Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

As a REALTOR® working in the Toronto area, this week’s interest-rate decision by the Bank of Canada (BoC) is very meaningful for you—whether you are on the buy side or the sell side of a real-estate transaction. Below is a breakdown of the decision, its real-estate implications, and how you and your clients can respond.

1. What did the Bank of Canada decide?

-

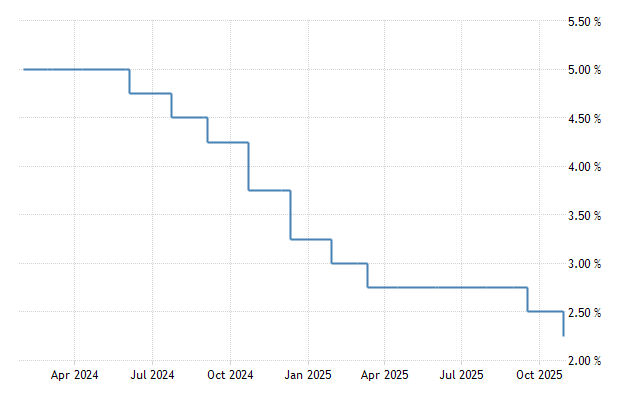

On October 29, 2025 the Bank of Canada cut its target overnight rate by 25 basis points, bringing it to 2.25%.

-

The Bank Rate now stands at 2.50% and the deposit rate at 2.20%.

-

The BoC signalled that, if inflation and activity evolve broadly in line with its October projections, “the current policy rate is at about the right level …” and further cuts are not guaranteed.

-

The underlying economic backdrop: modest growth, trade-headwinds (particularly U.S. tariffs) and inflation near, but slightly above, 2% (with core inflation a little higher) are influencing the decision.

In short: borrowing costs for banks should ease slightly (or at least stabilise) and the BoC is signalling caution about further rate moves—so this is a window of opportunity.

2. Why this is especially relevant for the real-estate market

For Buyers:

-

Lower policy rates => banks may offer slightly better mortgage terms (or at least less upward pressure) which can boost affordability.

-

If variable-rate or adjustable mortgage products respond quickly to BoC moves, you may see a dip in payments or an improved debt‐service ratio.

-

With this rate cut signalling a potential floor, buyers may be more confident stepping into the market now rather than waiting.

Call to action for buyers: If you’ve been on the fence, let’s review your financing options now—this could be a timely moment to lock in favourable terms before any shifting sentiment or rate increases.

For Sellers:

-

A marginally better affordability environment can broaden the buyer pool—especially first-time buyers or investors who were hassled by elevated rates.

-

Motivation to list now: If rates remain near current levels and affordability improves, competition can heat up. Listing later could mean facing more competition or less favourable financing for buyers.

Call to action for sellers: Let’s evaluate your home’s market value now, prepare your property for listing, and capitalise on potentially improved buyer demand while this window is open.

3. What’s going on in the Ottawa decision and economy

-

The BoC emphasised that “ongoing weakness in the economy and inflation expected to remain close to the 2 % target” drove the decision.

-

On the flip side, the trade‐shock (tariffs) has elevated costs for certain sectors and added uncertainty, meaning the Bank remains cautious.

-

According to projections, growth remains modest and risks remain elevated — meaning the BoC has to balance supporting the economy and keeping inflation contained.

