Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The Bank of Canada (BoC) has officially held its target for the overnight rate at 2.25% today, April 29, 2026. For homeowners, aspiring buyers, and savvy investors, this decision is the “calm within the storm.” While the rate remains steady, the global landscape—shifting from Middle East tensions to new US trade policies—is creating a complex environment for the Canadian housing market.

As your dedicated real estate partner, I’ve broken down exactly how these macroeconomic shifts will hit your pocketbook and your property value.

1. The “Rate Hold” Breakdown: Stability in Uncertain Times

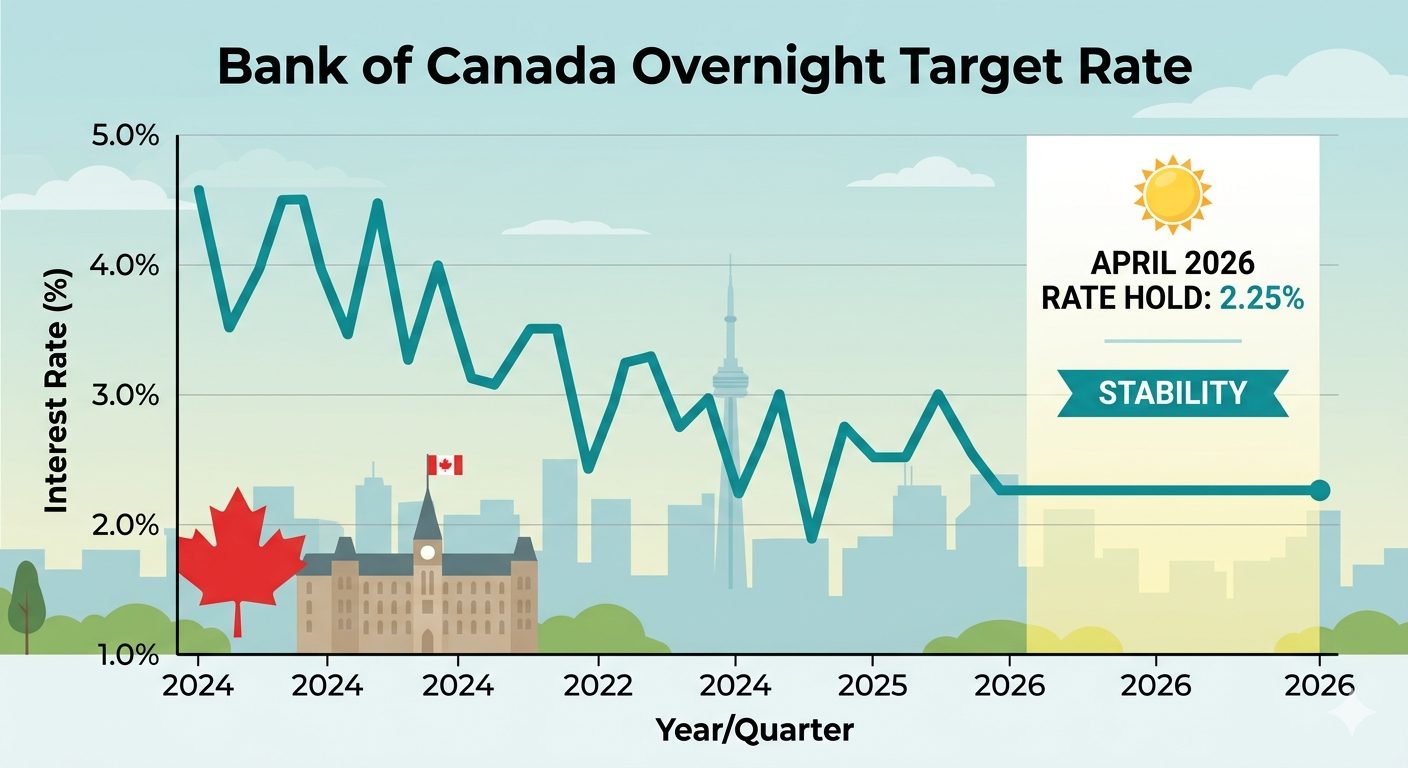

The Governing Council’s decision to maintain the policy rate at 2.25% (with the Bank Rate at 2.5% and the deposit rate at 2.20%) signals a “wait and see” approach. The Bank is currently balancing a soft domestic labour market against a global surge in energy prices.

