1,164,491. This price adjustment, combined with lower borrowing costs, is creating new opportunities for buyers who have been waiting on the sidelines.

Key Takeaway for Buyers:

Lower prices + reduced interest rates = improved affordability. This is potentially the best buying opportunity we've seen in recent years.

📋 Supply & Demand

With 19,839 new listings (up 7.7%) and 6,243 sales (down 2.4%), we're seeing increased choice for buyers. The sales-to-listings ratio of 31% indicates a balanced market with slight favor toward buyers.

Key Takeaway for Sellers:

More competition means strategic pricing and presentation are more crucial than ever. Professional guidance is essential now.

📊 Average Selling Prices by Property Type

🎯 BUYERS: Ready to Take Advantage of This Market?

With increased inventory and improved affordability, this could be your moment. Get a FREE consultation to explore your options and develop a winning strategy.

BOOK YOUR FREE CONSULTATION🎯 Strategic Insights: Expert Analysis

According to TRREB's latest market analysis, several key factors are shaping the current market dynamics:

🏦 Economic Factors

Interest Rate Environment: Lower borrowing costs compared to last year are improving affordability. Additional rate cuts could further strengthen market momentum.

Trade Relations: Economic uncertainty continues to keep some buyers on the sidelines. A firm trade deal with the United States could significantly boost consumer confidence.

🔍 Market Dynamics

Buyer's Market Characteristics: With more listings available, buyers are gaining negotiating power and securing discounts off asking prices.

Seasonal Trends: Month-over-month increases in sales, coupled with declining new listings, suggest a tightening trend through the spring season.

📊 Market Activity Comparison: June 2024 vs June 2025

🏠 What This Means for Sellers

The current market presents both challenges and opportunities for sellers:

📊 The Reality Check

- Increased Competition: 7.7% more listings mean more choice for buyers

- Price Adjustments: Average prices are down 5.4% year-over-year

- Longer Market Times: Properties may take longer to sell than in previous years

🚀 The Opportunities

- Motivated Buyers: Those entering the market now are serious about purchasing

- Strategic Positioning: Properly priced homes still sell efficiently

- Professional Advantage: Expert marketing and pricing strategies are more valuable than ever

📈 SELLERS: Maximize Your Property's Potential

Don't let market conditions discourage you. With the right strategy, pricing, and presentation, your home can stand out from the competition. Get your FREE CMA today!

REQUEST YOUR FREE CMA🎯 What This Means for Buyers

For prospective buyers, the current market conditions are creating excellent opportunities:

✅ Buyer Advantages

- More Choice: 19,839 new listings provide extensive options

- Negotiating Power: Buyers are securing discounts off asking prices

- Lower Costs: Reduced prices and lower interest rates improve affordability

- Less Competition: Fewer competing offers mean better chances of success

⚠️ Considerations

- Economic Uncertainty: Stay informed about broader economic trends

- Interest Rate Sensitivity: Be prepared for potential rate changes

- Property Condition: With more options, you can be selective about quality

📊 Sales-to-Listings Ratio Trend

🔮 Market Outlook: What's Next?

Based on current trends and expert analysis, here's what we anticipate for the remainder of 2025:

📈 Positive Indicators

- Gradual Recovery: Month-over-month improvements suggest building momentum

- Affordability Gains: Lower prices and borrowing costs are bringing buyers back

- Inventory Balance: Healthy supply levels support market stability

🎯 Key Factors to Watch

- Interest Rate Decisions: Additional cuts could significantly boost activity

- Trade Relations: Economic clarity could improve consumer confidence

- Seasonal Patterns: Traditional fall market dynamics may provide opportunities

💼 BUYERS: Don't Wait for Perfect Market Conditions

The best time to buy is when you find the right property at the right price. Let's explore what's available for you in today's market with improved affordability.

SCHEDULE FREE CONSULTATION🎯 Why Choose Gerald Lawrence as Your REALTOR®?

In a market with evolving dynamics, having an experienced professional by your side is more important than ever. Here's what sets me apart:

🏆 For Sellers

- Precise Market Analysis: Comprehensive CMAs that position your property competitively

- Strategic Marketing: Multi-channel approach to maximize exposure

- Professional Network: Access to qualified buyers and industry professionals

- Negotiation Expertise: Protecting your interests throughout the process

🎯 For Buyers

- Market Knowledge: Deep understanding of neighborhood trends and values

- Access to Listings: First look at properties matching your criteria

- Negotiation Skills: Securing the best possible terms and pricing

- Transaction Management: Smooth process from offer to closing

📞 Ready to Make Your Move?

Whether you're buying or selling, the current market presents unique opportunities that require expert navigation. Don't let these conditions pass you by without exploring what's possible.

🏠 Take Action Today!