-

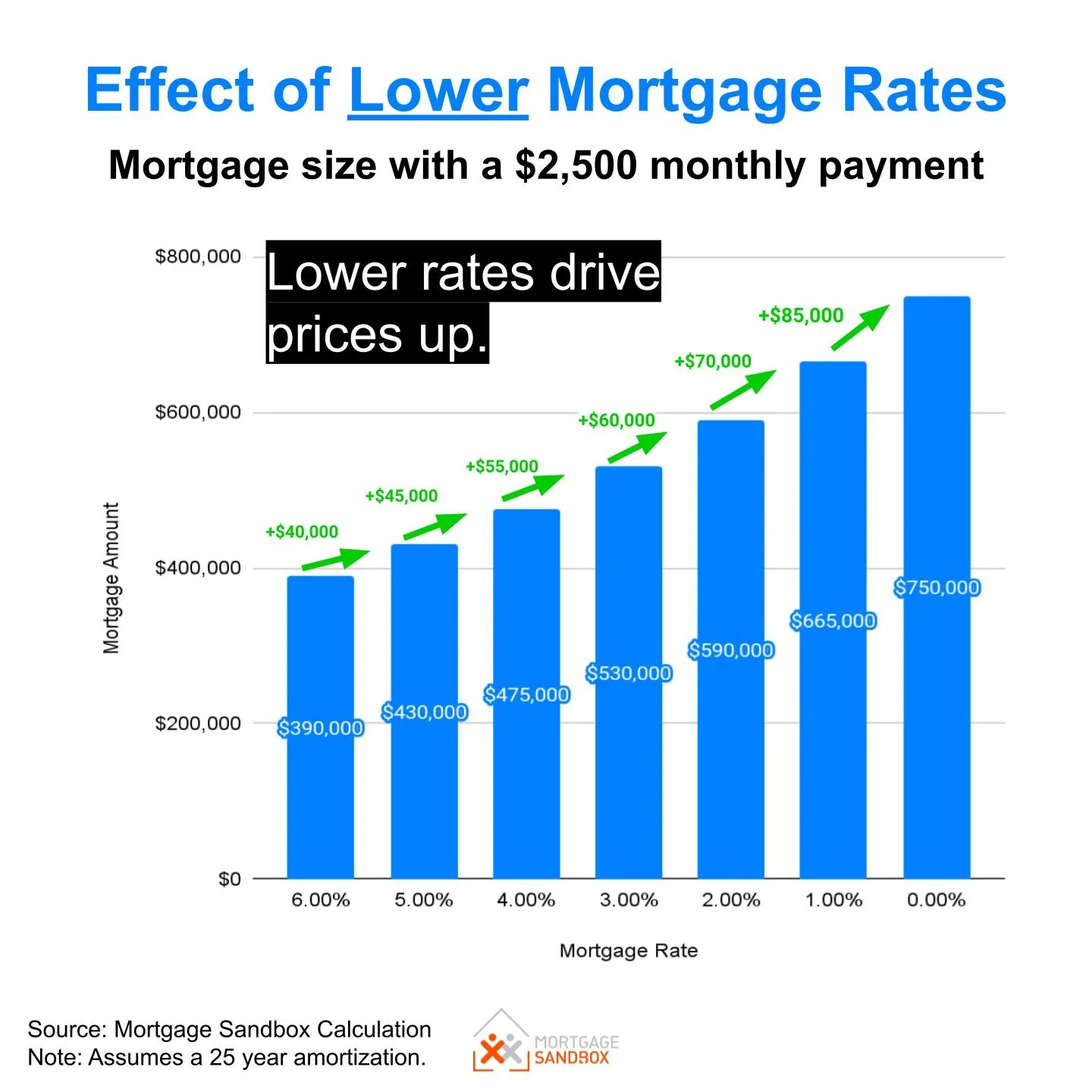

Mortgage rates don’t immediately mirror the policy rate, but the policy rate serves as a key anchor for banks’ cost of funds and thus influences what lenders offer.

📌 Real-estate note: While a 25 basis-point cut may not immediately translate into a dramatic drop in mortgage rates, the expectation of easier policy and stable rates matters for buyer psychology and listing strategies.

4. How this affects the Toronto / Ontario market specifically

-

In the greater Toronto region, affordability has been a key issue—higher interest rates squeezed budgets and slowed some sales activity. An easing environment can help.

-

Sellers who might have been cautious may now find there are more qualified buyers coming off the sidelines.

-

For investors: lower financing costs can improve cash-flow projections and return calculations, making small-scale investment properties more attractive again.

-

For first-time buyers: this may be a timely reminder to revisit budgeting and purchase-readiness.

-

As your REALTOR®, I can help interpret how this interest-rate backdrop translates into your specific neighbourhood, home-type, and budget scenario.

5. Strategic next-steps for you

Buyers:

-

Get pre-qualified now—we’ll work with your lender to survey the impact of the rate cut on your mortgage options.