For the real estate market, this means mortgage stress tests and variable rates will remain relatively unchanged for the next quarter. However, the Bank noted that CPI inflation rose to 2.4% in March and is expected to hit 3% in April due to gasoline prices.

Expert Insight for Sellers: Stability is a selling feature. With rates holding steady, buyers have more confidence in their monthly payment projections. If you’ve been waiting for a “predictable” window to list, this is it.

Click here to get a free, instant valuation of your home at GeraldLawrence.Realtor

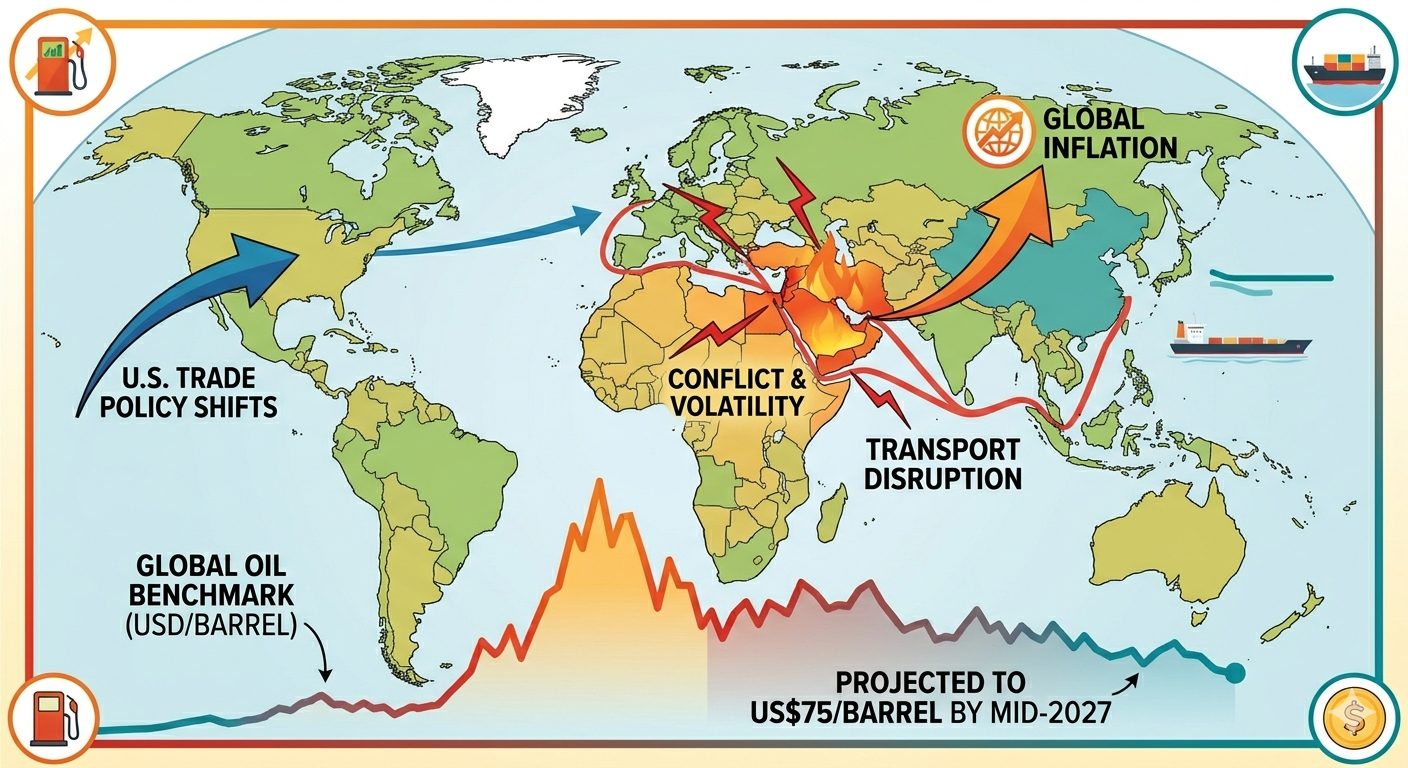

2. Global Volatility: The Iran War and Energy Costs

The ongoing conflict in the Middle East has sent shockwaves through the global economy. With oil prices projected to stay volatile before potentially declining to US$75 per barrel by mid-2027, Canadians are feeling the “gas pump squeeze.”

While higher oil prices actually boost Canada’s national income (as a net exporter), they simultaneously drain the disposable income of average households. This “dual impact” means that while the economy looks okay on paper, the average homebuyer has less cash left over for a mortgage after paying for heat and transport.

Expert Insight for Buyers: Don’t let the headlines scare you into inaction. While energy costs are up, the Bank of Canada expects inflation to return to the 2% target early next year. Locking in a home now before the next growth cycle could be your best long-term move.