SELLERS: Get your FREE Comparative Market Analysis and discover your property's true value in today's market.

BUYERS: Schedule your FREE consultation to explore the expanded opportunities available now.

FREE CMA FOR SELLERS FREE CONSULTATION FOR BUYERS

Data Source: Toronto Regional Real Estate Board (TRREB) Market Report, June 2025

Analysis by: Gerald Lawrence, REALTOR® - Coldwell Banker R.M.R. Real Estate, Brokerage

Property Update •

June 19, 2025

Move-In Ready & Full of Potential: Inside a Hidden Gem in the Heart of Stouffville

🏡 Just Listed: 14 Betula Gate, Stouffville

A Beautiful Start in a Family-Friendly Neighbourhood

Offered at $949,000

Welcome Home

A lovingly maintained 2-storey detached link home – perfect for young families and first-time buyers.

📍 Stouffville, ON | 🛏 3 Beds | 🛁 3 Baths | 🚗 1-Car Garage

📲 Book a Tour Today

Contact Me | 📞 416-556-0238

🧱 Why You’ll Love This Home

✅ Key Features

-

3 bright and spacious bedrooms, including a sunlit Primary Suite with 4-Piece Ensuite

-

3 bathrooms total — 2 full 4-piece bathrooms on the upper level, 2-Pc powder room on main floor, and a rough-in in the basement

-

Open-concept main floor — ideal for family time & entertaining

-

Eat-in kitchen with walkout to a fully fenced, landscaped backyard

-

Gas BBQ hookup, perennial flower beds, garden shed, and low-maintenance front garden

-

Built-in 1-car garage with backyard man-door

-

Finished basement featuring:

-

Recreation room

-

Bonus/office room

-

Utility & laundry room

-

Cold room and storage room with built-ins

-

-

2–5 mins from top-rated Barbara Reid PS, Sunnyridge Park, tennis & basketball courts

📍 Quiet street in a close-knit, family-oriented community!

📸 3D Interactive Virtual Tour

👨💼 About Gerald Lawrence

Hi, I’m Gerald — a full-time, full-service REALTOR® with Coldwell Banker R.M.R. Real Estate. I help first-time buyers and young families find homes where they can truly thrive. My knowledge of the Stouffville market and personalized approach ensure that you’ll feel confident and cared for every step of the way.

📧 Gerald-Lawrence@ColdwellBanker.ca

📞 416-556-0238

🌐 www.GeraldLawrence.Realtor

💬 What My Clients Say

❓ FAQs

Is this home move-in ready?

Yes — it’s been lovingly maintained by the original owner since 2010 and is in excellent condition.

What type of home is it?

It’s a 2-storey detached link home — fully detached above ground with a shared foundation wall below grade.

Can the basement be expanded?

Absolutely. The basement already mostly finished and has a rough-in for a full bathroom, allowing you to finish it to suit your needs.

Is the area good for families?

Definitely! It’s located within walking distance of Barbara Reid Public School, local parks, sports courts, and family amenities.

How do I book a tour?

📲 Contact me directly at 416-556-0238 or

📧 Email Click To Send Email

✉️ Interested in 14 Betula Gate? Let’s Talk!

Ready to book a showing or have a few questions? I’d love to help.

👉 Submit your inquiry below or email me directly.

📩 Click To Send Email

📞 416-556-0238

Your dream home could be just one message away.

🏡 Don’t miss out on 14 Betula Gate – Schedule Your Private Showing Now!

📞 416-556-0238 | 🌐 www.GeraldLawrence.Realtor

Market Update •

June 4, 2025

Rate Decision Breakdown: How US Tariffs and Rising Unemployment Are Shaping Canada’s Monetary Policy

🏦 Bank of Canada Holds Rate at 2.75%

🚦 BoC Hits the “Hold” Button: What Does It Mean For YOU? 🚦

The Bank of Canada’s job is like being the country’s economic pilot: they try to steer us toward stable prices (keeping inflation in check!) and healthy growth. Today’s decision to keep interest rates unchanged at 2.75% tells us a lot about what they’re seeing on their economic dashboard.

🔍 The Big Picture: Why the Hold?

The Bank’s Governing Council decided to keep rates steady because they’re navigating a complex economic landscape. Here’s what they’re seeing:

- Global Uncertainty is STILL High: 🌍 Especially concerning is the ongoing back-and-forth with U.S. tariffs and trade negotiations. This creates a big question mark for Canada’s export-driven economy. The Bank needs more clarity on how these trade policies will shake out.

- Canadian Economy: Softer, But Not Collapsing! 💪 Canada’s economy grew a bit stronger than expected in the first quarter (2.2% GDP growth!), driven partly by exports to the U.S. and inventory building. However, they expect the second quarter to be weaker as these factors reverse. Consumer spending has slowed, and housing activity is down, particularly resales.