-

Review fixed vs variable rate strategies in light of this decision and your risk-tolerance.

-

Expand your search with confidence: if the payment burden eases, you might access homes you thought were out of reach.

-

Let’s craft an offer strategy that capitalises on this moment of improved affordability.

Sellers:

-

Let’s conduct a market evaluation now: assess your home’s competitive positioning in the upcoming window of opportunity.

-

Prepare your home—staging, minor repairs, presentation—to ensure you’re ready to list when buyer interest rises.

-

Timing matters: listing now may catch buyers before they shift focus to other markets or before inventory builds.

-

Let’s discuss pricing strategy that reflects the slightly improved financing environment for buyers.

6. Visualising the Impact

🍁 What This Fall Market Means for Buyers in the GTA

The Bank of Canada’s latest rate cut to 2.25 % is more than just a headline — it’s a tangible opportunity for GTA buyers. With borrowing costs easing and lenders adjusting their fixed and variable mortgage products, your buying power has effectively increased. Whether you’re a first-time buyer trying to break into the market or a move-up buyer seeking more space, this fall could be the ideal time to act.

The GTA housing market remains diverse — from Toronto’s condo corridors to family homes in Durham, York, and Peel regions — and we’re already seeing signs of renewed buyer interest since the rate announcement. That means inventory may start tightening again as more buyers re-enter the market, especially for well-priced homes in desirable neighbourhoods.

Now is the time to take advantage of improved affordability and a slightly less competitive environment before momentum builds again.

Let’s sit down for a confidential buyer consultation to review your goals, pre-approval options, and neighbourhood strategies. As your REALTOR®, I’ll help you secure the right property at the right price — while the market is still in your favour.

📞 Call, text, or email me today to schedule your private consultation and discover what your next move could look like in this evolving market.

🍂 What This Fall Market Means for Sellers in the GTA

For sellers, the fall 2025 market brings renewed optimism — and a valuable window of opportunity. Lower interest rates are stimulating demand and improving buyer confidence, which can translate into more showings, stronger offers, and shorter days on market. Many prospective buyers who had paused earlier this year due to higher borrowing costs are now stepping back in.

This means your property could attract a larger and more motivated pool of buyers, particularly if it’s priced right and presented effectively. From professional staging to tailored marketing plans, positioning your home now — while the market is adjusting to this new rate environment — can help you stand out before winter listings begin to taper off.

Don’t wait until everyone else catches on to the changing momentum. Let’s review your home’s market value, current competition, and strategies to maximise your return this season.

Book your confidential seller consultation today, and let’s prepare your property to make the strongest impact in this more favourable market environment.

💼 Reach out directly for a no-obligation, one-on-one conversation — your timing, pricing, and preparation decisions today can make all the difference in your sale results tomorrow.

Navigating This Market with a Professional Advantage

Markets don’t wait — and opportunities like this come in cycles. Whether you’re buying your first home, upgrading, or selling an investment property, strategic timing and expert guidance matter.

As a trusted REALTOR® in the GTA, I provide market insight, negotiation expertise, and data-driven strategies to help you move confidently in today’s evolving landscape.

📲 Let’s talk confidentially about your next move.

I offer private consultations for both buyers and sellers to help you make smart, well-timed decisions in this shifting market.

Let’s turn this moment — and this rate cut — into your next real estate success.

7. Final Thoughts & Your Next Move

This week’s rate cut by the Bank of Canada is an important signal to both buyers and sellers: the environment for real-estate transactions is shifting favourably. Buyers have an opportunity to act with somewhat improved affordability, and sellers have a chance to access a broader buyer pool.

👉 If you are considering entering the market — contact me today. I’ll provide a tailored consultation:

-

For buyers: we’ll map out the best financing strategy and target homes at your new budget.

-

For sellers: we’ll prepare your home for listing, capitalise on current conditions, and hit the market at an optimal time.

Let’s leverage this interest-rate moment together. Markets move quickly when policy pivots. I’m here to ensure you’re ready.

The real estate market inside scoop for the community you love. See homes that are for sale and have recently sold. Find out if home sales in your neighbourhood are trending up or down. See what homes around you are currently selling for.