Start your custom home search today at GeraldLawrence.Realtor

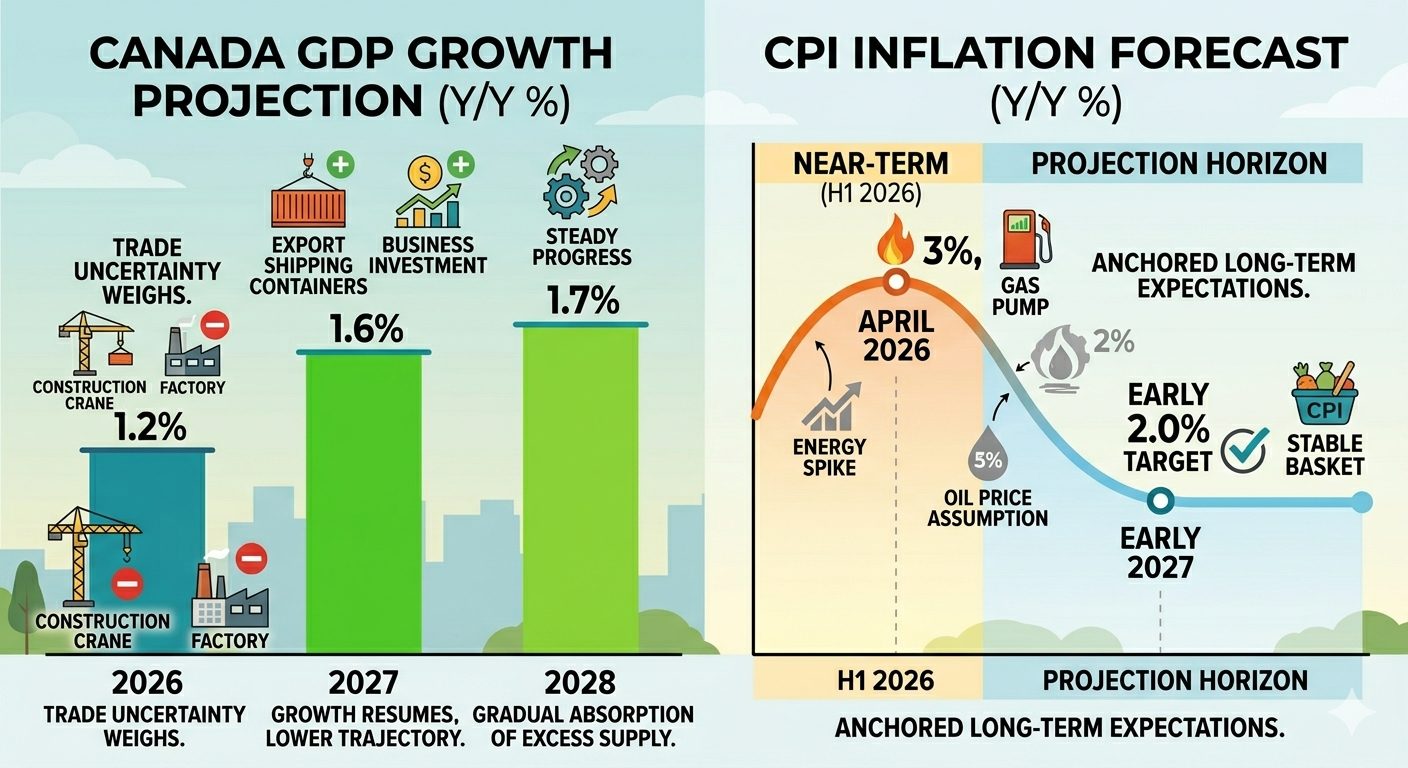

3. The US Trade Factor and the “Soft” Labour Market

The Bank highlighted that US trade policy and tariffs are weighing heavily on Canadian exports and business investment. We are seeing this reflected in a “soft” labour market, with the unemployment rate hovering between 6.5% and 7%.

| Economic Indicator | 2026 Projection | 2027 Projection |

| GDP Growth | 1.2% | 1.6% |

| Inflation (CPI) | ~3.0% (Near-term) | 2.0% (Early 2027) |

| Unemployment | 6.5% – 7.0% | Stabilizing |

The job losses in sectors targeted by US tariffs have led to a cautious sentiment in the housing market. However, with AI-related investments boosting US growth and Canadian businesses adapting to new trade patterns, the BoC expects a gradual recovery.

Expert Insight for Sellers: Pricing strategy is everything in a soft labour market. To attract the most qualified buyers, your home needs to stand out through professional staging and aggressive digital marketing.

See how I market homes differently at GeraldLawrence.Realtor

4. Real Estate Activity: Affordability and Supply

The Bank’s report was candid: Housing activity declined in late 2025 and is currently being held back by three factors:

-

Slow population growth.

-

General economic uncertainty.

-

Persistent affordability issues.

However, the “excess supply” in the general economy is being absorbed. As GDP growth rises toward 1.7% by 2028, the demand for housing is expected to outpace supply once again.

Expert Insight for Buyers: “Excess supply” is a phrase buyers love to hear. It means you have more leverage in negotiations than you’ve had in years. This is a rare “Buyer’s Market” window that may close as inflation anchors back to 2%.

View exclusive listings before they hit the market at GeraldLawrence.Realtor

5. Looking Ahead: The 2027 Recovery

The Bank of Canada is “looking through” the immediate spikes in energy prices, meaning they won’t hike rates just because gas is expensive—unless that inflation becomes “persistent.” Their forecast shows inflation returning to the 2% target early next year.

![]()

This suggests that 2026 is a “bridge year.” We are transitioning from the volatility of the mid-2020s into a more stable, growth-oriented period for 2027 and 2028.

Final Verdict: Should You Move Now?

-

For Sellers: You are competing in a market with fewer buyers, but those who are active are serious and benefit from stable rates.

-

For Buyers: You are in a unique position where “economic uncertainty” is providing you with more options and less competition.

The Bank of Canada is committed to price stability. I am committed to your financial success. Whether you are navigating a job change due to trade shifts or looking to downsize as energy costs rise, I have the data and the strategy to guide you home.

Ready to make your move in the 2026 market? Let’s chat.

Contact Gerald Lawrence directly at www.GeraldLawrence.Realtor